In the blog “NBFC-MFIs As Business Correspondents – Who Benefits? Part-I” we highlighted the range of benefits for both NBFC-MFIs and banks in arrangements under which NBFC-MFIs operate as BCs for banks. In“NBFC-MFIs As Business Correspondents – Who Benefits? Part-II” we discussed the advantages and disadvantages of the model for NBFC-MFIs.

But of course, the devil is in the details. So what will it take to make this happen in a way that is mutually beneficial for both MFIs and banks?

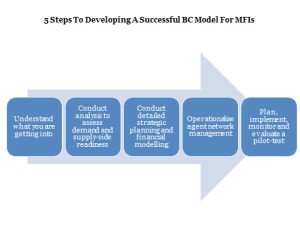

Built on years of experience of supporting MFIs (including some mass market market-focused banks) to plan for and operate as agent network managers, here is MicroSave’s step-by-step guide:

- Understand what you are getting into

There are four ways in which MFIs participate in a digital financial ecosystem. These include:

- Building a digital financial system on its own (not a real option in India!).

- Act as an agent/agent network manager for an e-money issuer (usually a bank or an MNO).

- Using an established digital payments system (for example an MNO-run mobile money network) to deliver its own products and services.

- Using mobile phones as an information sourcing (for example client enrolment and loan origination) and sharing mechanism (for example on repayments due and made) and for other non-cash purposes.

| MicroSave will soon run its “Digital Financial Services for MFIs” workshop in India to assist interested institutions to set up DFS initiatives for NBFC-MFIs (if you are interested to pre-register please send a mail to Garimasingh@MicroSave.net). The workshop provides insights into the costs and benefits of digital financial service adoption in the context of microfinance and assesses the capability of individual MFIs to successfully rollout digital financial services. It will also provide useful information with regard to the opportunities and challenges of digital financial services for MFIs. |

-

Conduct analysis to assess demand and supply-side readiness

Conduct a baseline qualitative assessment to gauge the initial capabilities and ground situation of your MFI on key aspects that will have a direct bearing on the success of your efforts to effect the significant changes that participating in a digital financial ecosystem will entail:

- Willingness of the client base to switch to digital financial services (DFS) channel to conduct loan repayment and savings deposit/withdrawal transactions. It will also seek to understand the extent of the processes that the clients will be comfortable adopting under the DFS channel. Essentially you will need to be able to answer all the questions highlighted in MicroSave Briefing Note # 101 Mobile Money – Questions That Your Clients Will Ask You.

- Mobile literacy among the client base: to understand the mobile phone usage pattern and the level of comfort and acceptance in using various functions of a mobile phone among different client segments.

- Institutional capacity assessment: to gauge the level of preparedness of the institution to adopt DFS-enabled operations. This will take into account staff’s understanding and level of comfort with DFS transactions, their opinions on client acceptance of DFS as a channel for loan transactions, back-end systems and staff skill capacities to manage DFS-enabled operations.

Supply-side assessment of the local DFS market: to gain a quick understanding of the various DFS solutions available in the states where your MFI operates and which of the available ones can be the best fit; also assess the capacity of the existing available DFS agent networks in terms of liquidity management, spread and density of agents to serve your client base.

-

Conduct detailed strategic planning and financial modeling

Using the findings of the baseline assessment, the MFI should organize a workshop involving key personnel from each department and associated consultants. Representatives from potential DFS providers should also be invited to discuss possible terms of engagement – see MicroSave India Focus Note 80 Driving Viability for Banks and BCs. This workshop will aim to draw a detailed strategy for the pilot project and also to use the platform to communicate the idea to all the departments. The deliverables at the end of the workshop would be, but not limited to:

- Decision on the business model: whether to leverage on an existing DFS provider’s network and technology platform or to become a business correspondent (agent network manager) for a bank. In case of the former, the decision on the potential DFS channel partner and description of the overall business model of the MFI to incorporate the DFS channel of operations. If the NBFC-MFI decides to become an agent network manager, detailing of the subsequent steps to acquire the BC mandate from a bank will be essential. This will also involve understanding how and how much a BC will be paid – see MicroSave India Focus Notes 71-73 Sustainability of BC Network Managers (BCNMs) in India – How Are BCNMs Paid? And Sustainability of BC Network Managers (BCNMs) – Review of Commission Structures and Sustainability of BC Network Managers (BCNMs) – Business Scenarios and its Effects.

- Decision on the products to be delivered: which products will be sold and serviced through the agent network has a profound effect on the profitability of the agent network manager and the front line agents themselves – so this needs to be defined by the partners up-front. See MicroSave India Focus Notes 97 & 98 How to Make Optimum Use of Agent Networks (1/2) and How to Make Optimum Use of Agent Networks (2/2).

- A detailed strategic business plan: MicroSaveKOGMA matrix (Key Objectives, Goals, Measures, Activities) for this to drive real action and facilitate the change management process. This will also need to address the risks and challenges highlighted in NBFC-MFIs As Business Correspondents – Who Benefits? (Part-II)

- Financial and operational projections: and thus pricing and commission structures. See MicroSave Briefing Notes # 106-108 Pricing for E/M-Banking and Incentives for E/M-Banking Customers to Drive Usage and Incentivising E/M-Banking Agents.

