01:15 – 03:45 – Akhand Tiwari, Partner, MSC – Welcome note and introduction to the schedule – Catalytic interventions for better CICO management.

04:15 – 13:27 – Dr. Pawan Bakhshi, India Lead, Financial Services for the Poor, BMGF – Highlighted the importance of CICO networks and their growth across India and other countries.

14:30 – 30:40 – Anil Gupta, Partner, MSC – Introduced the range of CICO agent personas in India and their journeys through the agent lifecycle. He also highlighted the complex environment in which the CICO agents operate and the variety of support systems they need.

31:56 – 34:12 – Dave Kim, Program Officer, BMGF – Welcome note and introduction of the panelists and three questions to the panelists: A little bit about themselves, a bit about their organization, and if they had a magic wand to solve one problem for their organization, agents or customers today, what would it be.

34:15 – 35:08 – Abhinav Sinha, Co-founder, Eko India – Introduction about himself and Eko India and answers to Dave’s questions

35:19 – 36:10 – Rachit Narang, Head of Strategy and Investor relations, Airtel Payments Bank – Introduction about himself and Airtel Payments Bank and answers to Dave’s questions

37:50 – 42:03 – Airtel Payments Bank pilot video on “Behavior change communication to encourage the use of agent banking among rural LMI women.”

42:05 – 45:37 – Eko India pilot video on “Banking Correspondent (BC) Agent incentives.”

45:45 – 01:16:12 – Dave, Abhinav, and Rachit – Discussed the problems, the intervention design of each pilot, and the impact it had on agents and customers.

47:20 – 52:00 – Abhinav – What drives the belief that Eko has an additional 15 years of work remaining in the CICO space, and how would CICO innovation show up in these 15 years?

53:19 – 56:22 – Rachit – The process adopted by APB to come to the simple and elegant solution of behavioral communication as a result of MSC’s pilot

57:05 – 1:04:20 – Abhinav and Rachit – Did their convictions about agent networks change, or were any of their existing beliefs strengthened due to the pilots with MSC?

01:17:04 – 02:02:00 – Graham Wright, Group Managing Director, MSC; Hillary Miller-Wise, Deputy Director, BMGF; Samuel Brawerman, Partner, Kuunda; Sanchita Mitra, National Coordinator, SEWA Bharat – Identified the integral factors that helped create a formidable and responsible agent ecosystem, specifically by efficiently recruiting and onboarding more women agents and providing agents credit, etc. They also explored how technology can help provide better financing opportunities for agents.

01:17:04 – 01:20:20 – Graham – Introduction of the panelists and welcome note

01:20:26 – 01:26:56 – Hillary Miller-Wise – The key challenges that limit the creation and expansion of CICO networks to offer inclusive financial services to the last-mile

01:29:11 – 01:36:05 – Sanchita Mitra – Challenges in selecting, recruiting, and onboarding women agents at SEWA and building an inclusive agent network

01:38:58 – 01:48:22 – Samuel Brawerman – Financing of agents for agents to meet their liquidity and working capital needs, and how the Kuunda product works and if it needs customizing for women agents

01:48:24 – 02:02:00 – Solutions to what we could do to build inclusive CICO networks and empower women agents in CICO

