Ghiyazuddin Mohammad – Manager, Digital Financial Services and Country Programme Development for Indonesia – presented at the International Telecommunication Union (ITU) workshop on “Digital Financial Services and Financial Inclusion” in Geneva, Switzerland on 14-15 December 2015.

Ghiyaz was part of the Customer Protection working group and presented on the topic – “”Mitigating Consumer Risks in DFS: Perspectives From Indonesia””. The presentation highlighted top five consumer risks related to digital financial services as identified in Indonesia. These risks are – low customer awareness, poor customer experience, poor quality of agents, remote transactions in the absence of customers and liquidity management issues. Ghiyaz talked about ways to mitigate these risks both from a policy and provider perspective.

Ghiyazuddin Mohammad – Manager, Digital Financial Services and Country Programme Development for Indonesia – presented at “”International Conference on the Linkages between Financial Inclusion and Financial Stability”” organised by Alliance for Financial Inclusion (AFI) in Bali, Indonesia on November 30th & December 1st, 2016. More than 100 participants across 30 countries from AFI members and partner organizations participated in the conference. The conference was co-hosted by Bank Indonesia and the Alliance for Financial Inclusion (AFI) with the participation of AFI member and partners including: the International Monetary Fund (IMF); the World Bank Group, the Financial Stability Board, the South East Asian Central Banks Research and Training Centre (SEACEN), and academic institutions.

Ghiyaz presented on the topic “”Digital Financial Services & Financial Stability – Perspective From Indonesia””. He spoke about the growth of digital financial services in Indonesia and abroad and its benefits and systemic risks to financial stability. He also deliberated upon the existing DFS regulatory framework in Indonesia and its compatability with the objectives of financial stability. Other presenters in the panel included representatives from Bank Indonesia, Bank of Tanzania, Bank of Ghana and the University of New South Wales, Australia. The session was moderated by Dr. Alfred Hannig, Executive Director of AFI.

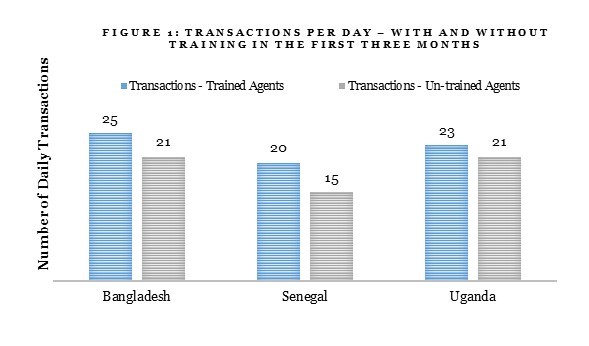

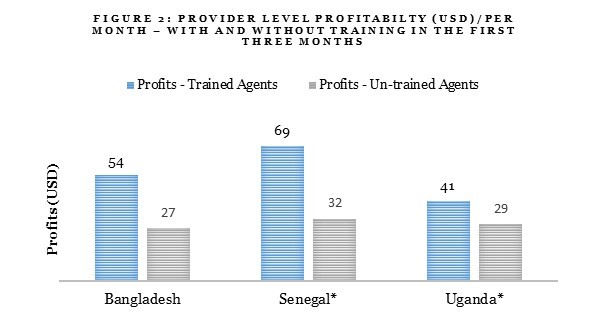

The Helix Institute of Digital Finance recently concluded the second wave of the Agent Network Accelerator (ANA) study in Bangladesh, which, along with a number of other key findings, highlights the importance of agent training in the first three months of inception (‘starting the agency business’).The ANA 2016 Bangladesh Report highlights that agents who receive training in the first three months of starting the agency business conduct, on average, 20% more transactionsper day compared to those who do not. These agents also earn USD 27 per month more than their untrained peers. We witnessed similar trends in Senegal (2015) and Uganda (2015), where trained agents conducted 33% and 10% more transactions per day, respectively. Agents in Senegal and Uganda also reported higher profits*. (See Figure 1 and 2 below)

Figure 1

Figure 2

It is not the first time we are learning about the importance of agent training. The Helix Institute, in partnership with the Harvard Business School, conducted econometric analysis and found that well-informed agents perform better in the face of competition and also experience higher demand for services. Well-informed agents, it argued, are a product of inception and refresher training.