4. Operationalize agent network management

The cost and complexity of building and managing a sustainable cash-in/cash-out (CICO) agent network across a broad geography is consistently under-estimated by providers across the globe. MFIs will experience additional challenges not least of all because their processes are credit-focused and banks are likely to outline (but not detail) a series of process that their risk management/statutory compliance departments will require. In addition, MFIs may struggle to assess the risks involved in both the delivery of a wider range of products and in the use of digital channels to do so.

MicroSave’s Agent Network Accelerator project works with agent network managers in eight leading markets across the world to understand address many of these challenges.

Key decisions required from MFIs acting as BCs will include:

- The structure or “hierarchy” of your agent network – see MicroSave Briefing Notes # 136 and # 137 Structuring and Managing Agent Network – I and Structuring and Managing Agent Network – II.

- The process for identifying, recruiting, training and on-boarding your agents. For a discussion of agent training see MicroSave Briefing Notes #135 & 138 Training E/M-Banking Agents: What is Missing? and Implementing Training for E/M-Banking Agents.

- How you will manage agent liquidity and rebalancing between e-float and cash as the transactions occur MicroSave Briefing Notes #78 M-Banking Liquidity Management.

- How you will monitor and support your agents – see MicroSave Briefing Notes # 73, 74 & 110 Managing Agent Networks to Optimise E- and M-Banking Systems Part-1 and Managing Agent Networks to Optimise E- and M-Banking Systems Part-2 and Managing Channel Satisfaction in Agent Banking.

| To get a really good handle on this, ideally MFIs should send participants to attend The Helix Institute of Digital Finance’s Core Agent Network Accelerator training workshop. This course is invariably hugely over-subscribed so if you want to pre-register, please contact Annabel@MicroSave.net. |

How you will manage customer service and satisfaction – MicroSave Briefing Notes #129 & 130 Customer Support for E/M-Banking Users and Customer Service Through Call Centres .

-

Plan, implement, monitor and evaluate a pilot-test

This phase will be focussed on establishing all the back-end systems and HR resources necessary for the rollout of the pilot phase. The key tasks during this phase will be the following:

- BC Transformation Planning and Change Management – building on the strategic business plan’s KOGMA analysis, including a detailed timeline of major activities and roles/activities assigned to individual staff/ consultants.

- Finalization of contracts with the mobile money (DFS) providers: The MFI will finalize the services to be availed/delivered and the applicable pricing/revenue/ commission systems with the DFS provider/banks. The resulting contract should describe in detail, among others: Each entity’s roles and responsibilities in the project,

-

Method and payment mode of commission/ revenue,

-

Service quality of software/ hardware platforms (service level agreement), and back-end support structure.

A detailed project implementation plan describing timelines and corresponding deliverables, etc. will be drafted jointly with the selected DFS/bank entity to ensure timely execution of the project activities. In addition, unless it is able to piggy-back on existing “pay bill” functions of providers, the MFI may need a separate USSD code. This will require careful negotiation with the MNOs.

- Negotiation and contracting with IT providers, installation of the IT Module: In addition to DFS providers, software providers will also be listed to identify the solution provider for the IT platform the MFI will require for reconciling the DFS transactions on its back-end systems.

- Decision on the selection criteria, and selection of branches for the pilot project.

- Setting targets: both quantitative and qualitative to allow assessment and evaluation of the pilot and define criteria for judging its success (or failure) and thus avoid pilot-test decision drift!

- Detailed definition of the processes and assessment of the attendant operational risks for the digital financial services that will be provided – including a detailed approach to the management of these risks to optimize the risk-efficiency trade-offs. See MicroSave Briefing Note # 115 Process Mapping for Mobile Banking Initiatives.

- Definition of the marketing & communication strategy to promote uptake and usage of the new digital channel by end-users. See the MMT/MicroSave webinar on Marketing E/M-Banking Services for an overview of the issues and opportunities for addressing them.

- Training of staff: on both the digital finance channel and how it changes their roles and responsibilities and on how they will market it to end-users.

- Establishment of the monitoring systems and evaluation team for the pilot project.

If all this looks complex, it is. Moving to a digitally enable system will require detailed planning and painstakingly detailed execution, including a significant change management process.

But help is at hand, MicroSave has years of experience of work on exactly these issues with banks and MFIs across Asia, Africa, and Latin America – including in India itself where we have worked with or are working with the four largest mobile network operators; banks including HDFC, Axis ICICI, State Bank of India, Punjab National Bank and Bank of India; agent network managers including Eko, FINO, SAVE, Oxigen and many others; and MFIs including KGFS, Cashpor, Grameen Koota and Arohan.

Click here for more information on our DFS Capability Statement and Agent Network Management for MFIsbrochure or contact us on info@MicroSave.net.