One of the flagship schemes of the current government in India is Pradhan Mantri Jan Dhan Yojana (PMJDY). It was launched as a national mission on financial inclusion in 2014 with an aim to provide access to affordable financial services to all. It played a critical role in managing COVID 19 crisis in India and supporting the weaker sections of the society. The government was able to provide cash support 198.6 million which amounted to INR 99.3 billion (as on 13th April, 2020). To date, more than 381 million accounts have been opened under PMJDY scheme with around 470 million insurance beneficiaries and 19 million pension beneficiaries.

Blog

An insight into the case fatality rate and its association with preventive measures taken by government in response to Covid-19

These projections have validated the necessity of these preventive measures. Similarly, the available data around fatalities, infections and tests conducted provide useful insights into the efficacy of preventive measures and the fallacies around stand-alone, exhaustive testing strategies.

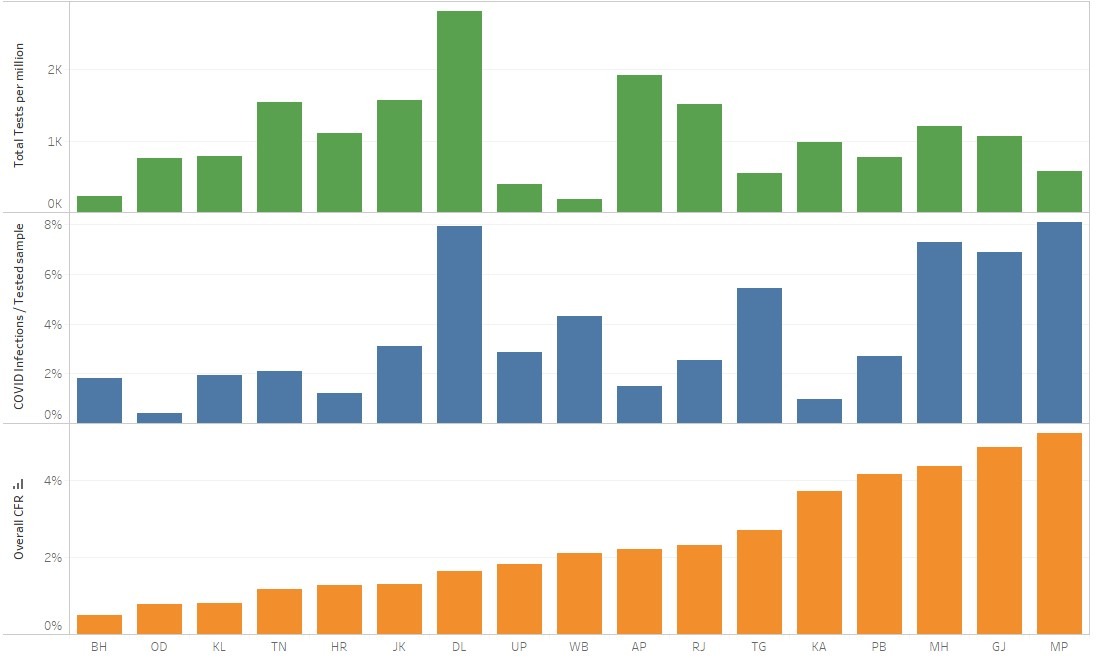

Based on the data released by the Ministry of Health and Family Welfare, GoI, we looked into the Case Fatality Rate (CFR) across 17 Indian states with more than 100 active cases. The aim was to explore the relationship between CFR and the preventive measures taken by respective state governments as a response to Covid-19. Apart from individual epidemiological factors, there could be various cofactors for CFR like the medical infrastructure and facilities, availability of frontline health workers, government preparedness & response and testing rates which helps in diagnosing the cases early and take essential measures. Using the 2011 census data, we calculated the number of tests done per million population in a state. This we call as tests per million. The other data-point that we used is the percentage of positive cases emerging from the tested sample. This we call as infection rate.

COVID19- Cases, infection and tests rate graph

Fig1: Case fatality rate, Infection rate – COVID infections/tested samples, Total tests per million population

Among the states, Madhya Pradesh (5.22), Gujarat (4.87) and Maharashtra (4.36) have the highest CFRs while Bihar (0.49), Odisha (0.78) and Kerala (0.80) are at the opposite end of spectrum.

