The second assessment (Wave-II) of BMs under PMJDY was conducted by MicroSave during April-May 2015 with an objective to provide a comparable analytical framework with Wave-I. Wave-II covered a total sample of 1,700 BMs and 4,514 PMJDY customers in similar geographies (as Wave-I) of 9 states and 41 districts.

Blog

Snapshots: PMJDY wave I assessment

MicroSave, with financial assistance from Bill & Melinda Gates Foundation (BMGF), designed three assessment surveys to understand the coverage and quality of Bank Mitrs (BMs) across a sample of Sub Service Areas (SSAs); and to understand customers’ experience with National Mission on Financial Inclusion more commonly known as Pradhan Mantri Jan Dhan Yojana (PMJDY). The objective of such assessments was to provide data and insights to the Department of Financial Services (DFS), M/o Finance for supporting the rollout of PMJDY.

Snapshots: PMJDY wave II assessment

Wave-II observed an improvement in most of the parameters over Wave-I and was more comprehensive as it covered additional information on other some aspects of BMs such as fixed and variable commissions; device enablement; infrastructure; fixed and variable costs incurred; product portfolio offered, capacity building; and satisfaction levels etc. The customers were additionally asked about their preference for a transaction point; reasons for such preferences and; problems faced while conducting the transaction at BM outlet etc. Wave-II provided bank wise and state wise comparisons on major parameters covered during wave-I to track the progress of PMJDY on ground implementation.

Over the Counter (OTC) Money Transfer in India: The Remittance Silver Bullet for Migrants

“Ready money is Aladdin’s lamp”― Lord Byron

Globally, mobile money services are being offered primarily over the counter (OTC). This underlines the demand for readily available, quick and convenient fund transfer services. For instance, 90% of WING’s transactions in Cambodia, 70% of EasyPaisa’s transactions in Pakistan, and 50% of bKash’s transactions in Bangladesh are OTC based. Due to market dynamics, customer pull and trust deficiencies, OTC transactions have been preferred, as highlighted in MicroSave’s blog, Beware the OTP Trap. Some other publications have, in detail, explored the prevalence, causes, and implications of OTC transactions in other countries, such as Pakistan, Bangladesh, Kenya and Uganda. Even though OTC is a well-established concept, there are varying views on what actually constitutes an OTC transaction. Moreover, OTC in India differs in some respects from OTC services in other countries. So, let’s start by outlining OTC in India.

What is OTC in India?

A simplified definition of OTC which is more appropriate for the Indian context, is: “Any transaction that is conducted by the agent on behalf of the customer” or an “assisted transaction”. This definition also encompasses the following:

a. The customer is not required to have a mobile wallet or a Mobile Station International Subscriber Directory Number (MSISDN; in simple terms, owning a mobile phone number) to use the service.

b. The customer may not have any knowledge about a wallet being opened on their behalf (this case has been observed commonly).

c. The agent is the “only” actor who conducts the transaction, i.e., there is no self-use of a wallet by the customer (similar to other countries).

Given the current regulations in India, which allow cash-out through full KYC bank accounts only, even transactions that are made OTC at the origination stage, fall under the ambit of formal financial services at the destination.

While sending the funds, however, two distinct scenarios are possible. First, the agent may use his personal account (or that of an acquaintance) to send money, without informing the customer about the process. The entire transaction process is carried out by the agent, with the sender only providing the beneficiary’s account number. Second, the agent may open a wallet for the customer (even without their knowledge or understanding), and then use that wallet to transfer the funds. The sender thus receives confirmatory text messages when the transaction is initiated and when it is completed. He associates these messages as part of the provider’s service offering, unaware that these are associated with the wallet opened in his name.

an acquaintance) to send money, without informing the customer about the process. The entire transaction process is carried out by the agent, with the sender only providing the beneficiary’s account number. Second, the agent may open a wallet for the customer (even without their knowledge or understanding), and then use that wallet to transfer the funds. The sender thus receives confirmatory text messages when the transaction is initiated and when it is completed. He associates these messages as part of the provider’s service offering, unaware that these are associated with the wallet opened in his name.

Thus, in an Indian context, any transaction where the agent’s account (or agent’s associate account) is used to send money without informing the customer, may be classified as informal OTC. However, when a customer’s account is used to send money (even without his explicit knowledge or understanding), the transaction can be termed as a formal OTC transfer.