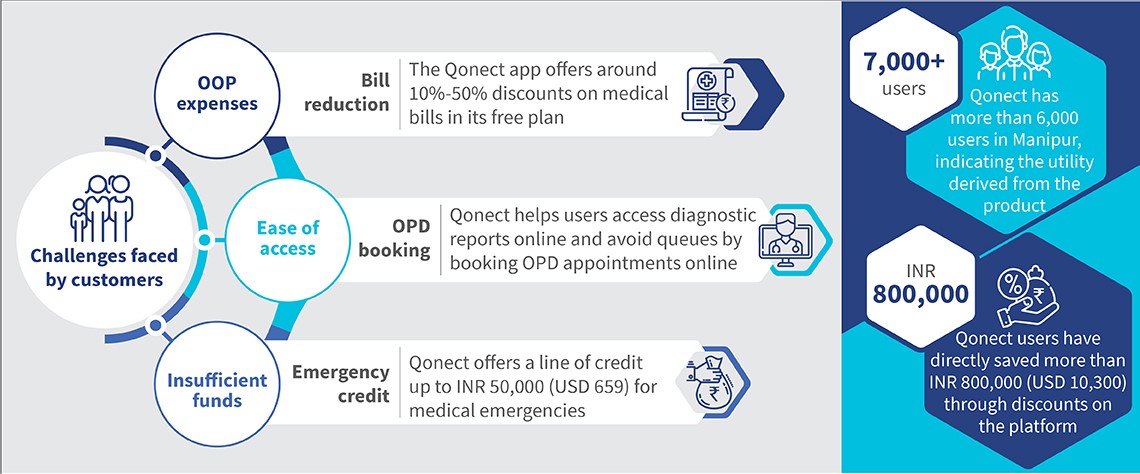

“If I could save 10% of my father’s medical bills, I would not need to ask anyone for money,” Lian Thangvung thought as his phone chimed with an INR 10,000 (USD 132) transfer notification from his sister. A year later, the budding entrepreneur did what few can do—act on his conviction, so others do not suffer. Lian founded Qonect, a HealthTech platform, in Manipur.

Qonect is a subscription-based digital health platform that offers various online medical services, such as discount medical orders and online booking of appointments, and diagnostic services, such as access to labs, archiving, and digital access to diagnostic reports. Personal experiences, an entrepreneurial mindset to solve complex problems, a supportive family, and ambition shaped Lian and fueled Qonect to its current stage.

Born out of empathy and personal experience—the phone call in 2017:

A phone call in 2017 kickstarted Lian’s journey when he heard about his father’s ailment. He immediately rushed to his home state of Manipur from New Delhi. What followed was emotional and formative for Lian and shaped his uncanny mix of grit and empathy. The doctor recommended a CT scan for his father during the diagnosis.

CT scan facilities are difficult to find in Manipur. On locating a facility, Lian found that a CT scan can cost anywhere between INR 8,000 (USD 105) to INR 10,000 (USD 132) in India. Lian did not have enough money to support his father’s diagnosis and treatment. Nor did he have the time to go through the protracted process of taking a bank loan, which had a fair chance of being rejected. His sister’s timely intervention helped Lian manage the crisis at that time.

Lian did not want others to suffer in similar circumstances and started to build solutions for these issues. Out of his efforts, Qonect was born in Manipur in June 2018.

The malaise runs deep—out of pocket expenses have pushed more than 55 million Indians into poverty:

Typical of a developing country, India’s population is also underinsured, leaving large sections vulnerable. Before the pandemic, roughly 8 out of 10 Indians met medical expenses out of pocket (OOP). In rural India, such OOP expenses averaged around INR 816 (USD 11), constituting roughly 12% of non-food expenses. Such high OOP expenses on medical care pushed 55 million Indians into poverty, even before the pandemic.

The COVID-19 pandemic was a double whammy. The cost of ICU hospitalization during COVID-19 was almost equal to nearly 16 months of work for a daily wage laborer or 10 months of work for a salaried or self-employed worker. Various estimates show that the pandemic drove another 32 million middle-class Indians into poverty. At a time, when loss of income rendered most LMI households vulnerable, out-of-pocket medical expenses and the high cost of healthcare were the top two reasons that plunged people into poverty. Such debilitating costs instill fear in patients, and as a result, they avoid medical care altogether, fearing that diagnosis of any acute diseases can break the household’s finances.

Qonnecting the dots—a bridge between healthcare providers and negligent at-risk patients:

Qonect has taken the bull by its horns by solving the problem of rising healthcare costs, starting with one of the most vulnerable and excluded regions of India—the Northeast. Qonect began as a health card in Manipur that offered discounts on medicine purchases, thereby reducing the OOP expenses. But soon, the pandemic hit, and the physical engagement with clients came to a halt.

Lian and his team at Qonect lost no time adapting to the pandemic’s new norms. They went digital to its current avatar—a digital subscription platform. Qonect partners with medicine retailers and negotiates preferential rates for medicines which are passed on to the users as discounts. The subscription amount helps to maintain the technology, as well as in pay the premiums for the insurance offered to the users as part of the plan. Their next objective was to provide fast and affordable financing to users for medical emergencies. Qonect partnered with a lender to offer instant credit for such emergencies. The credit is currently offered through partnership with an NBFC and is based on the credit history and bank account balance of the users. Gradually, Lian and his team have managed to give shape to their vision through the Qonect app.