In Madhya Pradesh, more than 60% of the cases and approximately 67% of the state’s deaths can be traced to the Indore-Ujjain corridor. This rules out individual epidemiological factors and suggests that better quarantine, testing and enforcement of lockdown protocols could have led to early detection and prevention of fatalities. Madhya Pradesh also has the highest infection rate at 8.09% and a testing strategy (575 tests per million) that is well below the 17 state average (825). A high CFR, high infection rates and low tests per million indicate that a lot more needs to be done to flatten the curve.

Odisha, on the other hand, has the second lowest CFR at 0.78, after Bihar (0.49). It also has the lowest infection rate at 0.40% compared to the 17 state average (3.76%). After the first COVID positive case was found in Odisha, the state was able to ramp up its social distancing and quarantining policies along with ramping up of testing protocols. The public health measures taken by the state has led to flattening the disease progression curve.

Maharashtra and Delhi show how exhaustive testing strategies will not work without effective complementary preventive measures. Maharashtra, at 1210 tests per million, is well above the India average (825) and has conducted the highest number of RT-PCR tests (130,000+) in absolute terms. In spite of this, the state has a high infection rate (7.31%) and CFR (4.36). Similarly, Delhi (2800 tests per million) having conducted more than 3 times the national testing average, has the second highest infection rate (7.93%). Both the states need to take more measures to flatten the curve. Anecdotal data and news reports suggest the need for strengthened and coordinated enforcement of preventive measures in these states.

As we prepare a graded exit strategy from the lockdown, it becomes evident that the preventive measures implemented in India have been largely effective in controlling the pandemic. Any exit plan must incorporate these learnings to tide over the epidemic in our country.

The blog was also published on ET Healthworld.com on 6th of May, 2020

GUVI: Bridging the language divide in learning technical skills

This blog is about a startup under the Financial Inclusion Lab accelerator program, which is supported by some of the largest philanthropic organizations across the world – Bill & Melinda Gates Foundation, J.P. Morgan, Michael & Susan Dell Foundation, MetLife Foundation and Omidyar Network.

The light bulb moment

Approximately 80% of computers, electronics, or allied engineering graduates are not fit to hire. Hence, it comes as no surprise that 73% of the recruiters are not able to secure the talent they require.

GUVI is an integrated EduTech platform that provides technical skills in local languages with end-to-end personalized support throughout the process of learning to recruitment. Arun Prakash, S.P. Balamurugan, and Sridevi founded the platform. While working together at PayPal, they observed a huge gap in the technological skills of fresh graduates in India, especially in computer programming. According to recent reports,

What started in 2014 as a YouTube channel to share technical knowledge has rapidly evolved into one of the biggest online EduTech platforms in South India.

“I remember posting a short YouTube video on the basics of programming in C/C++ in the local language—a mix of Tamil and English. That video became quite popular quickly!” Arun, the co-founder of GUVI, noted in one of the boot camp events of the Financial Inclusion (FI) lab.

“That was a light bulb moment for us. We suddenly realized the huge opportunity to bridge this skilling gap through the creation of an integrated learning and recruitment platform to cater to the talented but unskilled technical graduates from tier II and III cities,” he continued.

Figure 1: The co-founders of GUVI- Arun Prakash, SP Balamurgan, and Sridevi (L-R)

The unique pitch

GUVI’s mission is to make skilling an easy, simple, and intuitive process by bridging the gap between skilling and recruitment. On this platform, students can learn in their local languages through bite-sized videos, practice coding, test their skills, and compare their progress against their peers. GUVI attempts to make learning fun for its students through a gamified platform to practice coding, which awards “merit badges” to students who complete a course successfully. It also conducts periodic assessments and coding contests and rewards the top performers. The entire learning history of a student is maintained as part of their GUVI profile, which they can share with potential and current employers.

GUVI works on two models—an online learning platform that has been described briefly in the “unique pitch” section and an offline model that includes zen classes, which is a special classroom coaching model. As part of zen classes, GUVI handpicks students, trains them through industry experts, and finally places them with potential recruiters. Thus far, GUVI has been able to secure placements for all of its four zen class batches.

Skilling learners in the times of Covid-19

That Guvi’s model is relevant and popular with learners can be gauged by the fact that as on date (26th April, 2020), 62,000 new learners have joined the platform to upskill themselves since India went into a country-wide lockdown on 21st March, 2020. This led to a significant jump from 250,000 to 312,000 learners that are now registered on Guvi’s platform since the pre-lockdown period. Now on an average, a learner spends 20 times more learning hours per week compared to the time they spent during the pre-March 2020 period. Testament to its success is the fact that GUVI raised in April 2020 INR 6 crore in a pre-series A round of funding from Education Catalyst Fund.

