UNCDF’s Landscape Assessment of Retail Micro-Merchants in Bangladesh has shown that retail micro-merchants require access to financial services and credit in particular. Their need for financial services is high, and microfinance institutions are well placed to meet the growing credit needs of micro-merchants. These micro-merchants borrow predominately from microfinance institutions. With the introduction of digital technologies, microfinance institutions have a new opportunity to expand financial services further to micro-merchants by embracing digital and mobile technologies in their operations. In this context, UNCDF SHIFT commissioned MSC to conduct a study on the status of digitization in the microfinance sector in Bangladesh.

In the course of the research, we identified that while most MFIs use a loan management system, only a handful of MFIs have taken steps to digitize transactions. There are very few of these initiatives at pilot stages. Only three of the 16 surveyed MFIs have rolled out pilot tests to use the digital field application for loan origination. In conclusion, MFIs are on a digital journey but are yet to explore many more emerging technologies that would bring process efficiency and also increase the uptake of the products offered.

Keeping the micro-merchant market segment in mind, this report answers the questions of how and why microfinance institutions should make a switch to digital technologies to meet their customers’ needs better.

MicroSave (MSC) undertook extensive and widespread stakeholder consultations and has developed this report for enabling a micro-insurance ecosystem in Mozambique. It provides a pathway for a stronger foundation of micro-insurance in Mozambique and to guide all stakeholders towards establishing a mature and sustainable micro-insurance sector in the country. In this report, we discuss in great length about the four fundamental pillars necessary to develop an enabling ecosystem for micro-insurance in Mozambique.

I am Bernie Akporiaye, the co-founder & CEO of MaTontine. My speciality is financial software. My personal mission is to help reduce poverty in Africa through entrepreneurship and technology. I have has worked for over 20 years in Africa and elsewhere around the world.

Can you please introduce MaTontine?

MaTontine provides access to small loans and a range of financial services like microinsurance to the financially excluded in Francophone Africa via basic mobile phones. The problem for our customers is that they do not have access to small loans at reasonable costs. We solve the problem by utilizing mobile phones and our platform to digitize the benefits of traditional savings circles (ROSCAs), thereby reducing the cost of borrowing by 75% or more.

Why MaTontine? What client needs does it answer?

The big problem we are trying to solve though is how to lend small amounts like USD 100 profitably and at scale to the 1 billion people in Africa who are financially excluded. The banks and microfinance institutions cannot do it with their current cost structure. Consequently, the end user does not have access to financial services that are easily available, accessible, and affordable. The solution is a combination of technology, partnerships, and leveraging existing, traditional systems.

How long did it take you to commercialize MaTontine

Two years

What challenges did you have to face?

Our biggest challenge has been regulatory. We have found the regulators to be very inflexible. It seems to me that the financial services rules used to regulate today’s FinTech companies were designed decades ago for legacy financial institutions. We also found it difficult to form partnerships. The reality of the situation is that in Africa, one is dependent on the infrastructure of large companies like operators and insurers to deliver one’s services. These companies have very little motivation to work with small start-ups, so getting access to the decision-makers in these large companies to form partnerships is difficult.

What are the keys to success for a start-up like yours?

The keys to success for MaTontine and similar start-ups are a friendly regulatory environment, easier access to strategic partners, a simple and intuitive customer experience, and the ability to attract and retain senior management.

What are the key figures for MaTontine so far?

• We want to provide financial services to 1 million women over the next five years

• 90% of our members are women

• Till date, the default rate on loans provided has been 0%

• USD 100,000 lent to 1,000 in the past quarter

• The average contribution (savings) is USD 30 per month

• The average loan size is USD 170

• The current services are loans, life insurance, and health insurance

• 5,000 members by December, 2018

• USD 500,000 in loans by December, 2018

• USD 1 million in savings on the platform by December, 2018

In two recent blogs on the MSC website, I examined the evolution of the financial inclusion industry in the 20 years since MicroSave was established in 1998. In this blog, I will play the fool’s game of looking forward to what might happen in the next 20 years.

