A lot of financial inclusion efforts around the globe are targeted towards people who are new to technology and perhaps new to the formal financial system. Many of these people belong to Oral segment of society. “Oral” people are not comfortable with written numbers, they also do not know how to read and rely on mental calculation when it comes to any mathematics. Learning about them is critical for all of us who are working to make digital financial services work for financial inclusion, as these people form the financial excluded segment largely.

The objective of this research was to develop conceptual wireframe of a mobile wallet for ‘oral’ people to use. The user interface was developed keeping in mind the cognitive usability constraints of oral segment.

The result of our work is first ever wallet design for Oral ; that’s what we call it – MoWO – mobile wallet for oral. We believe MoWO is the first step in the right direction when it comes to financial inclusion of Oral people.

It was a hot and dusty day as our team drove into Meheba refugee settlement in the North-Western Province of Zambia. Our energy was high, though it was the adrenaline that kept us going after a couple days without sleep. We were going to see the initial results of a nine-month journey towards digitization of cash-based intervention (CBI) payments to refugees in Meheba, a joint project of the Office of the United Nations High Commissioner for Refugees (UNHCR) and the United Nations Capital Development Fund (UNCDF).

As we neared Block D, a woman waved at us. We recognized her as Judith, a refugee from the Democratic Republic of the Congo. She, on behalf of her family of eight, receives CBI payments once every two months. Judith is 67 years old and lives with her husband, two daughters and their husbands, and three grandchildren. During the SIM card registration process that was part of the digitization pilot, her husband was registered to receive the CBI payments on behalf of the family. However, Judith came to us and insisted that they had jointly decided to have the SIM card issued in her name as she is responsible for the household expenses.

We waved back at Judith, pulled out a mobile phone and showed it to her. She immediately understood, held up her SIM card and pointed towards the administration centre, where she can cash out from her mobile wallet. Judith joined us as we were setting up the desks for Airtel Money staff to help refugees cash out their CBI payments. She was the third customer in the queue that day. After cashing out, Judith sought us out with tears in her eyes to share her experience: “I did not believe you when you said that it will take less than two minutes to withdraw my benefit money from the SIM card. We put my SIM card in the agent’s mobile phone, put [in] my secret number and, see, I have money in my hand. It is like magic. This is the first time I have received money so fast. Thank you so much.”

The smile on the face of many beneficiaries like Judith was enough to rejuvenate us. The journey to digitize CBI payments, like other digitization initiatives, had been fraught with challenges. These challenges, along with the financial needs of the residents, were identified during research conducted in Meheba in September of 2017, which is detailed in the research highlight ‘Can digitization of social cash transfers improve the lives of refugees in Zambia?’. This blog, however, focuses on lessons learned during the sensitisation process and two digital payments piloted in Meheba in April and July 2018.

Sensitization of beneficiaries

Communication with beneficiaries: In a settlement the size of Meheba (720 sq. km with a population of over 20,000), it was very difficult to identify the beneficiaries. The beneficiaries live in significantly dispersed locations in six different blocks across the settlement. During the first test, several different sensitization approaches were attempted: conducting house-to-house visits, employing word-of-mouth, utilizing megaphones, and using Community Development Workers and Community Youth Workers to mobilize CBI beneficiaries for sensitisation and for SIM card registration. Megaphones had the maximum impact and were used in subsequent sensitisation and SIM card registrations, leading to the successful mobilization of beneficiaries.

Venue for sensitization: Meheba is arranged into various blocks, from Block A to Block H. Each block has several internal roads. Initially, door-to-door and road-wise sensitisation approaches were used, with the aim to reduce inconvenience to beneficiaries. However, most beneficiaries were not at home, as they were away working on farms, in trading areas, etc., which meant that sensitisation took longer and was inefficient. Therefore, another approach was sought. In the end, the most effective means to sensitise a large number of people was to conduct the sessions in a central area (a town hall) in each block.