Impact on the LMI segment

In India, students from tier II and III cities face the following challenges:

- They are not exposed to quality technical education in schools and colleges because quality instructors in this domain are usually found in tier I cities where they are paid better

- They struggle to read, understand, and write in English, which is the common medium of teaching technical courses and coding languages.

Unable to overcome these challenges, such students find it difficult to acquire the requisite skills to attain appropriate jobs.

GUVI, through its low-priced, local language platform and on-demand, simplified computer programming courses, has up-skilled more than 150,000 students, mostly from the LMI segment, and helped them be recruited in respectable technology firms.

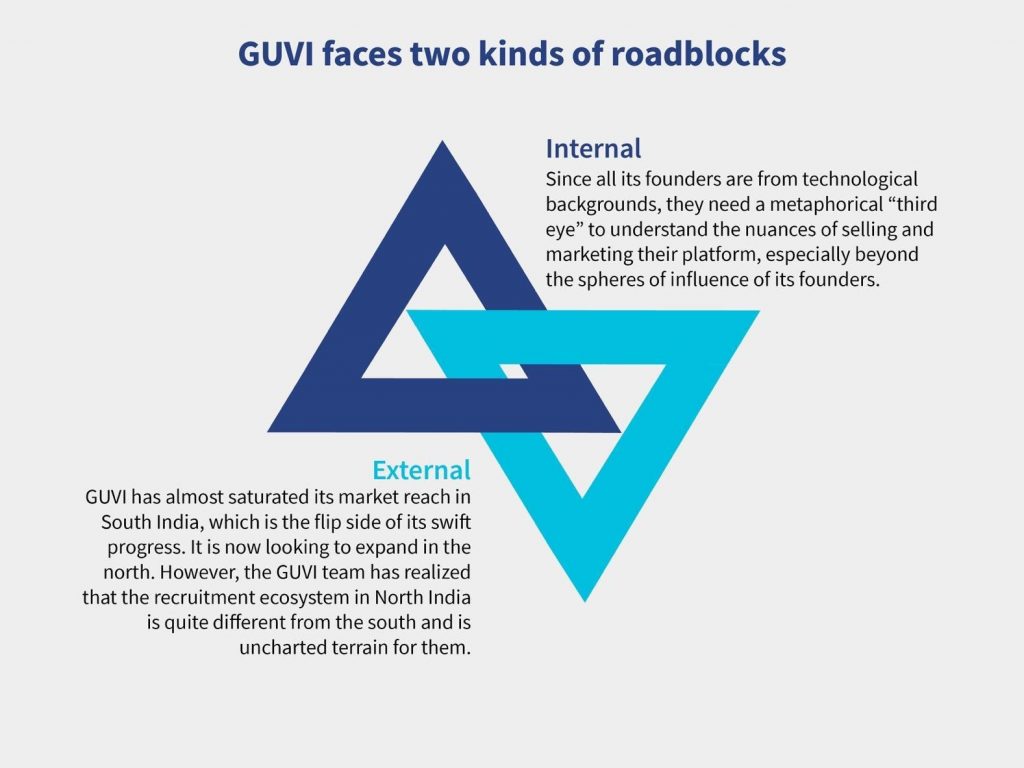

The roadblocks

Support provided by the Financial Inclusion lab

GUVI was selected for the Financial Inclusion Lab in its second cohort in March 2019, as part of which the start-up went through boot camps, diagnostic sessions, and clinic sessions with that provided bespoke technical assistance to achieve the following objectives:

- Understand the nuances of the fresher recruitment ecosystem of North India. This also included opportunities and market sizing of the business opportunities of GUVI with small, medium, and large technology enterprises and training and placement consultancies;

- Develop a cost-effective go-to-market (GTM) strategy by identifying the product-market fit for GUVI from among the technology and placement companies explored earlier; and

- Identify any overlooked skills to help GUVI differentiate itself from its competitors.

While the support of the Financial inclusion Lab continues, GUVI has already been able to achieve the following milestones:

- Partnerships with its most relevant enterprise segment—small and medium-sized technology firms in the north;

- Involved in strategic partnership discussions with prestigious IT industry associations such as NASSCOM, which has a pan-India presence and influence; and

- Built and incorporated soft-skill training modules in its platform to augment the employability of its trainees.