Lian remains focused on the purpose of Qonect as he says, “Qonect should be the bridge between healthcare providers and people who delay or avoid medical care because of costs.” Qonect has already impacted the lives of vulnerable low-income people in Manipur. Qonect has established the relationship between HealthTech and financial health.

Patients who make OPD bookings through the app save money that would otherwise result in significant OOP expenses, given the hilly and often inaccessible terrain of Northeast India. Furthermore, test results and doctors’ prescriptions can be delivered over the platform, thus saving patients from having to travel to collect these from the OPD. While the subscription model currently offers substantial discounts on medical costs, Qonect plans to offer a completely cashless experience to its customers and provide buy-now-pay-later (BNPL) credit for any medical expense. Such a BNPL product feature will underwrite customers on the basis of their transactions done on the Qonect platform as well as other alternate data points. Such an all-inclusive subscription will fortify the financial and physical health of the households as customers inculcate sustainable and repeatable behavior that reduces negligence and encourages timely attention.

Figure 1: Translating product design to impact

One of the proudest feats for Lian so far has been helping customers save more than a month’s salary equivalent in medical bills. Customer impact is the guiding force that drives product design and business decisions at the Qonect headquarters. The struggle for money and handling the trauma of a medical emergency may have developed the extraordinary amount of empathy that is evident in Lian when he talks about Qonect helping thousands of users in Northeast India get access to timely and affordable medical services.

No shortcuts to success

But, building products based out of Manipur in the Northeast is hardly a walk in the park. Geographical constraints, such as lack of access to infrastructure and resources along with widespread information asymmetry among customers, are daunting barriers for any startup. For example, Imphal, where Lian wants to set up offices, lacks good internet connectivity and suffers from power outages. “Sometimes, I am forced to miss calls with investors or partners because of internet outages or running out of backup during prolonged blackouts,” says Lian. However, Lian and his team have found strategies to overcome each such challenge with their grit.

The government has provided satellite internet at the village panchayat, and Lian, with his elder brother and the village chief, uses this connectivity during consumer internet outages. Such efforts, combined with the network and handholding from CIIE.CO and MSC have helped Qonect beat the odds.

However, an obvious question remains—why go through such difficult paths when Lian can move his offices to Guwahati, the biggest city in Northeast India? Lian’s headstrong conviction reflects in his answer, “I want the young ones from these regions to believe that it does not matter where you come from as long as you have zeal and passion.” No surprise then that Qonect now attracts investors from the metros across India, who frequently fly to Imphal to keep close tabs on Qonect’s operations.

What next?

Qonect’s vision is clear. It wants to be the first startup from Northeast India to expand and provide healthcare services across India. For the immediate next steps, MSC is supporting Qonect in understanding the needs of a diverse set of customers through market segmentation. MSC is also helping Qonect to achieve a product-market fit for LMI customers across various states of India by packaging credit and healthcare in an intuitive subscription model.

In the mid to long term, Qonect wants to develop predictive capabilities to mitigate risks for medical emergencies from preventive and financing perspectives. Apart from delivering impact at scale, Qonect has set ambitious but achievable business goals. The goal is to hit a revenue of INR 300 million (USD 4 million) in the next 18 months.

With Qonect’s empathetic product design and rapid growth to date, no mountain is too high. The future is not far away when a family a medical emergency will be able to afford the best medical attention for their loved ones without the additional concerns of access and funds.

This blog post is part of a series covering promising FinTechs making a difference in underserved communities. These startups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative, co-powered by MSC. #TechForAll #BuildingForBharat