While it is evident that training makes agents more knowledgable and, thus, the preferred choice of customers, we wonder whether training only influences agent knowledge. Is it also that a trained agent is more motivated to expand and improve his business? Does training change anything else for agents?

Recent data from Bangladesh (2016), Senegal (2015) and Uganda (2015) demonstrate a rather interesting story of what else training might be doing to the agents.

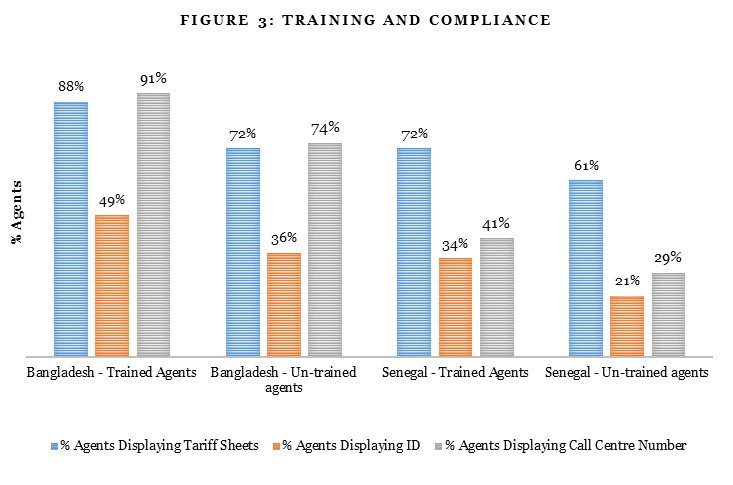

Compliance,** too, is affected by training

We find that agents who are trained in the first three months of starting their agency business are more likely to be compliant – they display tariff rates, grievance redressal cell numbers, call centre numbers, and unique ID or certificate from the provider (Figure 3). Interestingly, these, more compliant, agents also perform better than the non-compliant ones.

Since the number of transactions at an agent point is primarily a function of customer’s trust in service and in the agent, in the light of findings above, we hypothesise that training in first three months is a significant factor in helping make agents more compliant, and hence, more trustworthy, from the customer’s perspective.

Agent compliance enhances the “appearance and impression”/ “look and feel” of an outlet, and contributes to a sense of legitimacy that makes both the agent and customer more confident. It can be argued that this helps improve customer services by making agents more client-centric, which can help build agent/customer trust and improve the customer’s experience.

A logical extension of agent compliance to outlet set-up is their modus operandi of running the outlet. A compliant agent will be more likely to follow providers’ instructions/suggestions on liquidity management and customer engagement. A compliant agent will, therefore, be more hands-on in managing liquidity (critical to DFS) to ensure minimal denial of transactions due to lack of liquidity; and will be more pro-active in supporting customers when the latter face challenges.

Where does this hypothesis lead us?

The current data provides preliminary empirical evidence to the hypothesis – “agent-training->more compliance->higher trust->more transaction”. Nevertheless, it does open up the probability of more nuanced inter-linkages, perhaps on what changes training can bring along and/or other parameters that affect compliance, customer trust, and number of transactions.*** While more data will help us understand and explore these nuances and inter-linkages, for now, we see a clear theory that identifies changes that an agent witnesses due to agent training – thereby answering the question we started with. We will be closely watching evidence from further ANA research to evaluate how this hypothesis may be supported further.

* For Senegal and Uganda, the profit numbers aren’t statistically significant.

**Compliance is measured by the display of tariff sheets, agent’s ID, grievance redressal number, call centre number, provider sign, provider colours, etc., and performance is measured by transactions and profitability of agents

***We know training might not be the only cause for better compliance. Monitoring visits by the provider, for example, is also likely to impact agent compliance. Compliance is likely not the only factor that builds customers’ trust in DFS. Service reliability, for example, influences a customer’s trust too. Similarly, external factors, such as ATL and BTL marketing by the provider, also contribute to a customer’s trust in DFS.