As a result, GUVI witnessed an improvement in the number of recruiters who joined its platform alongside an increase in the success rate of placement of its students or trainees, both in North and South India.

Skilling learners in the times of Covid-19

GUVI has become more relevant and popular for learners. Now, a learner spends, on an average, 20 times more hours per week as compared to time spent during the pre-March 2020 period.

Witnessing the immense success in terms of the number of learners on the platform, GUVI has also re-invented it’s B2B2C business model, in which it offers its courses and platform to engineering colleges completely online, due to broader market situation. GUVI has also proactively moved its Zen classes, one of the most popular and successful ones, completely online because of the lockdown and social distancing norms.

GUVI firmly believes that they can overcome the barriers of the background, region, situation, or financial status to skill any willing learner.

This blog post is part of a series that covers promising FinTechs that are making a difference to underserved communities. These start-ups receive support from the Financial Inclusion Lab accelerator program. The Lab is a part of CIIE.CO’s Bharat Inclusion Initiative and is co-powered by MSC. #TechForAll, #BuildingForBharat

Is it the right time to push for wallet interoperability in Bangladesh?

Covid-19 is impacting people’s lives in multiple ways. With restrictions on movements and fear of getting infected, people are staying homes. While this is the right thing to do, one still need to purchase household essentials and send money to relatives who need it. Essential services industries also need constant cash flows and payments. Jamal offers one such service. He is a fish seller. He travels 30 kms everyday from his village in Narayanganj to sell fish in Dhaka. He receives bulk payments from customers – once in 15-20 days, both in cash or in his bKash wallet. But that’s the story of pre Covid-19 time.

Policymakers have proactively taken steps to ensure financial service needs to people are not hampered

MFS providers, such as bKash, Rocket, and Nagad have emerged as key channels for fast and cost-effective fund transfers with minimal manual interventions. Bangladesh Bank asked the competent authorities from the Home and Finance Ministries and Bangladesh Police to take essential action for asserting mobile financial services (MFS) as emergency services amidst the ongoing closure following the coronavirus outbreak. The Bangladesh Bank has also made MFS cheaper through its directive which says that no transaction charge would be levied to purchase medicines and other essential commodities using MFS P2P transfer and debit or credit cards. The merchant discount rate and interchange reimbursement fee will not apply to a transaction limit of BDT 15,000 per day and BDT 100,000 per month. Further there will be no charge for MFS cash-out of BDT 1,000 daily at a time. The current charges are BDT 20 for BDT 1,000 withdrawal. The monthly ceiling of MFS P2P transactions has been raised from BDT 75,000 to BDT 200,000. The transactional premises of banks, ATM booths, POS, and agent points are required to be disinfected periodically and equipped with hand sanitizer.

In addition, readymade garment factories have been directed [by whom??] to pay all salaries to workers and employees through MFS accounts. This must be done by 20th April, 2020. It is important to note that the government and stakeholders had committed to making wage payments to around 90% of the country’s garment workers digitally by 2021 as part of the government’s target to develop a cash-lite digital ecosystem in line with the vision of “Digital Bangladesh”. Infrastructure development, creating awareness among owners and workers, and financial and digital literacy are the major challenges in bringing all the garment workers under the digital wage payment system. Currently, more than 1.5 million out of 4.0 million garment workers have been receiving their wages digitally. With Government’s current push some of these challenges will be addressed. The circular suggests banks and MFS providers create immediate awareness of the scheme amongst target customers and direct/help them to open MFS accounts. Customers can open these accounts free of cost. We learn that bKash is now registering more than 50,000 new wallets of RMG workers every day. Almost 70% of these wallets are registered at its digital registration agent points.

Although transactions are reducing but it does not indicate that people do not need money

bKash has been managing, on average, 5.7 million transactions of BDT 4,500 million (USD 53 million) since the government’s general leave from 27th of March 2020. At the same time, 150,000 consumers across the country have paid for electricity bills through bKash in a single day. But compare this with pre-covid-19 situation: bKash handled approximately BDT 10,000 million (USD 119 million) in terms of transaction value.