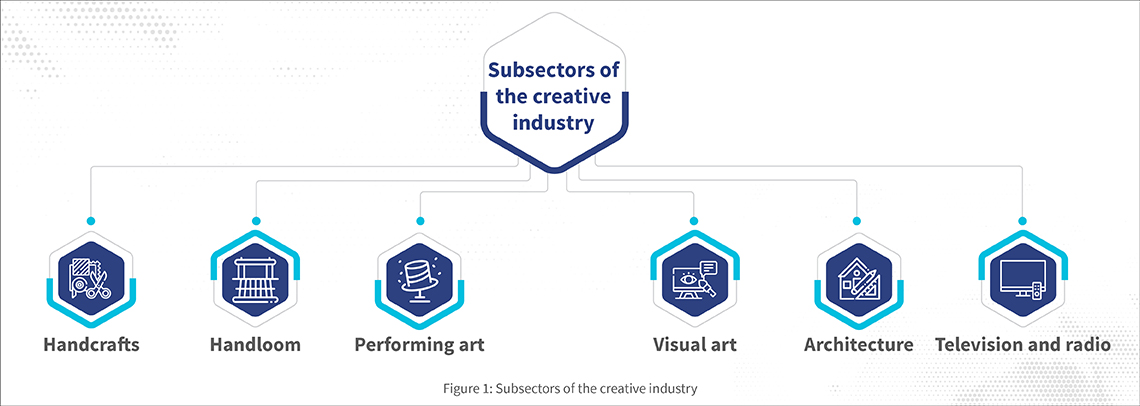

One of the most versatile subsegments of the creative industry is India’s handloom art. Indian handloom weave mirrors the country’s rich culture and heritage that dates back more than 2,000 years. The traditional artifacts depict the region’s geography, history, and rich culture. From Kani in Kashmir to Kasavu in Kerala, from Gujarati Patola to Manipuri Phanek—every area has a signature weave.

Over the past few years, many new-age startups and contemporary brands have emerged to revive the ebbing handloom industry and create demand for their products using technology. One such startup is Yes!poho—India’s first experience-based social platform that connects artisans and customers directly.

The lightbulb moment

The platform’s cofounder Raghuram, fondly known as Raghu, started his entrepreneurial journey early on. He went to the US for his higher education. In parallel, he started working on a commodity trading platform. He wanted to include silk on the trading platform, so he reached out to a friend whose family had business roots in sericulture.

To understand the silk industry and its supply chain, Raghu decided to visit India. He met several silk farmers from different clusters and weavers for the next few weeks. During his stint, he observed the deplorable condition of the handloom weavers. Most of them lived hand to mouth as they earned less than USD 65 (INR 5,000) per month—way below the Minimum Wage Act.

Raghu wanted to buy a few handloom sarees for his friends on his way back to the US. Unfortunately, despite a long commute and detours through several stores, he could not find the sarees of his choice. The unavailability of quality sarees in the cities, coupled with his experience of interacting with the weavers, spurred the lightbulb moment. An idea was born—of a technology-based platform that would connect artisans and customers. It motivated him to take the entrepreneurial plunge yet again.

Figure 2: Meenakshi (L) and Raghu (R) – Cofounders, Yes!poho

Raghu started working on the idea. Later, he roped in Meenakshi Dubey, a tech professional with vast experience in customer relationship management, whom he met during a family event. Meenakshi had a similar discouraging shopping experience while buying sarees for her brother’s wedding. She could relate to the hassle and agreed to join hands.

With their combined expertise, they began talking to artisans and customers to identify gaps related to access and created a tech-based platform to address those issues. Yes!poho was born in 2015, turning their idea into reality.