Billions of people around the world are required to meet know your customer (KYC) norms to avail of services considerably important to their lives. Yet, widely prevalent archaic methods for KYC come in their way. e-KYC, a fully digital solution, leveraging resident Indians’ centrally stored demography details and biometrics (fingerprints and/or iris recognition) is changing how KYC has been done for ages. This blog examines how e-KYC is an established and proven solution and (together with the India Stack presents a compelling and transformative blueprint for a majority of the emerging markets to consider.

The payment system in any country needs to pass the litmus test of safety, security, soundness, efficiency, and accessibility. In order to address all these, payment systems have evolved from barter to currency, to digital systems. Read how India is witnessing enormous change in the payment systems, disrupting the monopoly of physical/paper-based system by electronic ones.

“Fintech” – an intersection of financial services and technology – is taking the traditional financial world by storm. Indonesia is no exception, with a fast-evolving ecosystem that includes a host of financial services offered by new generation fintechs.

Indonesia is the fourth largest mobile market in the world with 339.9 million connections – a SIM penetration of 131%! 43% of Indonesians already own a smartphone. Furthermore, Indonesia is going “mobile-first” with 64.1 million out of a total of 88.1 million users accessing Internet through mobile devices. This is fuelling social media usage by platforms such as WhatsApp, Facebook, Blackberry, Line, Path, etc. This trend is also leading to explosive growth in electronic and mobile commerce, with big names such as Alibaba, Softbank, Sequoia, Rocket Internet, and Temasek backing local ventures. In contrast, only 36% of 250 million Indonesians have access to formal financial services.

Keeping these technological advancements in context, the blog highlights how Indonesia is well placed to leverage “fintech” towards the cause of financial inclusion.

Globally, mobile money services are being offered primarily over the counter (OTC). This underlines the demand for readily available, quick and convenient fund transfer services. Even though OTC is a well-established concept, there are varying views on what actually constitutes an OTC transaction. Moreover, OTC in India differs in some respects from OTC services in other countries. The blog outlines OTC in India.

It is always dangerous to make predictions in an industry which is expanding and evolving rapidly, so it is with trepidation that I now do so. The blog presents predictions in Digital Financial Services based on market insights and observations from working many years within the mass retail financial sectors and in Digital Financial Services.

The Helix Institute of Digital Finance recently concluded the second wave of Agent Network Accelerator (ANA) study in Bangladesh which found signs of growth in the digital financial services landscape in Bangladesh on all the key performance metrics*. The number of providers, agents, and users –all have increased since the previous wave of the study was conducted in 2014 and the research indicates that the Bangladeshi market is poised for the next level of digital financial services. Service providers are likely to lead this wave of change, while the regulator – Bangladesh Bank, and agents will play their respective parts in contributing to it. You may call us victims of optimism bias, but study findings and interaction with various stakeholders clearly indicate that the market already has a good appetite for better digital financial services – or DFS 2.0, as we refer to it in this blog.

Providers will lead the change

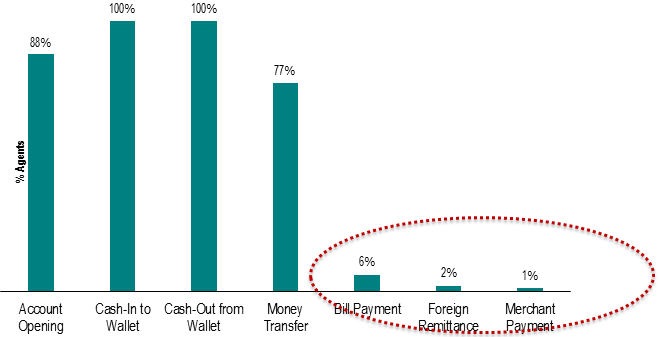

The current DFS product offering in Bangladesh is limited to the basics – account opening, cash-in/cash-out transactions, bill payments and money transfers, although bill payments and merchant payments have a negligible presence in the product suite (Figure 1). Compared to other factors that contribute to successful DFS ecosystems – players, agent networks, technology, customers, and products, the Bangladesh market is still nascent, in terms of the range of products and services. The country shows positive growth trends and is comparable to other ANA countries in terms of the training and liquidity management of its agent network.