Outlining the transaction process

MicroSave conducted research to understand the experience of customers using OTC remittance services in India. By carrying out mystery shopping exercises, we are able to define a common process that is followed when a typical OTC remittance transaction takes place. This process has been illustrated in the figure below.

i. Opening customer’s wallet

i. Opening customer’s wallet

The sender/remitter walks into the agent outlet with cash in hand with the purpose of remitting the money. Generally, the agent notes down the mobile number of the sender (in some cases, the agent uses his own mobile number, but because of caps put on the number of daily transactions from any one account, this is a rare occurrence). The sender’s mobile number is then used to open a wallet on the provider’s portal (an internet website used by agents to open wallets, and transact after signing in with their credentials). However, this is often done without the consent and knowledge of the customer. Consequently, the senders, who visit (different) agents associated with different providers, have multiple wallets opened using the same mobile number. This process of customer acquisition on behalf of payment service providers is leading to an overstatement of the number of unique users who are actually using DFS for remittances.

The sender, unaware that a wallet is opened, believes that the mobile number will be used to receive a confirmatory text message via Short Messaging Service (SMS) from the provider. The agent informs the sender that this text message will apprise him/her of the status of the transaction.

We observed that a very few agents, working for different providers, conducted transactions without the customer’s mobile number. In such cases, the agent used a mobile number belonging to someone else (or, in rare cases, their own), which is already registered. This number was never shared with the customer. In lieu of the confirmatory text message, the sender is provided with a printed or written receipt, with details of the transaction. However, these cases are very rare, as most customers using these channels own mobile phones or provide phone numbers belonging to their families or friends.

ii. Recording receiver’s details

Once the wallet is opened, the agent asks the sender for recipient’s details at the destination point. These details always include:

- Complete name of receiver,

- Name of the bank in which recipient holds an account, and

- Bank account number of recipient.

There are several other fields that should be filled up (but are not mandatory) by the agent such as IFSC code, bank location, and relation between the receiver and sender, among others. However, in order to save time and for fear of losing customers, who may not have/remember such information, some agents randomly fill these details. As most transactions are initiated using Immediate Payment Service (IMPS) system (for reasons highlighted below), these incorrect details do not affect the success of transactions.

iii. Conducting the transaction

All Indian providers’ portals can use both IMPS and National Electronic Fund Transfer (NEFT) to conduct money transfer services. On some portals, agents can view the downtime status of IMPS. When IMPS is down, these agents use the NEFT service to remit funds.

However, IMPS is the preferred system, as the transactions occur on a near real-time basis. However, most agents believe that regional rural banks (RRBs) do not support IMPS and, hence, they prefer to use NEFT when transferring to RRB accounts.

iv. Receiving confirmation of the transaction

Once money has been transferred via the portal, a text message is received on the phone number provided by the sender. Some providers’ systems also send the agent a text message confirming the transaction. This communication generally happens on a near real-time basis. The sender uses this text message to inform the receiver about the transaction status. When a customer does not have a mobile number, he/she receives/asks for a printed or hand-written receipt from the agent as a proof of the transaction. Next, the sender communicates with the receiver to know the status of the transaction. The receiver then visits either the bank/agent branch or an automated teller machine (ATM), and confirms the transaction status to the receiver. In instances where the receiver does not receive the funds, the sender (at times, using the receipt) follows up with the agent.

Most agents provide a receipt to their customers when asked. The agents print these receipts themselves. These receipts typically do not mention the provider’s name. The receipt helps customers in two ways. First, it acts as a proof of the transaction for the customer. Second, in case the receiver notifies the sender of non-receipt of funds (if the transaction has failed or been delayed), the customer brings this receipt to the agent, who can then check the status of the transaction.

v. Withdrawal of funds by the recipient

The sender, after receiving the text message confirming the transaction, informs the receiver about the transaction status. Once the transaction is successful, the receiver then has three options to access the funds:

- S/he can visit the bank branch in which the account is held and withdraw the funds;

- S/he can visit an agent (Business Correspondent ― BC) outlet, to withdraw the funds; or

- S/he can use a debit card to withdraw the funds from an ATM.

Of these different methods, ATM cards are increasingly preferred at the destination points of remittances. The major reason for this shift is the PMJDY scheme, which provides RuPay debit card to all account holders.

