MSC director in conversation with NDTV Profit on the progress of Pradhan Mantri Jan Dhan Yojna (PMJDY). Catch full coverage here.

Blog

Customer Protection in Indian Digital Financial Services: Part 2: Transparency and Privacy

MicroSave’s study for the Omidyar Network on customer protection, risk and financial capability in India sought to understand the extent to which customer protection practices were embedded into DFS offerings in India. The research examined the effectiveness of these customer protection practices and the ease with which customers and agents could access them. In the first blog of this series, we examined Customer Recourse. This blog looks at Transparency and Privacy

2. Transparency

Communication with customers is typically verbal in nature

Our research showed that in most deployments, a well-developed customer support system in the form of regular interactions (SMS/voice) and monitoring visits by supervisors/managers to agents for optimising customer service is missing.

Furthermore, most customer communication is verbal. A small proportion of customers are not even provided information, either at the beginning or during the course of operation of their account. Some of the reasons for this were: agent did not have time; agent did not take interest; customers did not ask; and the agent explained initially, but they could not understand.

High dependence on agents both for terms and conditions of service, as well as for recourse options, makes customers highly vulnerable to agent-perpetrated fraud. Since most of the communication is verbal, the customers would not even know whether they are being defrauded or not.

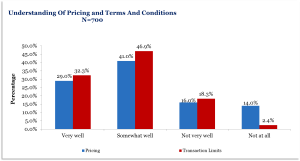

Around 2/3rd of the customers do not fully understand the terms and conditions of DFS service that they are using. Lack of awareness of service among customers is the largest stated barrier for DFS growth, according to MicroSave’s recent ANA India Survey.

Around 2/3rd of the customers do not fully understand the terms and conditions of DFS service that they are using. Lack of awareness of service among customers is the largest stated barrier for DFS growth, according to MicroSave’s recent ANA India Survey.

Communication Between Agents, Agent Network Managers, and Banks Needs to Improve

Communication Between Agents, Agent Network Managers, and Banks Needs to Improve

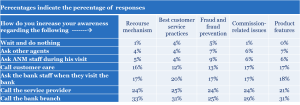

After the initial agency agreements, there is no active communication between the agent network managers (ANMs), banks and agents. The table below suggests that some agents try to reach out to the most responsive option, but a few just do not make any effort to reach out. This suggests that an active dialogue between agents and service providers is missing, and details are communicated only on the basis of a specific request from the agent.

Agents point out that lack of support for them in running the agency is one of the reasons why they do not recommend DFS/bank agency as a business to others.

Agents point out that lack of support for them in running the agency is one of the reasons why they do not recommend DFS/bank agency as a business to others.

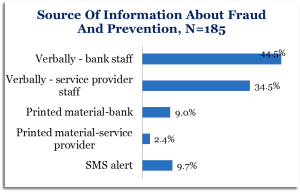

The current system of providing fraud and risk-related information to the agents is ad hoc, and only 63% of agents are provided information on frauds. In most cases, the information about risks is verbal and, thus, informal.

Proper formal communication about the terms and conditions of service is also not complete. Only 68% of all active agents reported having received documents with terms and conditions of service. Poor communication both at the customer as well as at the agent level means that the situation will facilitate external frauds as DFS grows and matures in India.

Proper formal communication about the terms and conditions of service is also not complete. Only 68% of all active agents reported having received documents with terms and conditions of service. Poor communication both at the customer as well as at the agent level means that the situation will facilitate external frauds as DFS grows and matures in India.

Moreover, coupled with low awareness levels about recourse among customers and high dependency on the agent for information and recourse, most customers, ANMs, and banks will not even know about risks/frauds until they have become big.

3. Privacy: Customers

Experienced customers (who have had an account for more than one year) are more aware of the means to protect their account information. More than one-third of all customers interviewed highlighted that they do not share their PIN. But, once again, agents are the most important source of information about methods to protect accounts.

Experienced customers (who have had an account for more than one year) are more aware of the means to protect their account information. More than one-third of all customers interviewed highlighted that they do not share their PIN. But, once again, agents are the most important source of information about methods to protect accounts.

As highlighted earlier, one of the major risks is transaction data security. However, MicroSave’s qualitative study shows that most transactions are assisted by the agent who thus has access to account details.

CGAP notes that assisted transactions are common particularly with elderly customers and in rural areas where literacy levels are low.

3. Privacy: Agents

Agents are very proactive in protecting their personal and account information and do not share personal account-related information with others.

Though these are good practices, there are a number of ways in which fraud can happen, about which they are not aware and thus do not know about its prevention. (See Survival of the Fittest: The Evolution of Frauds in Uganda’s Mobile Money Market (Parts 1 and 2)).

In the same way that operational issues often lead to service denial (“Real and Perceived Risk in Indian Digital Financial Services”), the precautionary measures adopted by agents also often result in service denial to customers in different forms. As highlighted before in a variety of MicroSave and CGAP publications, this service denial undermines trust in digital financial services.