More Bangladeshis are embracing DFS and it is likely that providers may want to offer them more than the basic wallet and P2P services. We predict that providers will begin to focus on diversifying and offering more sophisticated products.

Figure 1: Products offered by by Agent in Bangladesh

Agents also noted that “individual clients’ demand for (DFS) service is not regular”. This perception could be largely due to the P2P nature of the market which is not predictable as it is governed by a degree of migration in the market. The demand might become regular and/or predictable if there are more use-cases in the form of sophisticated products by providers that motivate more usage and uptake of DFS offerings.

As DFS market continues to evolve, acquiring a large customer base that understands and uses digital financial services is critical (Davidson and McCarty). We believe that the Bangladeshi market has reached this critical juncture and providers have attained a customer base ready to use more sophisticated financial services.

Bangladeshi providers have much to learn from the success of African markets where digital financial services have successfully offered savings and credit services – KCB-MPESA, M-Shwari, Equity Bank, are all shining examples. There are also examples of agents offering savings, credit, and insurance products. These experiences, irrespective of whether they were successes or failures, provide immense literature and learning on customer behaviour towards a credit product or role of agents in offering insurance products. This will be hugely beneficial to the providers in Bangladesh in designing both products and strategies.

Fortunately, all DFS providers in Bangladesh are banks or their subsidiaries. Unlike non-banking providers who lack expertise in the area, banks, in general, are far more proficient in designing banking products. The changing landscape of new product development that involves big data and Behaviour Economics principles will further help banks to design products that are tailored to meet the critical financial needs of customers. All these factors add weight to our optimism about DFS 2.0 in the country.

Agent optimism will support the launch of more complex financial products

The ANA study found that Bangladeshi agents are the most optimistic ones among all the ANA markets – almost all agents see themselves continuing as agents for another year. About one-third (31%) of agents in Bangladesh are high performing, that is, they conduct more than 1.5 times the country median level of transactions. Agents are critical to the development of digital financial services, and a happy army of agents is one of the most useful assets for a provider. There is, therefore, a good probability that agents in Bangladesh would be willing to promote and service complex financial products. The road to agent management, however, is not without its own challenges, as with more sophisticated products, agents will be more prone to fraud. The data shows that fraud has risen three percentage points – from 19% in 2014 to 22% in 2016.

Support from the Regulators will be key

It is worth noting that the regulator in Bangladesh supports both – mobile financial services (mostly wallet based payments offered by the banks) as well as agent banking (to promote bank-branch like experience for customers). We reckon that the competition for market share between these two models will catalyse the development of more sophisticated products. The objectives of both models are largely the same – increasing the penetration of financial services and achieving financial inclusion. Although there is a slight variation in the basic modus operandi of the two models, agents appointed by the bank play a key role in both of them during customer interaction. The best practices of agent management have already been established for the market, therefore, the next phase will be about providers competing to get the customer value proposition right. It is time to wait and watch how providers who offer either MFS (for example bKash) or agent banking (for example, Bank Asia), try to win customers over; and how provider(s) who offer both type of services (for example, Dutch-Bangla Bank) consolidate their value propositions. We believe that these two guidelines (agent banking and revised mobile financial services), will create opportunities for developing more complex financial products. The push for DFS 2.0 will, therefore, be greatly determined by how regulation facilitates this while ensuring customer protection at the same time.

Markets evolve in terms of the products they offer; Kenya evolved from ‘send money home’ to ‘payments’ to ‘get credit on the phone’ and beyond. India evolved from no-frills accounts to Basic Savings Bank Deposit Accounts to Jan Dhan Yojna accounts. In Bangladesh, the stage is now set for the evolution of the DFS ecosystem to take place.