The unique pitch: A modern spin to the traditional setup

Supply-side transformation

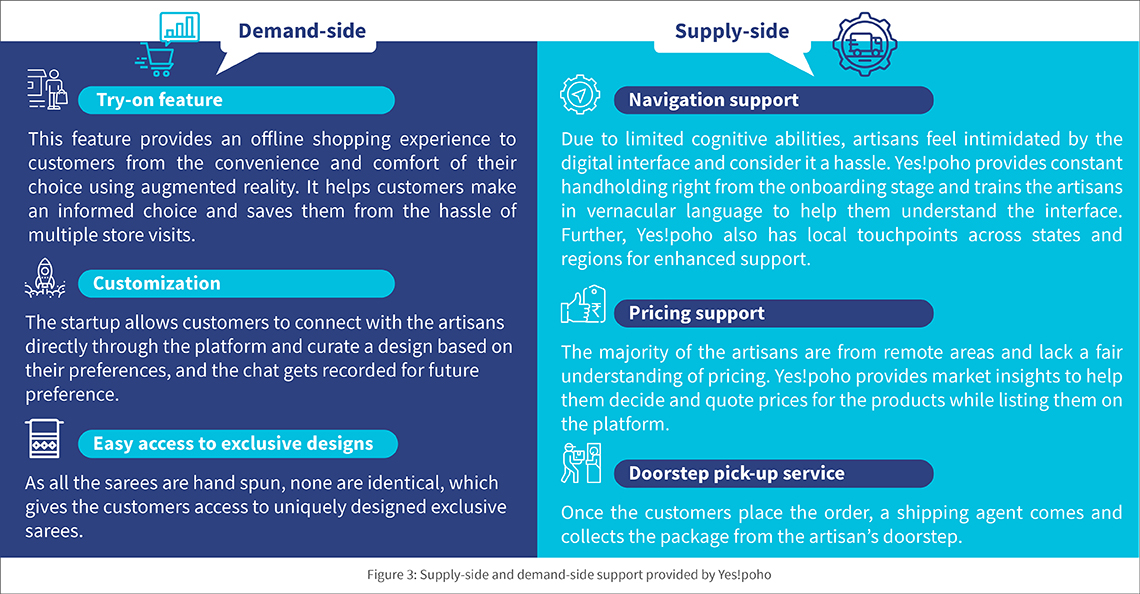

Yes!poho is an experience-based platform that connects the supply-side—the artisans—and the demand-side—the customers—using technology to interact and customize the product. The platform works on an asset-light model. This model puts the onus of inventory management on artisans, who are notified through the weaver-facing interface once customers place an order. Yes!poho has a tie-up with multiple shipping partners across the states in India to collect order consignments from the artisan’s doorstep.

On the demand-front, Yes!poho allows customers to interact with the artisans and customize their sarees based on their preferences. Customers can even buy handloom sarees already listed on the platform.

Are you wondering what is new? The platform offers a unique augmented reality (AR) try-on feature to provide an immersive user experience. The feature helps customers experience the live mockups of the products virtually and make an informed decision, reducing the return rates, which improves profitability for weavers.

Impact on the low- and middle-income group

The roadblocks

Like any other startup, Yes!poho faces its fair share of challenges. Most artisans lack digital readiness and fear online platforms for selling due to loss aversion. They generally exhibit status quo bias and hesitate to work with online platforms. They seek social proof from trusted people, such as friends, and in-person meetings to overcome fear, prolonging the process of lead generation and onboarding.

Further, despite the government’s efforts to revive the handloom sector through recognition and programs, the sector remains highly fragmented and unorganized. The new-generation artisans do not wish to continue weaving and prefer alternate jobs to ensure consistent cash flows.

Support from the Financial Inclusion (FI) Lab

Through CIIE.CO and MSC, the FI Lab have been helping Yes!poho’s business in two phases.

Yes!poho’s passion for improving the lives of the artisan community inspired it to seek a nuanced understanding of artisans’ pain points and expectations associated with the platform. The primary research across six states helped Yes!poho understand the artisans’ needs and gaps in the current artisan-facing interface. MSC also suggested behavioral hooks and game-based setups that Yes!poho can use to expand the artisan base and streamline the lead generation process.

Figure 4: Snippet from MSC’s field study

In the ongoing second phase of technical assistance, MSC been helping Yes!poho design better frameworks through a digital performance marketing approach that will improve customer engagement.

MSC plans to conduct a workshop for the startup by hiring external industry experts and in-house digital marketing specialists to help them understand best practices in digital marketing. The workshop will also provide insights on various topics, such as using data to offer curated advertisement messages for different customer segments, crafting a brand story, and tips to streamline the online purchase experience. This workshop will aid their marketing efforts and support sales uptick.

Overall, the FI Lab’s advisory support will ensure an agile onboarding experience on the supply side to attract artisans to the platform. On the demand side, it will help build a solid customer base to support artisans by buying their products.

The road ahead

Over the next few years, Yes!poho plans to onboard more than 100,000 artisans to their platform and grow their customer base to 1 million from 0.35 million. The team is ready to foray into other parts of the world and sell Indian weaves. It aspires to become a one-stop shop for artisans that goes beyond demand generation for their handwoven sarees. Yes!poho also plans to offer financial products, such as business credit and insurance, to boost artisan’s financial health, motivating many like Dilshad to continue the unique legacy of handloom art.

This blog post is part of a series covering promising FinTechs making a difference in underserved communities. These startups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative, co-powered by MSC. #TechForAll #BuildingForBharat

It is barely 6:30 am when the first mobile money outlets start to open in Soubré, a cocoa-producing town southwest of Côte d’Ivoire. New blue signs with a penguin mascot from Wave, a Fintech created in 2011, and the latest market entrant tower above small kiosks lining the main roads, overtaking the incumbent telecom operator Orange’s black and orange signs.