Almost all MFS agents remain closed under the lockdown situation; the remaining agents open their shops for limited hours in a day. The regular earning of the low-income group people, such as rickshaw pullers and daily laborers has been reduced significantly and in many cases eliminated. They have been living on limited means with aid from the government along with other social organizations and NGOs. Such lower-income people use cash-in/cash-out/P2P almost every day—such transactions have reduced. An ongoing MSC study has found that the incomes of some MFS agents have reduced by 50%-70%.

Activity at ATMs has reduced as well. For Dutch-Bangla Bank country’s leader in ATM banking, daily transactions at ATMs have reduced by 30-35%. Bank Asia’s agent banking outlets are conducting almost 20% of the transactions they performed in pre-covid-19 times. Most of the agent banking outlets remain closed during this pandemic lockdown situation.

These extraordinary reductions in transactions can be attributed to restricted movement of people, slump in economic activities, and the closure of service points.

Jamal is impacted as well. While he is not selling fish currently, but he has payments due from his customers that could help him wade through these difficult times. Sadly, though, some of his customers only have Rocket wallet and cannot send money to him.

Money is indeed not moving smoothly between rural and urban areas, because banks and agent banking outlets have limited operations. Those MSMEs that were operating through banks are facing challenges in making and receiving money, as banks are not working in full capacity.

Can interoperability of wallets help?

Developing an interoperable switch is not an easy technology. It is a complex process that ensures that the customer user experience is seamless and pricing is just. The backend system of a switch, settlement process for providers, pricing amongst the parties, etc. has to be carefully thought of as well. The regulator needs to establish a governance framework that is transparent and inclusive, and a strong Anti-Money Laundering (AML) compliance for interoperability.

We wonder if in these times where everyone is working hard to make basic things work, Bangladesh Bank has the bandwidth to put interoperability into practice. The easiest bit can be tried first. In our opinion that will be MFS wallet to MFS wallet interoperability. That is a customer having a Rocket wallet will be able to send money to a bKash wallet. But this type of interoperability may have unintended impacts on how agents operate. MFS provider and regulations can be tightened to ensure thriving competition in the market. MFS wallet to MFS wallet interoperability will impact 80 million registered wallets across 64 districts in Bangladesh—and positively, we believe.

The most profound impact will be on people’s financial lives. An interoperable wallet facility will reduce at least one worry of ensuring that both parties have same wallet service providers. This will impact all MFS users including the newly on-boarded RMG workers. It will bring ease receiving and making payments for goods and services especially for MSMEs, who are likely to adopt payments via MFS wallets as the Bangladesh Bank has already increased the limit for P2P to BDT 200,000.

The authors are international financial inclusion consultants from MSC – a boutique consulting company working on meaningful financial, social, and economic inclusion. They can be contacted at Jakirul@microsave.net and Akhand@microsave.net

The blog was also published on Financial Express on 27th of April, 2020

Aadhaar Ideas and lessons from India

Aadhaar is a unique digital identity issued by Unique Identification Authority of India (UIDAI). It is a database with no duplicates which serves as an identity and address proof. More than 1.25 billion residents have enrolled themselves in it. It has been a game-changer in streamlining digital payments in India, including G2P payments. In the midst of COVID 19 crisis, the Indian government has been able to support the vulnerable sections of society via cash transfer support. The government transferred USD 7 billion benefiting more than 200 million households in the country.

Innovations and coping strategies for food security at the time of COVID-19

COVID-19 is likely to have a widespread, deep, and prolonged impact on every sector and segment. Farmers and cultivators in countries like India are rapidly starting to bear the brunt of the pandemic, even though restrictions and lockdowns have largely spared agriculture and allied sectors. The disruptions have affected the long value chains between cultivators and consumers. Retail prices have shot-up, wholesale prices continue to fall, while producers struggle to find buyers for their produce. In many areas, farmers lack access to adequate labor or equipment to harvest standing crops.

The impact on the next cycles of cropping is going to worsen as several factors start to play out. These include constrained logistics of input supplies to farmers, an anticipated shortfall in the availability of credit, subdued demand, unpredictable consumer behavior, and reduced buying power. Sadly, the worse may be yet to unfold!

What can players in the ecosystem do amid the gloom? Are there innovative and practical solutions to aid food security? Can we prevent massive wastage or losses and protect the livelihoods of smallholders?

Lessons from innovative ideas and approaches, and their rapid replication

India is known for its frugal and rapid innovations, termed colloquially as jugaad. Agtechs and other stakeholders in agri value chains are trying innovative approaches to reduce the fallout of COVID-19.