Nomination of a household representative: Traditionally, CBI payments were distributed to the head of the household (focal point) who collected the money on behalf of the family. In the digitization project, the decision was made to register the SIM cards and mobile wallets at the household level as well, rather than the individual level, to avoid practical challenges such as issuing SIM cards to minors. During the sensitization process, instead of registering the heads of household by default, beneficiaries were asked to nominate a household representative to receive the digital money on behalf of all household members. It was important for the beneficiaries to choose the right representative who would be available to receive the CBI payments and use them for the benefit of the family.

SIM card and mobile wallet registration

Training of the GSM and mobile money team: SIM card and mobile wallet registration failures mainly occurred due to technical challenges (system upgrade), poor network quality, poor document quality for know-your-customer (KYC) requirements (crumbled or faded ID documents) and human error. It became clear that it is very important to train both GSM and mobile money team members on the importance of understanding the beneficiaries, error-free data capture and alternate KYC documentation validity. The training helps to ensure more successful SIM card and mobile wallet registration from the start, which results in more satisfaction by the beneficiaries and lower costs for the mobile money provider.

Sharing of registration reports: The key stakeholders needed to agree on the turnaround time for different reports related to successful and failed SIM card and mobile money registrations and reasons for failure, as well as the method for re-registration of SIM cards without any inconvenience to the beneficiaries. Coming to an agreement is crucial to ensuring that beneficiaries have a positive experience from the registration process onwards and start trusting the communication from different stakeholders. Further, the stakeholders must have a prior agreement on the format and turnaround time for validation of SIM cards and KYC documentation, which is vital for seamless transfer of funds to beneficiary accounts.

Stakeholder engagement

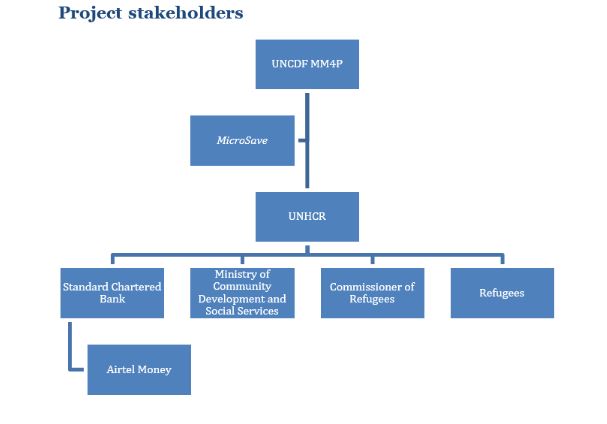

As with any digitization initiative, strong partners are critical for its success. The stakeholders in the CBI digitization project in Meheba are depicted in the figure. Strong partnerships allowed UNHCR to disburse the first digital payments within 24 hours of the final decision.

The highly motivated stakeholders and the strong relationships between them also helped in finding alternative mechanisms, such as the use of a cash-in-transit facility to disburse cash to the beneficiaries who were not part of the first digital payment.

Clear communication

Continuous communication to the beneficiaries about the venue and date for SIM card and mobile wallet registration, the required documents for withdrawal and the disbursement date for the first payment was crucial to ensuring the efficient utilization of resources from UNHCR and its partners.

Although SMS text messages were sent to confirm the digital payment transfers to the beneficiaries’ mobile numbers, the digital transfer information was also communicated through word-of-mouth and through megaphones to those without mobile phones. These approaches proved to be effective means of communication.

Support of beneficiaries during cash-out

Research indicated that only 52 percent of the beneficiaries owned a mobile phone. To support the beneficiaries who did not have a phone during withdrawal, Standard Chartered Bank organized for extra mobile phones to be provided to every Airtel Money agent in the settlement. The agents assisted the beneficiaries, who came only with a SIM card, to withdraw using these extra mobile phones. This approach helped to reduce the overall cost of digitization as well as to make sure that all beneficiaries were able to cash out their payment easily at an agent location.

It was important to create a positive experience by supporting the beneficiaries, especially those who were first-time users, to check their balance, withdraw their money and see the other services available on the mobile phone.

Reporting

Developing reporting requirements regarding timelines and formats among all stakeholders helps to ensure smooth functioning of digital payments.