The future will inevitably prove me wrong on many points, but these predictions should, at a minimum, highlight some trends and technologies that are likely to play important roles in the sector’s ongoing development.

The Potential of Technology

We live in extraordinary times: In the next 20 years, those of us privileged to live in wealthy countries can expect to see drone deliveries, driverless cars and Hyperloop trains in use in our communities. Virtual reality will replace textbooks, fully furnished, 3D printed houses will come into being and the Internet of Things will be ubiquitous, while robotics will replace millions more jobs. We can also expect to see Big Data analytics integrated into everything we do — used both by those who want to sell to us and the governments that “take care” of us. As a result, the combination of smartphones, computers, CCTV cameras, sensors, wireless communication satellites and GPS will eradicate most forms of privacy.

And these are just the easily predictable innovations: Some analysts point to a future marked by technologies that are far harder to foresee. For instance, Ray Kurzweil, a Director of Engineering at Google makes remarkable predictions based on his Law of Accelerating Returns, which states that technology is progressing at an exponential rate — much faster than our traditional linear way of thinking. This acceleration will provide unimaginable advances in just a few decades, from DNA manipulation and nano-bots that can ensure immortality, to “the singularity,” in which computers merge with man, unlocking astonishing new capabilities. Ultimately, Kurzweil predicts, this massive degree of technological development will largely eradicate wars, disease and hunger by 2050.

No less an authority than Bill Gates extends some of this optimism to financial inclusion. In his 2015 Annual Letter, he wrote, “By 2030, 2 billion people who do not have a bank account today will be storing money and making payment with their phones, and by then, mobile money providers will be offering the full range of financial services, from interest-bearing savings accounts to credit to insurance.” I won’t hazard a guess on the likelihood of the singularity – much less predict a date. But I find Gates’ predictions on financial access to be quite realistic. The question is: Will the distribution of these innovations be equitable? That’s less clear.

History teaches us that humanity is remarkably poor at sharing wealth and well-being. Will it be different in the next 20 years? Much will depend on how effectively we choose to address the six core drivers of the digital divide—and this will largely be determined by the seventh core driver: the business case to do so. Let’s examine some of the technological and social/psychological barriers to this potential progress – and how these challenges can be overcome.

Technological Barriers and Solutions

The prospects for the equitable division of tech-generated revenue in emerging countries do not look positive. The Brookings Institution report of 2016 on income inequality concluded, “The basic story that emerges from a review of the evidence on income distribution is one of steady and often major increases in inequality within countries over the past about three decades.” If the poorer countries and populations within those countries do not reap the benefits of the increasing prosperity arising from the new digital age, private sector entrepreneurs are unlikely to invest in providing products and services to them.

At present, the low-income market does not buy enough to warrant the data-driven, targeted digital marketing that sustains Facebook, Google, and so many other platforms and apps. And even where the poor can access the internet, they do so with what Jonathan Donner calls the “metered mindset, in which people don’t surf and browse, but rather sip and dip.” This lack of a strong business case is a major impediment to access: As the Collaboration on International ICT Policy in East and Southern Africa notes, “Internet penetration in Africa stands at 21.8% of the population, leaving the majority of the continent’s population offline.” If these conditions persist, we risk seeing digitally enabled hotspots only in urban and peri-urban areas where it is profitable to deliver digital services — and digital deserts in rural and remote areas. As others reap the benefits of enhanced education, healthcare, agriculture, enterprise and financial services, those stranded in the digital deserts would be left to struggle with basic analog and 2G products. This would inevitably lead to increased rural to urban migration, the outcomes of which are much debated.