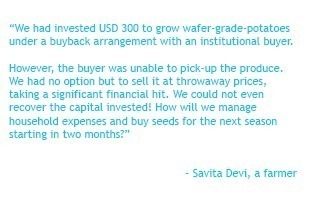

Savita Devi, an Indian Farmer

Lessons must be learned quickly, evaluated, and those that work should be scaled up. Governments, private players, investors, and start-ups will need to recognize solutions with high potential and invest in them to expand them rapidly. These are trying times like never before. Yet they also offer opportunities for unprecedented innovation, learning, and evolution of collaboration models.

Let us start at the consumer end. Household demand for staples and perishables is still high. We can say that this demand is reasonably inelastic, especially in urban areas and in the near-term. Closure of restaurants and workplaces has expanded demand somewhat, at the household level. Moreover new demand centers like community and government-sponsored kitchens have surfaced.

Entrepreneurs have developed simple demand aggregation solutions using Google Forms or over WhatsApp messaging. Once logistically feasible demand is generated, for example, a suitable truckload, entrepreneurs are completing fulfillment directly from farm gates. Agri-techs can do this either directly or in collaboration with active farmer cooperatives or producer organizations. Noteworthy examples include Praakritik, Sahyadri Farms, and Loop from Digital Green.

Based on anecdotal evidence, farmers who have been able to connect through these entrepreneurs are harvesting under-ripe fruits and vegetables. Earlier, market intermediaries would undertake the ripening process down the value chain. However, the current trend—and fear of coronavirus—makes consumers store fruits and vegetables for a couple of days before consuming them. This means that ripening is now happening on the shelves of consumers. This is beneficial for farmers as it reduces wastages. Moreover, the farmer has factored the increased time required to get the produce to the consumers with the prevailing lockdown in place.

Governments, such as in Maharashtra, are trying to devise innovative solutions. They have tied-up with leading farmer producer organizations to supply produce directly to households. However, logistics and fulfilment needs considerable strengthening. Getting to scale with such models is the challenge. Agri-techs that have robust farm-to-fork supply chains can provide important lessons.

Governments should collaborate with agri-techs that have the outreach and are capable of scaling up, rather than trying to create impromptu farm-to-fork supply chains.

Governments should collaborate with agri-techs that have the outreach and are capable of scaling up, rather than trying to create impromptu farm-to-fork supply chains.

As we move up the value chains, wholesalers and aggregators are facing a slowdown in demand from retailers and vendors. This is because of a combination of issues related to logistics and the partial closure of retail markets. Overall, wholesale prices are being driven down while the agriculture value chain from farm to fork faces many roadblocks. The friction in the supply chain has multiplied because of the lockdown. Reduced wholesale prices and increasing retail prices reflect the situation—not a happy one for either the farmer or the consumer.