Key success factors

As with any pilot, it is critical to identify lessons learned that could drive improvement of products and services in the next iteration of the project. The digital payments in Meheba were a great success: 57 percent and 100 percent of payments were sent to beneficiaries’ mobile wallets in the first (April) and second (July) digital payments, respectively. Ninety-seven percent of beneficiaries were able to withdraw from their mobile wallets immediately. The cash-out process took only about three days as opposed to the manual process that used to take 10 to 13 days. It is expected that, as beneficiaries gain trust in the services over time, they will not immediately cash out all of the money in their wallets. This shift will also depend on the continuous availability of agents within the settlement to enable cash-out at any time.

The success of the two digital CBI payments lays the foundation for developing a digital ecosystem in Meheba by identifying additional services that could be digitized. This effort will include offering mobile wallets to other residents in the settlement, guaranteeing the availability of well-trained agents in the settlement with sufficient liquidity and, finally, moving towards digital means of paying for goods and services (merchant payments). These achievements could not have been possible without rigorous pilot preparation, continuous community engagement and concerted efforts from the multiple stakeholders who were involved in the testing and iteration of the digitization processes. Other assistance programmes provided by UNHCR that are also being considered for digitization include the distribution channels for non-food items and the DAFI scholarship programme that helps to fund the education of refugee students to access tertiary education. A similar approach is intended to digitize CBI payments in Mantapala refugee settlement in Zambia, which hosts over 10,000 refugees.

Overall, feedback from the beneficiaries as well as from various stakeholders was positive and encouraging. UNHCR and UNCDF are working together with Standard Chartered Bank and Airtel Money to streamline processes and to develop solutions to address some of the challenges identified.

The hope is that, with these successes, digital ecosystems can be replicated in the other two refugee settlements in Zambia, thus ensuring that humanitarian assistance can be delivered in a timely, transparent and efficient manner that achieves its main goal: to assist refugees as they acclimatize to a new way of life in their new home.

With testimonials from the beneficiaries and the implementing partners, this video summarizes the journey to digitizing payments to refugees in Meheba, Zambia.

The long debate on the constitutionality and purpose of Aadhaar may not end with the judgement of the Supreme Court but it will certainly become more specific and narrower. In a landmark judgment, the five-judge Supreme Court bench opined with a 4:1 majority that Aadhaar is legitimate and proportional. The judges observed that although Aadhaarinfringes on the right to privacy slightly, the benefits it provides to the marginalised sections of society serves a much larger purpose. It provides rightful benefits and dignity to the marginalised that outweighs the perceived harm.

In the judgement, the judges struck down section 57 of the Aadhaar Act that deals with sharing of data with corporate bodies. It is not yet clear whether corporates are barred completely from using Aadhaar infrastructure or if they can use it as one of the options to provide services to customers but cannot mandate it. From the verdict, it is yet unclear if it is left to people to choose if they wish to share the data (or not) or if it is a blanket ban. For instance, if someone wants a mobile connection to be activated instantly, then it is still unclear if that person can use Aadhaar-based e-KYC instead of waiting for 3-4 days for paper-based KYC. This conundrum would be the same for bank account opening.

Repealing section 57 may have a huge impact on Aadhaar-enabled services, especially on e-KYC, and Aadhaar-enabled Payment System (AePS). Over the past few years, AePS has become the default method for people to withdraw money from local banking business correspondents, especially in rural India. Using biometrics to conduct a financial transaction, which in most cases is limited mainly to withdrawals and deposits, had removed several barriers. These include the need to remember the PIN for debit card and fill withdrawal or deposit slips, which become particularly difficult for illiterate and innumerate people in rural areas.

The process of using AePS is intuitive and simple for people, as they do not have to learn anything new. The only change is that they have to apply their thumb on the biometrics reader instead of on a piece of paper. This is in contrast to a debit card or other modes, which call for considerable efforts to educate users. And even then, they may need assistance to either fill up a form or enter the PIN correctly. This makes these users susceptible to fraud.

Since the government transfers most benefits, such as pensions, scholarships, and others electronically, people only need to access their bank account to withdraw this money. If AePS is scrapped, people may have to go through the ordeal of traditional technologies, such as debit cards or go back to filling and signing or putting their thumb impressions on papers!