Addressing this digital divide will require concerted efforts from governments, development agencies and the private sector, which must work together to provide an enabling environment and digital ecosystems for the development of new products. This is where initiatives to build infrastructure, like the Gates Foundation’s Mojaloop, can play a necessary (but probably not sufficient) role. E-platforms such as Google/Alphabet, Apple, Facebook and Amazon, and Chinese companies such as Baidu, Alibaba Group, Tencent Holdings and JD Group could also play a central role. However, they would rather ride on functioning ecosystems than roll out their own.

To help create these ecosystems, Universal Service Funds (USFs) have been collected in many countries, often as a percentage of the gross revenues of telecommunication companies. These funds are specifically designed to extend mobile coverage to more remote areas. However, studies show that globally, over half of the sums collected for USFs were never utilized, and more than a third of the funds were not able to distribute any of the money collected. Governments will need to increase the collection and improve the use of these USFs – and we need to find credible alternatives for rolling out internet coverage to remote areas.

Fortunately, these alternatives exist. With the switch to digital TV, the analog TV spectrum can be repurposed to deliver mobile network coverage via lower frequency signals, which travel greater distances before weakening. Therefore, to cover remote rural areas, MNOs would need fewer towers and base stations than they currently require (though the economics of this will require careful management).

Another solution would be to incentivize the deployment of balloons, low-orbit nano-satellites and other sources of low-cost remote connectivity. However, this will need to be done with care, understanding and empathy. While Facebook’s Free Basics has already connected 100 million people in 60 countries, its limited internet access precludes the availability of some of the very apps that could unlock increases in income. In the words of Mike Santer, founder of BluPoint, “Western companies need to show more awareness that what works for them does not always translate to the developing world.” A better approach, he says, would be for big tech companies to partner with local organizations that understand the local language, culture, market needs and opportunities.

Social and Psychological Barriers and Solutions

However, providing access to this technology doesn’t guarantee that people will use it. Consider the fact that more than 1 billion people globally, in both rural and urban areas, cannot read or write, or understand the long number strings necessary to transact in the digital age. Natural language processing (NLP), a branch of artificial intelligence that helps computers understand and manipulate human language, can enhance these people’s ability and willingness to interact and transact with each other, and with service providers. However, most of them do not speak one of the top 30 global languages as their first language — none of which are indigenous to Africa. And for obvious commercial reasons, the languages spoken by a limited number of (often relatively poor) people are less likely to be the focus of NLP products. Furthermore, many of the poorest are women who face social barriers that exclude them from the digital revolution, even if NLP is rolled out in their language.

If we can get connectivity and smartphones into the hands of people in remote and rural villages, helping people who cannot read or understand number strings should be relatively easy. Indeed, MSC’s MoWo project is already starting this, using icons instead of words, with plans for a cash calculator with an interface specifically designed for this population. This will need to be tailored for each cultural context, but depending on the development of NLP, it may well be a more cost-effective approach for less-common languages.

That said, with the evolution of artificial intelligence, the next 20 years may see the development of commercially viable NLP for these languages. Alternatively, governments may commission or cost-share the development of NLP for the diverse languages in their countries, in order to reach excluded populations. Moreover, of course, advances in education may reduce the numbers of illiterate/innumerate people.

There is growing evidence that many low-income (and quite a few high-income) people want human touch to navigate the digital age. This is particularly valued when making decisions and resolving issues through customer support. Indeed, the uptake of digital tools often depends on the quality of this support, whether it is delivered through agents or call centers. Of course, with the growing sophistication of chatbots, significant elements of this “human touch” can actually be digitized. However, this is again contingent on the development of NLP in the languages that people actually use. Even with this technology, my guess is that on-the-ground agents will still be required, and will play significantly broader roles than their current ones.

Another key to addressing users’ psychological barriers will be to incentivize the poor to adopt and use mobile phones and digital financial services. The Government of India has shown the power of combining a national digital ID system with a seamless, interoperable payments system, using bulk digital government-to-people payments to drive uptake and usage. The poor comprise the vast majority of the 180 million people who receive direct benefit transfers from the Indian government. Paying them digitally fosters use and trust in the digital ecosystem.