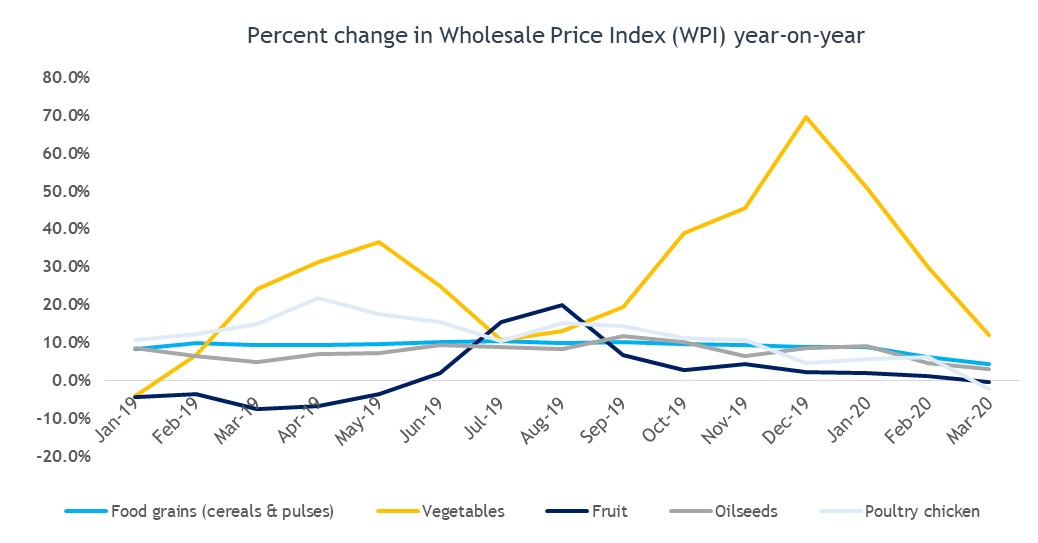

The year-on-year trend in the Wholesale Price Index (WPI) for food grains, oilseeds, vegetables, fruit, and poultry exhibits a sharp downward trend. The disruption in retail supply chains of food grains and perishables is causing uncertainty in supplies and fluctuating prices. Meanwhile, panic buying and hoarding by high-income segments have started to create shortages for low-income segments.

Department of Co-operation, Marketing and Textiles, Maharashtra

Percentage in Wholeprice Index

Source: Government of India, MSC analysis

Governments and local bodies need to streamline operations of agri-markets even as they ensure safety. Some states have staggered the working hours in markets, with separate timings for buying fruit and vegetables and longer opening hours throughout the day. Wholesale agri markets are functioning from midnight to early morning in some districts in Uttar Pradesh. This discourages retail buyers from flocking to these markets in search of bargains. Other states are identifying new marketplaces to expand space for agri-transactions while reducing mass gatherings.

The critical role of self-help-groups

Low-income segments receive a significant part of their food supplies through the Public Distribution System (PDS) in India. Women self-help groups (SHGs) can play a vital role in strengthening the distribution of food grains. In the state of Bihar, SHG members undertake distribution of a select basket of food grains for the low-income households. This is managed through a World Bank-supported Food Security Fund (FSF) program.

In the state of Uttarakhand, SHGs and village organizations are actively involved in cleaning, sorting, packaging, and distribution of a basket of food grains. The state government has gone a step further to broaden the food basket to include local millets, which add nutritive value while catalyzing demand from local smallholders—thereby adding to their revenue streams.

SHGs and women cooperatives have proven their agility in this time of crisis. They are actively involved in producing new categories of products that are in demand. These include fabric masks, aprons, sanitizers, and soaps. The state rural livelihood missions (SRLMs) drive most of the SHG programs. State governments need to share lessons across different SRLMs and replicate innovations and best practices to achieve better outcomes.