There is a clear need for significant improvements in the communication of both DFS products and how to use them in India. Not all agents will be able to do this, as it involves fundamentally different skills than conducting transactions, but many will be able to do so, given their existing (remarkably – almost alarmingly ― trusting) relationships with customers. Agents who really can only perform basic transactions to service existing products, should be supplemented with sales agents charged with clearly explaining products and how to use them.

Fair Price Shop Ownership: How Viable Is It?

India’s Targeted Public Distribution System (TPDS) is the largest food security distribution network in the world. The National Food Security Act (NFSA) 2013, aims to cover 75% of the rural and 50% of the urban population through this network. The network also provides employment for 478,000 Fair Price Shop (FPS) owners, their employees, and hired labour, who work across the supply chain in corporations and godowns. In order to curb diversions, FPS automation was proposed. In this Note, we specifically talk about the revised commissions proposed by the Cabinet Committee on Economic Affairs (CCEA) of Rs.70 (US$1) per quintal of ration and an additional Rs.17 (US$0.25) per quintal for FPS owners making sales through Point of Sale (POS) devices are not proving enough for FPS onwers. With these levels of commissions, many FPS owners are likely to close their shops. In the end we recommend developing an economic model to optimise the business case for FPS owners.

Low Cost Housing Markets

Access to housing is a basic right and is important in improving livelihoods of poor people. There have been various efforts to support the poor to access low cost housing. MSC recently with support from Habitat for Humanity International and some microfinance institutions in Kenya, supported the development of housing microfinance to improve housing situations among low income people. In this video, George Muruka, Senior Specialist, Private Sector Development, at MicroSave speaks on the key concerns affecting low cost housing market in Kenya.

Savings Achieved through FPS Automation: Step for Greater Efficiencies

Under the Targeted Public Distribution System (TPDS) system, state governments give licenses to Fair Price Shops (FPSs) to distribute commodities to low-income segments.However, distributing through FPSs has always seen problems of diversion and “leakages”. A high-powered committee appointed under Mr Shanta Kumar, Member of Parliament, estimates that 46.7% of goods distributed through FPSs were lost to “leakage”. Two models suggested in the Shanta Kumar committee report to arrest leakages, are: 1) direct benefits transfer; and 2) automation of distribution channel. In this note, we discuss savings that have accrued to the state of Andhra Pradesh and Telangana (partially) because of automation of FPSs. Based on the findings, we can divide savings (realised/disguised) into three broad types:

1. Savings due to one-time activity of de-duplication;

2. Recurring savings due to beneficiaries willingly not turning up to receive their entitlement; and

3. Savings due to inconvenience ― currently being calculated by states, but which should not be included. These savings are due to transaction denial owing to server failure and/or authentication failure; or closed shop.

Automation of the front-end distribution system in PDS results in very significant savings to the government. These savings justify the investment in deployment of automated systems. The one challenge that we foresee is that profitability of FPSs has come down drastically, as diversion of food grains has stopped. Our calculations show that profitability of an FPS outlet in the automated environment will be down to Rs.1,100 (USD 16.18) per month. Discussions with stakeholders shows that in the non-automated environment, FPS shops were making a profit of Rs.60,000-70,000 (USD 882-1,029) per month. State governments will have to relook and work out a commission structure that can ensure the long-term viability and sustainability of FPSs.

DBT in TPDS – A Mid-line Assessment: The Road Ahead Seems To Be Long

Government of India (GoI) implemented the National Food Security Act (NFSA) in 2013 to provide food and nutritional security to vulnerable households. Simultaneously, to make the system more efficient and to plug leakages, GoI requested States/Union Territories (UT) to implement a Direct Benefit Transfer (DBT). Two suggested methods were: 1) installation of point-of-sale (PoS) devices at fair price shops (FPSs) for biometric authentication of beneficiaries, and physical off-take of food grains, or 2) direct cash transfer to the beneficiary’s bank account. The UTs of Chandigarh, Puducherry, and Dadra & Nagar Haveli (DNH) opted for DBT through cash transfer. Chandigarh and Puducherry launched DBT in PDS in September 2015. However, DNH postponed the pilot roll-out due to upcoming local elections. To assess the performance of these pilots, MicroSave conducted a baseline assessment in August 2015, and a midline assessment in November 2015. We presented the baseline assessment in a separate note and this note looks at findings from the mid-line assessment. Progress in both the UTs of Chandigarh and Puducherry is chequered and needs streamlining before the pilot for DBT in PDS can be scaled up. On parameters such as access to market, availability of withdrawal points, and use of the subsidy payments, the pilot has done well in both UTs.

However, the pilot has highlighted the need for additional work on awareness – a recurring theme (see “Communication: The Achilles Heel of Direct Benefit Transfer – 1 and 2”) ― and grievance redressal. There are also challenges in terms of adequacy of subsidy amount and whether there is subsidy diversion by male beneficiaries in the household. In Chandigarh, FPS shops closed down after the pilot launch. However, not all beneficiaries have managed to enrol for DBT, due to requirements related to the opening of bank accounts and linking these to their Aadhaar numbers. Puducherry has seen similar challenges. The administration will have to look into this aspect, as exclusion can be detrimental to the overall success of the scheme.