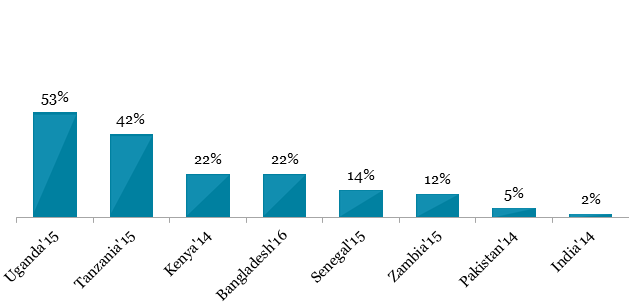

When it comes to fraud in digital financial services (DFS), stories from Uganda will surely arise: be it the infamous case of internal collusion within an MNO or the highest rates of agent-reported fraud across all countries where the Helix Institute has conducted research (Figure 1). The first blog in this series focused on who and what it would take to get DFS industry collaboration on fraud in Uganda off the ground. This blog proposes five avenues where DFS providers can step up the fight against fraud in DFS.

Figure 1. Agents reporting Fraud: ANA Research Countries

Source: ANA Uganda 2015, The Helix Institute of Digital Finance.

Five Ways to Tackle Fraud

Conduct periodic mass education campaigns. These are critical for creating and sustaining awareness about fraud among customers and agents alike. Ugandan providers should continue to invest in above-the-line communication on the variety of fraud risks, ideally in partnership with Bank of Uganda and the media. As the guardian of consumer protection, the Bank of Uganda has taken successful initiatives to educate the public on how an agent is expected to operate. Its continued involvement in such efforts would bolster their credibility.

A good example is Safaricom’s campaigns. Safaricom used multiple channels – from SMS blasts, newspaper ads, to skits and radio spots in local dialects – for targeted communication about fraud. Furthermore, its ‘PIN Yako Siri Yako’ (Your PIN Your Secret) campaign has increased user awareness on keeping their PIN number secure.

Revamp internal systems and processes to ensure adherence to clear protocols.

Providers may need to clarify their operational protocols for fraud identification, management and reporting and relay this to all of their stakeholders—from agents and aggregators/master agents to sales and distribution managers, to ensure a shared understanding of the protocols.

Essential within these protocols are effective complaints and redressal mechanisms accessible 24/7 in local languages, with dedicated customer- and agent- hotlines. In Kenya, some providers accept customer complaints via social media, which given their open nature, can result in faster turn-around and keep other customers informed about the lastest fraudster tricks.

Regardless of the medium, these mechanisms should adhere to clear procedures for transaction repudiation, complaint escalation, and logging customer- and agent-reported fraud incidents. Aggregate statistics on fraud should be regularly transmitted to internal and external sensitisation channels to ensure that the latest information is integrated into consumer education as well as agent and internal staff training.

b. According to a study by Deloitte, the primary root causes of mobile money fraud are internal control failures related to governance, IT, and continuous monitoring. Providers should strive to implement preventative and detective safeguards. Some examples of these measures, among others, include:

Disabling incoming SMS/calls from unauthorised numbers on transaction SIM cards;

Allowing access to web terminals from secure terminals only;

c. Robust analytics are the backbone of fraud monitoring and management. However, Ugandan providers have not yet fully developed their capacity in this area. Data systems and analytics should include at a minimum: transaction pattern tracking with time/location stamps and reference numbers (with automatic blocks applied to customer and agent accounts flagged for suspicious activity), float and cash balance monitoring, as well as periodic commissions’ analysis to detect agent-perpetrated fraud.

One example is recent collaboration among leading Ugandan providers to claw back commissions for direct deposits by analysing transactions’ locations and time stamps. This was done using BTS/Booster detection – deposits withdrawn from the same account in a different location within several minutes were not remunerated.

d. Automation can significantly reduce opportunities for fraudulent meddling by agents and employees. Providers should prioritise automating transaction reconciliation (B2B, C2B), tariff collection, and aggregator/agent commission pay-outs. Enabling customer cancellations, modelled after M-PESA’s Hakikisha, could help curb customer-facing fraud. To further protect customers, systems could auto-generate SMS warnings to those using common PINs like 0000 or 1234.

Improve staff and agent network management through enhanced training and monitoring, as well as stricter recruitment and contracting.