Even though there have been a slew of technological innovations to allow migrants to remit funds themselves, without reliance on a third party (such as an agent), their uptake has been very, very slow. OTC providers offer a fast, secure, and reliable service at a nominal cost to the customer. These three attributes are the most important needs of a typical migrant who wishes to remit funds home without the worry associated with a financial transaction.

Now that we have an understanding of how OTC works in India, in our next blog, we will present the findings from our mystery shopping and the experience of customers, by presenting an experience map for a typical OTC transaction.

Time for Action! Customer Service, Protection and Trust in Indian Digital Financial Services

|

MicroSave’s research (funded by the Omidyar Network) into customer protection, risk and financial capability in India shows that Gayatri’s experience is not uncommon across India.

India is a country committed to achieving full financial inclusion. The recent policy-push under the PMJDY programme and India’s commitment to Better Than Cash Alliance shows this intent. However, because of its sheer size and geographic and ethnic diversity, providing access to quality financial services, especially at the base of the pyramid, remains a challenge. MicroSave’s ANA India Survey report states that “India is a country with 1.2 billion people, 29 states, 100+ Agent Network Managers (ANMs), five major telecoms, 27 public sector banks, 23 private banks, and 100+ rural and cooperative banks participating in delivery of Digital Financial Services (DFS)”.

The Reserve Bank of India advised banks to open “no frills” account way back in 2005, and there have been a number of enabling (but sometimes conflicting) regulation and policy-pushes since then. However, the growth in active bank accounts has been slow and beset with a number of issues ― leading to account dormancy levels of 48%.

And the experience of DFS for both agents and the customers that they serve has been extremely mixed. There has been high churn amongst agents, who are often poorly trained, supported and remunerated; as a result, customers, who like the convenience of a local DFS outlet, are often unsure about its reliability. As with many deployments across the globe, it is basic hygiene factors, like system reliability and agent illiquidity that are primarily responsible for the lack of trust in DFS. These are seen to be both frequent and high-impact in nature … and ironically, at present, theft, robbery and fraud are viewed as both infrequent and low-impact. Our qualitative work suggests that these are low-impact because most customers have yet to experience them … this may well change over time as highlighted in Fraud in Mobile Financial Services.

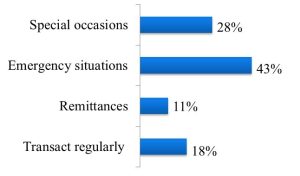

MicroSave field research highlights two contradictory facts that further indicate the fragile nature of DFS in India. While 85% of the DFS customers said that they would recommend DFS to others, they mainly treat it as a back-up option. While customers appreciated the accessibility and ease of use of DFS, they did not really trust it enough to use it regularly – see bar chart highlighting the use of DFS services.

The Indian context reflects a number of conditions highlighted in the MicroSave paper on fraud. The paper notes that weak processes, poor compliance monitoring, and poor customer awareness are key enablers of fraud. Our research shows that all of these are present in India. At present, there are not many reported risks or loss of funds; however, based on current conditions, these are likely to emerge as the system matures and grows

Furthermore, customers’ high trust in, and dependence on, agents for knowledge and conducting assisted transactions, coupled with their limited understanding of, and opportunities for, recourse may lead to a number of agent perpetrated frauds like:

- Unauthorised access to customer’s transaction PIN

- Imposition of unauthorised customer charges

- Split withdrawals (thus increasing commissions earned)

- Agents encouraging customers to leave money with them and then absconding (see box)

|

It is time that providers focus on addressing these customer service and protection issues – see Solving Customer Service Issues in Digital Finance – Can Do, Must Do. Doing so is essential to build trust in DFS and thus stimulate uptake and regular usage … and to prevent widespread fraud and loss for customers.

Connecting the Dots: Putting Risk, Customer Protection, and Financial Capability in Perspective

Risk in Digital Financial Services (DFS) has the potential to derail the financial inclusion agenda. If not managed in time, it can reduce trust, resulting in a vicious cycle of poor uptake of products and services, poor profitability, and thus poor implementation. This paper presents the findings on three inter-related concepts – Risks, Customer Protection, and Financial Capability in DFS at both the customer and the agent level. The vulnerability context in which people operate directly influences the risk profile of the customers as well as the frontline agents. Most of the risks identified in this research were operational in nature and can be resolved relatively easily. However, their expression, in terms of service denials and potential manifestation of fraud, in an environment with limited financial capability and high level of trust of the agents, is potentially dangerous.