The Supreme Court has allowed the government to continue using Aadhaar to deliver benefits and services where money is drawn from consolidated funds of India. This is a welcome move. The Direct Benefit Transfer (DBT) programme primarily relies on Aadhaar to uniquely identify and target beneficiaries. This led to reducing leakages by removing duplicate and “ghost” beneficiaries. Current government estimates point to savings under DBT to be around INR 90,000 crore. Aadhaar authentication for lifting ration through the Public Distribution System (PDS) ensures that identity fraud is reduced and denial of the ration is also controlled.

Our studies show that beneficiaries are aware that transactions now leave digital trails and the Fair Price Shop (FPS) owner can be challenged in case of identity fraud or denial. This is also altering the social fabric of rural India, where FPS owners had absolute authority on providing or denying ration to people. Our studies show that now these cases have reduced.

However, issues related to technology still exist. These include non-functioning biometrics, issues with connectivity, among others, which have led to a denial of benefits in a few cases and led to more severe implications for some. The Supreme Court clarified that the government should create alternate mechanisms for people who cannot authenticate using biometrics. A few states already use alternate methods of authentication for the population that cannot perform biometric authentication.

For instance, the Jharkhand government introduced the concept of Apwaad Pustika (exception book) to provide ration to people who cannot authenticate using Aadhaar. Similarly, Andhra Pradesh made multiple provisions to handle exceptions in case of biometric failures, such as One Time Password (OTP) and making a list of such people and granting them exception, etc. However, the efficacy of such mechanisms has come under question and needs scrutiny. The central and state governments must take note of the Supreme Court judgement and review processes and systems thoroughly to handle exceptions so that no one is denied benefits.

The Supreme Court has also clarified that banks, educational institutes, or other corporates cannot force people to provide their Aadhaar number. Even the government can seek Aadhaar only from people who want to draw benefits from the consolidated funds of India. PAN is the only exception where such linking has been made mandatory. Limiting purpose and period of storing metadata is another landmark step. This allays some fears of people around breach of privacy. However, the debate would continue and the government will have to come up with rules or legislative changes to comply with the verdict. We expect more details to emerge as the detailed copy of the judgement is read and analysed.

Details of the poverty levels of our 50 ‘diarists’ can be found in the article on savings listed on the publications page there. In short, they fall into four classes, ranging from extreme poor to near-poor. In this article, we look at the borrowings of our diarists, using daily data for the period from March to October 2016.

For Bangladesh, more than any other country, microfinance also symbolizes the nation’s economic and social development, with growth in the sector and the sustainability of its institutions coalescing with the persistent decrease in poverty and extreme poverty rates at the national level. Its fame has, however, drawn tough scrutiny from international donors and researchers concerned with its impacts on the ground.

In our earlier blogs, we expressed our concerns around the growth of the digital divide, as the focus for financial inclusion shifts to FinTech and superplatforms as “the definitive solutions”. While these solutions typically require smartphones, many of the poorer households in Asia and Africa simply do not have access to the devices. Neither do they have access to the bank accounts that are typically required to use the solutions effectively.

While there are potential solutions that could empower those without access to smartphones through the use of agents, it is also clear to us that successful efforts to foster financial inclusion involves three inter-related and mutually-reinforcing components. These are:

1. A national digital ID system, bank accounts, and, ideally, mobile phones for all

2. Bulk payments, which are typically government-to-people (G2P), to drive uptake and usage and thus foster trust in the digital ecosystem;

3. A seamless, interoperable payments system.

This is why everyone is so excited about the digital ecosystem currently under development in India. It combines these three elements. In this blog, we examine these in some detail:

1. A seamless, interoperable payments system

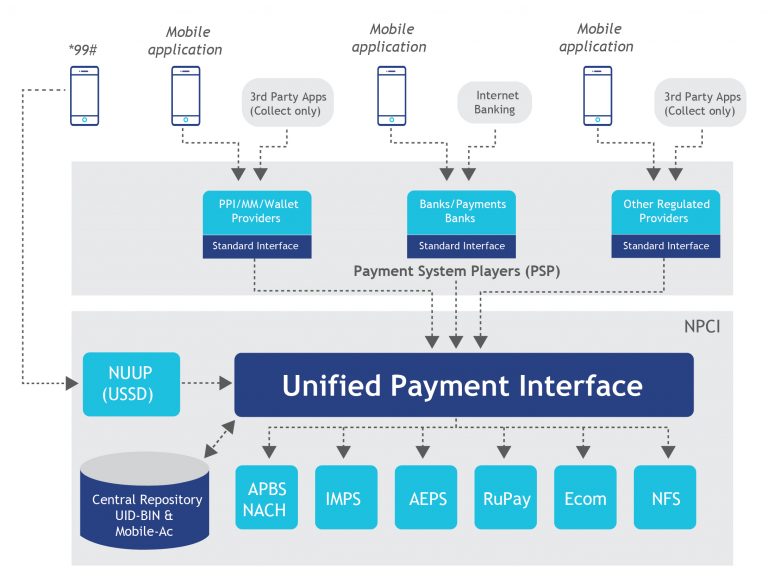

Unified Payments Interface (UPI): The UPI was developed by the National Payments Corporation of India (NPCI). The NPCI already operates the RuPay payments infrastructure as a lower cost rival to Visa and MasterCard to permit banks to interconnect and transfer funds. The NPCI was established by the RBI and Indian Banks’ Association (IBA) in April, 2009. It aims to consolidate and integrate India’s numerous payment systems and thus create national, standardised business processes for all retail payment systems.

The UPI provides a single, digital interface across all systems for smartphones (but not feature phones) linked to bank accounts. It provides users with the ability to make payments using 1-click 2-factor authentication, using just a personal smartphone without requiring any acquiring (swiping) devices or physical tokens. The diagram below illustrates this in detail.

To do this, the UPI allows a unique digital identifier for every bank account in the country, which can then be used to send money using India’s existing Immediate Payment Service (IMPS). The unique identifier is almost like an email address or an assigned name as well. It allows users to transfer money 24/7 and instantaneously to any other account in the country without requiring either a digital wallet, a credit card, or a debit card.

As a result, UPI users can make payments simply by exposing their unique identifier (the Virtual Payment Address (VPA) without sharing account details. The UPI also offers both individual users and business entities with the ability to send payment or “collect” requests to others with a “pay by” date. Users can also delay payment requests for later payment before the collection expiry date without having to block the money in their accounts. Users can, therefore, use their mobile phone to “pay” someone (push) as well as to “collect” from someone (pull). In the future, users will also be able to pre-authorise recurring payments, such as for school fees, subscriptions, and utility bills, with a one-time secure authentication and rule-based access.

UPI offers a fully interoperable system that incorporates all players in the payment ecosystem without silos and closed systems, allowing users to transact from and to any bank. In the long-term, it is likely to result in the phasing out of debit and credit cards and point-of-sale devices—except perhaps in places where many foreigners frequent. Similarly, mobile wallets are likely to face a challenge from the rollout of UPI.

With the arrival of UPI, the 14 million merchants in India will be able to accept digital payments with ease. It has the potential to make every merchant, or indeed each individual, a cash-in and cash-out agent and accelerate the rollout of a “cash-lite” India. And, of course, both Google Pay and WhatsApp payment system are riding on UPI.

BHIM Aadhaar PayBHIM Aadhaar Pay was launched in early 2017 to make payment to merchants with biometrics instead of relying on other form factors like phone, cards, etc. The merchants can download the app and, using a certified biometric scanner, accept payment. To make a payment, a customer simply needs to enter their Aadhaar number in the merchant’s app and select the bank from which they wish to make the payment. The customer’s biometrics, which is typically the fingerprint, is then used as the password for the transaction.