In the current decade, mobile money and agent networks are positioned as a critical lever and a channel to promote economic, social, and financial inclusion in the last mile. Côte d’Ivoire has a banked population rate of 30.8% and a mobile money penetration rate of 73%. Mobile money, therefore, plays an increasingly important role in financial inclusion in the country.

According to the telecom regulator ARTCI’s quarterly report published in March, 2021, three leading mobile network operators (MNOs) currently control the mobile money offerings in Côte d’Ivoire. Orange CI has been the leader in offering mobile money services in Côte d’Ivoire. The market share of these MNOs—Orange, MTN, and Moov—is 48.3%, 41.1%, and 10.6%, respectively.

Competition in the market was weak until Wave arrived in April, 2021. Two months after Wave launched operations, Orange’s market shares fell by 8.7%, despite a 3.2% increase in mobile subscribers, while MTN lost 1.7% of its market share. The overall total decline of the three operators was 4.6%.

The current competition between new players like Wave and the existing MNOs in the West African market for mobile money services has not only affected market share. Mobile money service providers have started a price war that impacts transaction fees and agent commissions.

Wave, an innovative model but not very user-friendly for the rural population

Wave’s service model is innovative and addresses many of the longstanding pain points of agents. These issues include high transfer fees and double charges for any transaction—the sender pays a charge when sending, and the receiver pays a charge when receiving. Other problems include a restrictive account opening procedure and issues with liquidity.

The registration process for smartphone owners is more straightforward and faster as it is done through an app that provides a QR code. As the penetration of SIM cards is 152% in the country, Wave developed an alternative solution for feature phone owners. A potential client must register in person, where he receives a physical QR code card to bring to each transaction—an additional requirement compared to other MNOs. Notably, Wave customers struggle to check the balance on the Wave account with a feature phone. This is something only agents can do.

Yet Wave’s value proposition is its policy of eliminating dual pricing. To the delight of the Ivorian population, deposits and withdrawals are free for Wave customers. Only domestic transfer fees between operators are priced at 1% of the transaction, while the charge for transfers to neighboring countries is 1.5%—levels below the market average. Likewise, the other operators were compelled to compete with this price and lowered their tariffs to match this new competitor.

Some people are not surprised by these tariff adjustments that have been longstanding in the Ivorian mobile money market. “So these operators have been ripping us off all this time. If today they can lower their rates, they are not honest. They do not like us. Welcome to Wave,” muses Fabiola, an agent at the Soubré market. Wave considers the tariff reductions by competitors as a small victory, as stated by Coura Carine SENE, CEO of Wave Mobile Money: “…Wave is pleased with the alignment of mobile money players to a much-criticized business model.” While this battle benefited clients the most, this is not the case for some agents in the rural areas of Soubré.

Improved support but lower commissions

Some rural agents believe that Wave is the operator that finally understood their liquidity needs by offering a revolving fund and a phone to start operations. The player has created panic in the mobile money market. Decisions made by the competition have influenced the activities of agents in rural areas, such as blocking SIM cards, running investigative visits to ensure that agents do not offer Wave’s services when they are not exclusive agents, and reviewing commission rates.

“They blocked my transaction SIM cards from some agents (including mine) and not others for two weeks, which would require traveling to Abidjan (about 410km) to have access restored,” an agent confirmed. Except for Orange, all operators have modified their agent commissions, which will review their commissions after the cocoa trading period.

Wave’s commission model is based on the volume of daily transactions compared to other operators who apply a per-transaction fee—a model agents prefer. The public’s preference for Wave has caused many transactions to be switched from other operators. The changes in commission levels and the choice for Wave transactions create uncertainty in the total commission package agents earn every month.

Wave’s entry into the market has also shifted other MNOs’ transactions to its platform. According to agents in rural areas, this shift hurts their commissions. With this perception, agents in rural areas face a dilemma between their preferred operator and the commissions offered by that operator. Wave has been taking over most transactions in the market. Yet it offers lower commissions to agents. The incumbent operators, who have dominated the market, offer higher commissions but are gradually losing market share.

From a perspective where the issues are a fair price and customer needs, all stakeholders in the agency banking model benefit from Wave’s entry into the market because they have no choice but to be partners. The impact-based profitability is essential. However, many people question the Wave model’s performance and sustainability.