Protecting Consumers in a Digital World

Currently, the financial inclusion sector is struggling to create regulatory environments, data privacy norms and consumer protection provisions that are appropriate for the digital age. The digital revolution will amplify and extend these challenges significantly over the next 20 years.

Only recently have developed countries begun to realize the implications of these changes, and they have been scrambling to respond. Nonetheless, this is an area where I foresee progress being made. Yet once again, support from a range of stakeholders, particularly multilateral organizations and donor agencies, will be essential. Regulators and policymakers will need assistance as they strive to make sense of how, and how much, to regulate and supervise – and careful tailoring for specific country contexts will be essential.

However, we all must avoid becoming complicit in the development of exploitative digital systems. These could be commercial (as I fear we may have advertently done with digital consumer credit) or political (by creating a system of social control for repressive governments) — how else can one describe China’s Social Credit system? MSC is already working on several ambitious programs to address some of these issues – from the i3 Program’s efforts to “Innovate, Implement and Impact” across Bangladesh and Vietnam, to our work with large tech-based financial service providers to design and roll out products that combine physical engagement with digital efficiency.

But as we conduct this work, we have to recognize that there is an almost irresistible temptation for corporations and governments to centralize and exploit the data from digital systems. Work on data privacy and consumer protection, as well as consumers’ own behavior to “self-protect,” will be key to ensuring that the future is not dystopian. Let us hope that this focus extends into the developing world.

I am optimistic that these problems can be solved in the next 20 years, as technology’s potential to boost social and economic inclusion is unprecedented. However, we must not overestimate its ability to deliver developmental impact for good. Technology provides us with the opportunity to do more, faster and better – as long as we don’t overlook the vulnerable, low-income, rural and remote communities that are less able to harness the vast potential of the digital age.

MicroSave Consulting (MSC), with support from UNCDF SHIFT Bangladesh, undertook a qualitative consumer behavior research to examine the gender centrality of Mobile Financial Services (MFS) in Bangladesh. The study used MSC’s Gender Centrality Framework and adopted a positive deviance approach by focusing on learning from only the women MFS users to make sense of “how and why” women use MFS. This approach helped us to recognize patterns and build a meaningful picture of the drivers of MFS use among women, and make recommendations for policy and practice. The findings were disseminated through an event in presence of regulators, providers and academicians in Dhaka on December 2018.