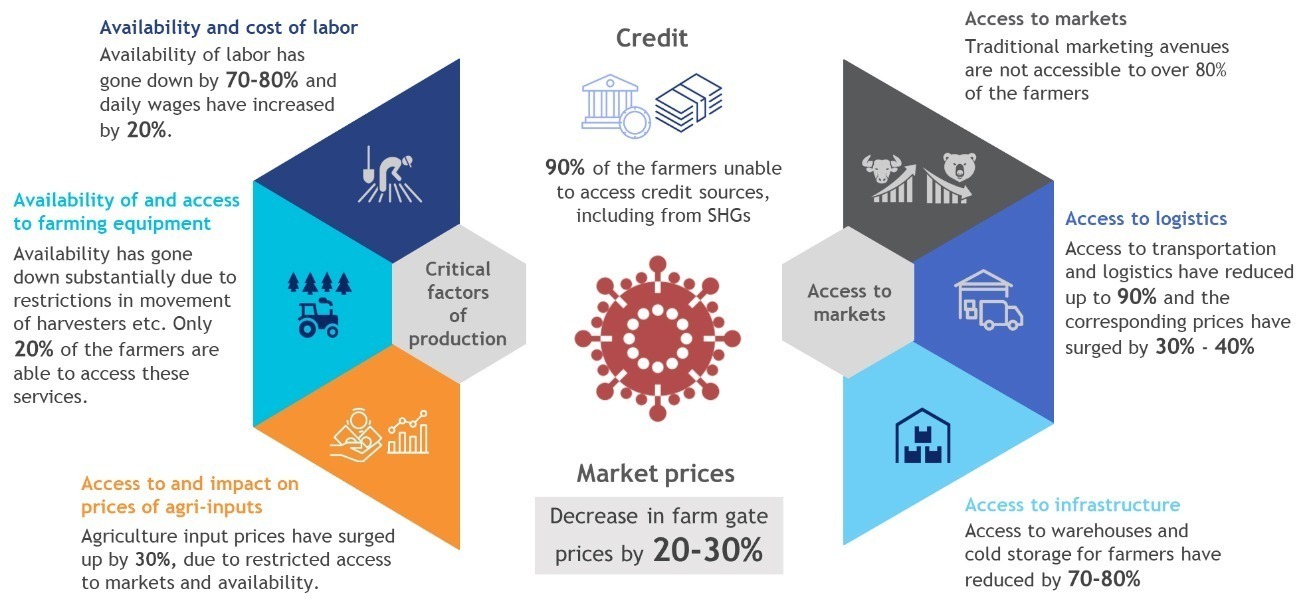

We now analyze how farmers, who are at the top of agri value-chains, are coping. MSC conducted a short research exercise with a few farmers, rural aggregators, and traders. The following exhibit summarizes the situation of the farmers and the distress they face.

Indian Market price and production illustrator

Farmers are suffering substantial economic losses due to disruptions in market access, logistics, and prevailing uncertainty.

They are uncertain and scared of threats and challenges related to their harvest-ready Rabi (winter) crops.

Harvested crops are either being sold at extremely low prices or are being stored in non-conducive conditions. Reports have emerged of farmers burning their standing crops, as the economics of harvesting them and transporting them to markets are not feasible.

Harvested crops are either being sold at extremely low prices or are being stored in non-conducive conditions. Reports have emerged of farmers burning their standing crops, as the economics of harvesting them and transporting them to markets are not feasible.

Burnt crops

Farmers are even more apprehensive of the upcoming Kharif (summer) cropping season. They are uncertain about the crops to plant. The situation of the market and the logistics at the time of harvest are unpredictable. The farmers are also concerned about the unavailability of farm inputs and credit.

Livestock farmers are equally distressed. For example, poultry prices have dropped more than 90% during the past two months. This is partly due to the unfounded belief that coronavirus can be transmitted through poultry.

Potential solutions for farmers

At this point, governments must undertake widespread communication with farmers and MSMEs in agri and allied sector value chains to allay fears, address misperceptions, and outline measures and interventions being taken.

MSC is planning to undertake a research project with farmers, traders, and other intermediaries. This will generate last-mile insights for policymakers and the sector at large, based on ground validated realities. Governments and policymakers should make informed decisions, determine appropriate responses, and calibrate actions to support smallholders and their families.

Under the leadership of JEEViKA and with support from the Bill & Melinda Gates Foundation, farmer producer companies (FPCs), MSC, DeHaat (Agrevolution), and other partners have been working together to support smallholder farmers in Bihar. One of the interventions is to provide timely offtake and optimal value realization for the harvest-ready maize crops of farmers. DeHaat has an innovative model of continual physical and digital (phygital) engagement with farmers throughout the year by meeting their needs for inputs, advisory, marketing, and credit linkages.

Under the leadership of JEEViKA and with support from the Bill & Melinda Gates Foundation, farmer producer companies (FPCs), MSC, DeHaat (Agrevolution), and other partners have been working together to support smallholder farmers in Bihar. One of the interventions is to provide timely offtake and optimal value realization for the harvest-ready maize crops of farmers. DeHaat has an innovative model of continual physical and digital (phygital) engagement with farmers throughout the year by meeting their needs for inputs, advisory, marketing, and credit linkages.

MSC is also exploring partnerships with innovators like GrainPro to provide low-cost hermetic storage facilities to farmers and FPCs. Farmers are unable to transport produce to warehouses or to markets. Temporary storage solutions at their farms or homes, therefore, can provide immense value. These will allow farmers to store grains for the short-term without infestation, degradation in quality or moisture levels, and thereby allow them to retain value.

A bag of grains

India has several innovative models similar to those of DeHaat and GrainPro. They include Kamatan, Crofarm, Ninjacart, WayCool, and many others. These institutions work across India on diverse agricultural or horticultural commodities while others like S4S Technologies, OurFood, and Ecozen provide smart and low-cost primary agri processing and storage solutions.

The country now also has a range of custom hiring centers (CHCs), some with Uber-like models. They can meet the shared needs of farm equipment economically and efficiently, particularly when availability is severely constrained.

The current situation provides an opportunity for governments and other stakeholders to collaborate and scale-up outreach that many of these MSME models find it difficult to achieve on their own. Farmer producer organizations and companies too can be important partner institutions in this multi-stakeholder approach, as the country prepares to ensure food security for all and to protect the livelihoods of farmers.