2. A national ID system and bank accounts for all

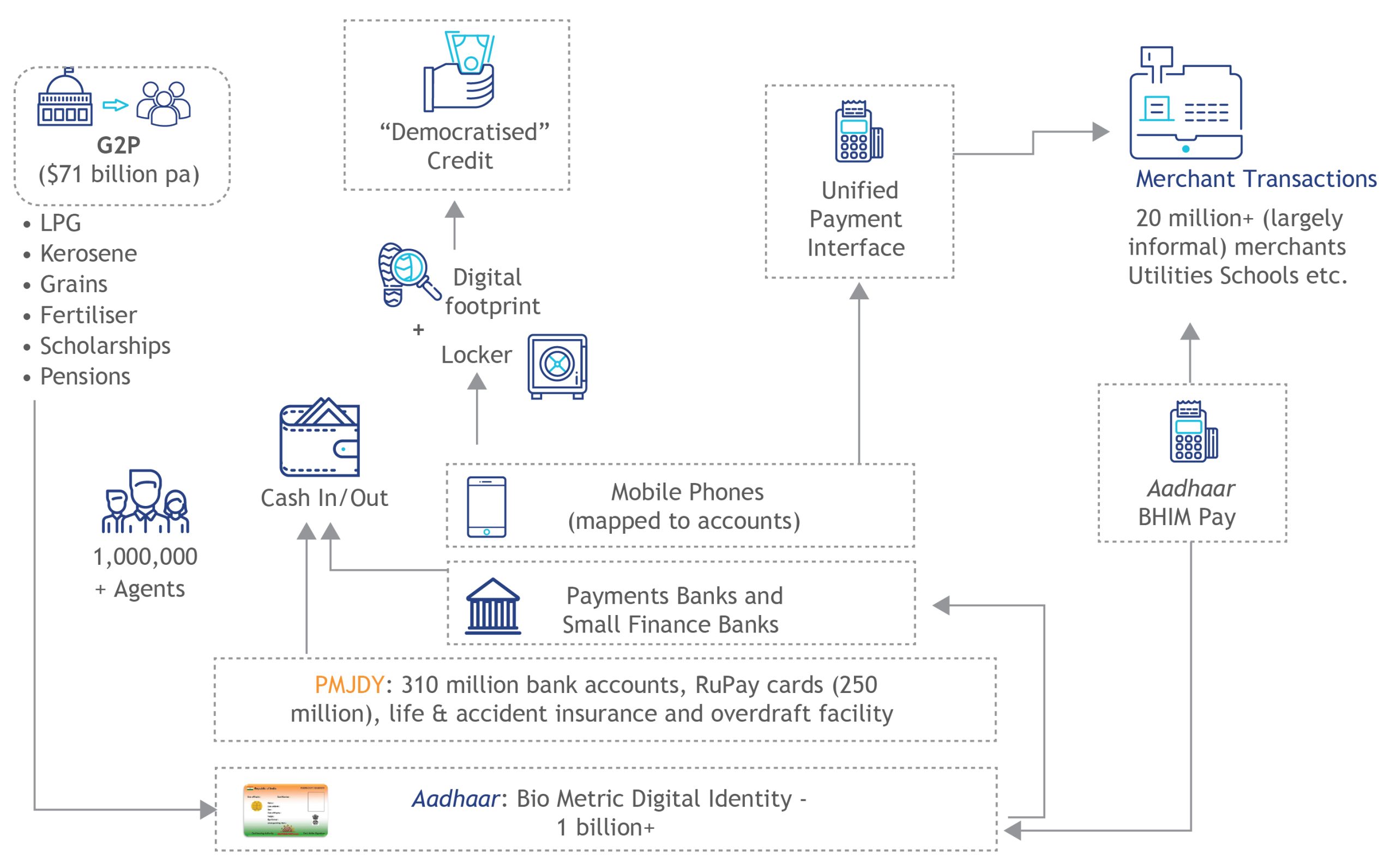

The Aadhaar national biometric digital identity system. More than a billion Indians, well over 85% of the eligible population now have unique biometric digital identity cards. Their biometric data (fingerprints and iris scans) is held on a large database overseen by the Unique Identification Authority of India. Under the current regulations, this allows KYC/AML for basic account openingand for authenticating transactions. Aadhaar is the foundation for the India Stack (see below).