Without a universal definition of a “successful” agent network, it is still early to comment on Wave’s model.

Our research on successful agent networks and the key elements that determine their success, such as a clearly defined value proposition and a good understanding of the competition, enable digital financial services providers to build an agent network that will help them achieve their goals.

MSC has supported several entities in improving their agent network strategies, operations, and processes. We have researched to understand the agent banking environment and their motivations. We have also trained professionals to manage an agent network and provided training and support to agents to increase transactions and efficiency significantly. This support is based on interviews with more than 40,000 agents worldwide to identify the factors responsible for the success or failure of agent networks, helping our clients to improve their agent network strategies, liquidity management systems, agent selection training, and recruitment approaches. Most importantly, in a highly competitive environment, it has helped the value proposition for agents more attractive and helped reduce inactivity and churn.

MicroSave Consulting (MSC) is a boutique consulting firm that has, for 25 years, pushed the world towards meaningful financial, social, and economic inclusion. These podcast series are hosted by MSC for dedicated founders, start-ups, investors, and other stakeholders in the startup ecosystem. Through this bouquet of curated conversations around developments in the financial inclusion space, we offer insights and lessons based on our research and expertise.

Transforming cash in/cash out – Leveraging the potential of female agents

byMicroSave Consulting

In this podcast, “Transforming cash in/cash out – Leveraging the potential of female agents,” we deep-dive into the landscape for female agents and the challenges they face and discuss opportunities for female CICO agents. We chat with Shelley Spencer, Founder and CEO of Strategic Impact Advisors, a global consulting firm committed to spreading the use of digital technology for financial inclusion and the development of communities and individuals. This podcast is a part of a broader effort of MSC to facilitate discussions on CICO networks through frameworks and collaterals such as blogs, focus notes, and reports.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

medical bills. Customer impact is the guiding force that drives product design and business decisions at the Qonect headquarters. The struggle for money and handling the trauma of a medical emergency may have developed the extraordinary amount of empathy that is evident in Lian when he talks about Qonect helping thousands of users in Northeast India get access to timely and affordable medical services.

medical bills. Customer impact is the guiding force that drives product design and business decisions at the Qonect headquarters. The struggle for money and handling the trauma of a medical emergency may have developed the extraordinary amount of empathy that is evident in Lian when he talks about Qonect helping thousands of users in Northeast India get access to timely and affordable medical services.

To understand the silk industry and its supply chain, Raghu decided to visit India. He met several silk farmers from different clusters and weavers for the next few weeks. During his stint, he observed the deplorable condition of the handloom weavers. Most of them lived hand to mouth as they

To understand the silk industry and its supply chain, Raghu decided to visit India. He met several silk farmers from different clusters and weavers for the next few weeks. During his stint, he observed the deplorable condition of the handloom weavers. Most of them lived hand to mouth as they

It is barely 6:30 am when the first mobile money outlets start to open in Soubré, a cocoa-producing town southwest of Côte d’Ivoire. New blue signs with a penguin mascot from

It is barely 6:30 am when the first mobile money outlets start to open in Soubré, a cocoa-producing town southwest of Côte d’Ivoire. New blue signs with a penguin mascot from  Wave’s service model is innovative and addresses many of the longstanding pain points of agents. These issues include high transfer fees and double charges for any transaction—the sender pays a charge when sending, and the receiver pays a charge when receiving. Other problems include a restrictive account opening procedure and issues with liquidity.

Wave’s service model is innovative and addresses many of the longstanding pain points of agents. These issues include high transfer fees and double charges for any transaction—the sender pays a charge when sending, and the receiver pays a charge when receiving. Other problems include a restrictive account opening procedure and issues with liquidity. Wave’s commission model is based on the volume of daily transactions compared to other operators who apply a per-transaction fee—a model agents prefer. The public’s preference for Wave has caused many transactions to be switched from other operators. The changes in commission levels and the choice for Wave transactions create uncertainty in the total commission package agents earn every month.

Wave’s commission model is based on the volume of daily transactions compared to other operators who apply a per-transaction fee—a model agents prefer. The public’s preference for Wave has caused many transactions to be switched from other operators. The changes in commission levels and the choice for Wave transactions create uncertainty in the total commission package agents earn every month.