Training. It’s encouraging that Ugandan providers are already training their agents and staff on fraud. Providers are formalising training curricula through Training-of-Trainer manuals. As these are compiled, they may want to ensure that manuals include a comprehensive fraud typology. This can include practical prevention tips such as:

Complying with customer KYC;

Keeping agent materials secure;

Picking difficult to guess passwords;

Identifying counterfeit currency identification;

Adhering to customer privacy standards;

Handling customer complaints; and

Regularly updating the agents and staff on the latest types of fraud and prevention strategies.

b. Monitoring. Providers have already started using agent support and monitoring visits as an opportunity to address the issues of fraud and operational compliance. Such visits are a convenient, periodic opportunity to check the level of agent awareness and compliance to KYC procedure, inspect mandatory tariff disclosure, ensure password security, and check for counterfeit currency. They can also be used to inform agents of emerging fraud trends and best practices in fraud mitigation elicited through internal redress channels, feedback at conventions, or experience-sharing provider fora. Of course, staff conducting such visits must also carry proper identification, given cases where agents have been defrauded by fraudsters posing as provider support staff in the past.

Visits by a provider or third-party personnel could be supplemented with mystery shopping exercises by the regulator to check compliance. Providers may further consider enabling aggregators/master agents to access their agent transactions via a specialised portal. This could boost their ability to track sub-agent performance and identify unusual activity.

c. Agent Recruitment and Contracting. The Bank of Uganda’s Mobile Money Guidelines already dictates minimum agent KYC credentials. However, given the prevalence of fraud in the country, providers would greatly benefit from expanding these criteria and revisiting their due diligence process to include background checks. These revised criteria and due diligence should not be limited to agents alone but should be extended to all employees, including aggregators/master agents. For example, Safaricom requires agent applicants to submit a certificate of good conduct from the Criminal Investigations Department of the Kenya Police.

Additionally, employee, aggregator and agent contracts must be reviewed to explicitly state the obligation of adherence to operational standards – in particular, those pertaining to fraud (e.g. customer KYC, transaction logging, tariff display requirements) – as well as grounds for dismissal.

Factor fraud into product design. This will become increasingly important as more complex bundled products, such as digital credit, savings, and insurance products are introduced.

Greater product sophistication, delivered via partnerships between different financial service providers, could increase the opportunities for committing fraud. It will be crucial that all business partners involved are trained in fraud mitigation and have compatible fraud mitigation systems.

Prior to the roll-out of these products, provisions for complaints and redressal mechanisms – including division of roles and responsibilities, as well as communication channels must be clarified with the relevant staff receiving corresponding, specialised training. For example, in Tanzania, Commercial Bank of Africa (CBA) and its MNO partner, Vodacom, have agreed that all complaints regarding CBA’s product, M-Pawa, will be handled by Vodacom call centre staff, who receive specialised training from the bank.

Enhance regulatory enforcement and the prosecutionof offenders. While this recommendation does not pertain only to DFS providers, ensuring compliance to KYC is a crucial preventative step to fraud. Only 2% of Ugandan customers show identification when conducting a transaction, even though 84% have the requisite ID. Combating non-compliance on this particular issue must be done in collaboration with the regulator and the National Identification and Registration Authority.

Closer collaboration with the Uganda Police Force will ensure timely investigation and prosecution of fraud perpetrators. Ugandan providers have called for a common database of blacklisted agent employees to track fraudster handlers. Such an endeavour could be spearheaded by the regulator in partnership with law enforcement and National Identification and Registration Authority. The State Bank of Pakistan’s online database, AgentChex, enables the regulator to track agent transactions and flag those implicated in the fraud. It would be essential that such information is shared among all DFS stakeholders.

Fraud is an ever-evolving phenomenon and concern in Uganda. We hope the analysis of ANA data and our qualitative research offers some practical advice as to where providers may enhance their efforts to combat fraud effectively. The Helix Institute is vigilantly watching this space and equips the DFS community with preventative and mitigation strategies to address fraud in its Risk and Fraud Management Training Course.

The Helix Institute of Digital Finance would like to thankFSD Ugandafor funding and supporting the 2015 ANA research in Uganda.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

When it comes to fraud in digital financial services (DFS), stories from Uganda will surely arise: be it the infamous case of

When it comes to fraud in digital financial services (DFS), stories from Uganda will surely arise: be it the infamous case of