The Pradhan Mantri Jan-Dhan Yojana (PMJDY): In 2015, the Government of India launched the PMJDY financial inclusion scheme to provide banking to all households without access to the formal financial system. PMJDY provides debit cards, insurance, pension facilities, and overdraft to beneficiaries. Within two years of the launch of the scheme, banks and their agentshad opened 310 million accounts. While MicroSaveestimates that around a third of these were opened by people who already had another bank account, the impact in terms of access to basic banking services was impressive. PMJDY-2.0 was launched in August 2018 with enhanced benefits including the doubling of the overdraft limit to INR10,000 (USD139) and INR200,000 (USD2,778) accident insurance cover for RuPay cardholders.

Payments banks and small finance banks: While almost all PMJDY accounts were opened by public sector scheduled commercial banks, the Reserve Bank of India (RBI) created two new types of banking licenses based on the Mor Committee’s recommendations. Given the precarious state of India’s public sector banks, this looks like a prescient move. Payments Banks are permitted only to offer payments and limited savings servicesbut may not lend to their clients. These payments banks are expected to leverage digital technology to maximise their reach and minimise operational costs. In contrast, small finance banks were created to allow selected microfinance institutions to transform and begin to mobilise deposits from the low income, mass market.

Mapping mobile phones to bank accounts and the India Stack: The next key part of the development of the ecosystem will be to map account holders’ mobile phones to their bank accounts. The mapping exercise will allow them to conduct transactions and begin to fill their “digital locker” with transaction data from their phones, as well as other Aadhaar enabled devices. This key data will complement other key records, such as education certificates and land titles, also stored in the locker – thus creating a “digital footprint” to inform financial service providers.

An ever-increasing proportion of India’s adult population now owns smartphones – a figure that is set to rise to 50% by 2020. Those with smartphones will, (subject to trust and connectivity issues) be able to use the UPI. The UPI will allow both push and pull transactions, using basic identifiers similar to email addresses or telephone numbers. Currently UPI is free, thus removing the need for merchant discount rates and other charges for making payments. This effectively enables merchants and individuals to use the UPI in the same way as they currently use as a point-of-sale device to effect transactions and receive payments.

All these paperless, presence-less, cashless transactions will create a digital footprint, stored in the user’s digital locker. The India Stack offers open application programming interfaces (APIs), which thus encourages the full force of local and international creativity to leverage the ecosystem and offer value to users in a variety of ways.

3. Bulk payments– typically government-to-people (G2P) payments – to drive uptake and usage and thus foster trust in the digital ecosystem

Government-to-people (G2P) Payments: The Government of India transfers around USD 71 billion to its citizens every year. These transfers comprise cash as benefits and pensions, as well as kind as grains, kerosene, and fertilisers, among others. This provides a tremendous opportunity to kick-start financial inclusion by using these transfers to seed digital money into bank accounts. Furthermore, the savings that arise from digitising these payments and linking them to biometric identity are breath-taking – and enough to pay for the cost of rolling out Aadhaar every 4-6 months. The estimates of what is quaintly referred to as “leakage” suggest that for many schemes, as much as 40% of the amount transferred does not reach the intended beneficiaries.

However, there are a surprising number of challenges to digitising G2P payments effectively. These range from the basic need to link bank accounts to Aadhaar numbers, to ensuring that there are adequate agents and retail outlets. The availability of adequate outlets would allow beneficiaries to cash-out and then buy grains and other items if their benefits are transferred directly in cash to their bank accounts.

These three ingredients come together in India’s remarkable digital ecosystem to create the basis for not just financial inclusion but to create digital footprints for the poor. This begins the journey to “democratised credit” – as the diagram below highlights.

Each of these three key ingredients plays a synergistic role:

National ID, bank accounts, and mobile phones provide the foundational layers and channels for people to enter and participate in the digital financial ecosystem;

Bulk payments (typically G2P transfers) push the digital value into these accounts and thus encourages their use and development of trust in digital money as opposed to paper money;

Based on this, the seamless, interoperable payments system encourages further use of digital money, thus building the digital footprints that will allow people to participate fully in the financial system, and to derive real economic value from it.

Each of the three is essential to achieving meaningful financial inclusion – as we have seen that simply opening bank accounts is not enough.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.