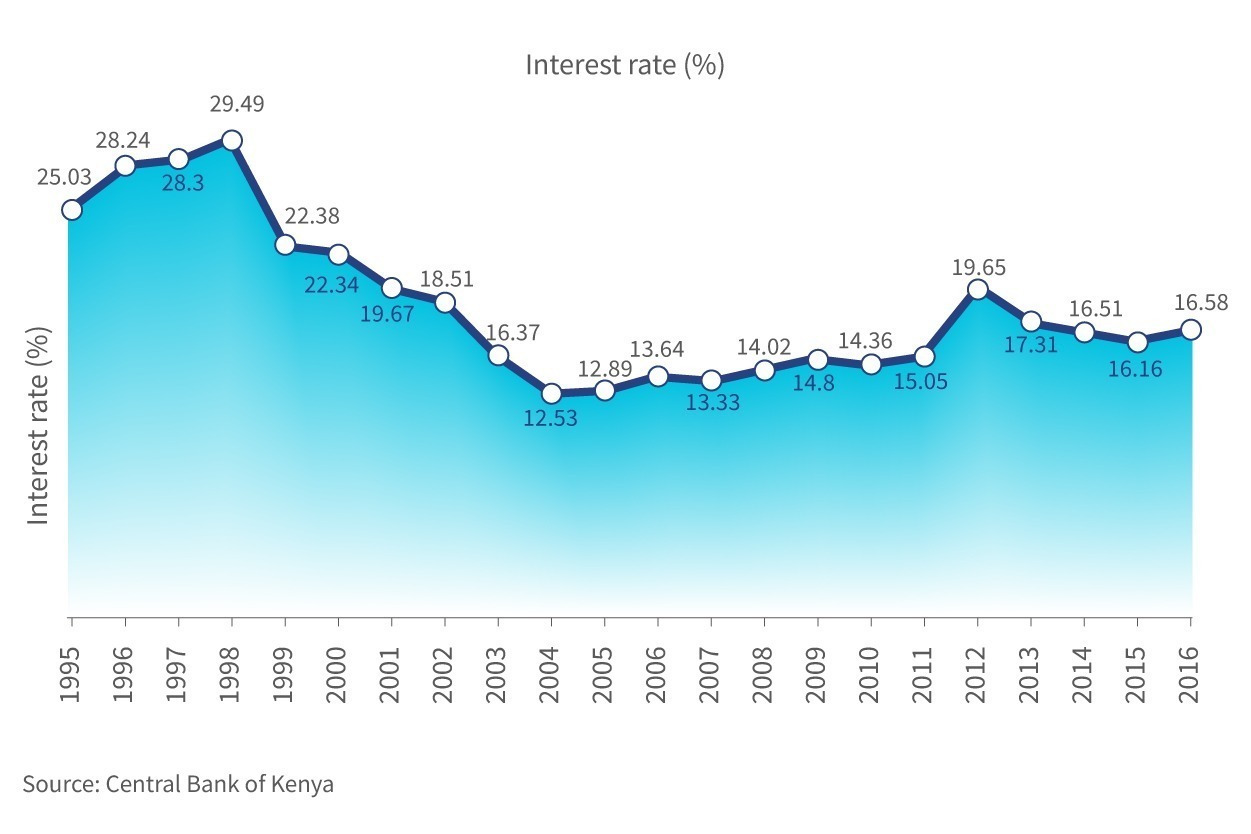

In Kenya, interest rates have historically been driven either by the market or through regulation by various amendments of the Banking Act. The weighted interest rates of commercial banks hit an all-time high over the past two decades between 1995 and 1998, averaging between 25.03% and 29.49%. During this period, commercial banks had started to diversify into the low-income segment. This segment had been considered riskier and less lucrative because of low-value transactions and, therefore, considered a preserve of microfinance institutions. The year 2004 marked the time when commercial banks in Kenya offered the lowest lending rates in recent times, an average of 12.53%. Over the next 10 years, the weighted average rates in the banking industry increased steadily and pushed towards capping the interest rates constitutionally.

Below is a snapshot of the weighted interest rates trends for the commercial banks in Kenya for the years 1995 to 2016.

In 2001, a bill was passed by parliament which introduced lending rates caps at 4% above the 91-day T-bill and deposit rates at 4% below the 91-day T-bill. Popularly known as the “Donde Bill”, banks contested it in court and the bill was reversed even after the then President had accented to it. The second attempt to cap interest rates came in 2013, where Kenya’s Parliamentary Budget Office proposed that the deposit rates be pegged to the lending rates. This too did not succeed. The two bills failed, based on the government’s preference for free-market interest rates as opposed to caps. The Central Bank of Kenya also asked banks to self-regulate and to take measures that would reduce the cost of credit—to no avail.

In a further attempt to have the banks lower their lending rates and enhance transparency in credit to the private sector, Central Bank of Kenya (CBK) introduced the Kenya Banks Reference Rate (KBRR) in July, 2014. The KBRR sought to have banks disclose and explain to their borrowing clients the effective base lending rate and any additional premium above the base rate. When it was introduced, the KBRR was set at 9.13% with a review to come after every six months. On 14th January 2015, CBK conducted a review and the KBRR was further reduced to 8.54%. However, lending rates from banks did not reduce.

Ultimately, in mid-September 2016, following various campaigns by legislators to revive the Donde Bill, CBK introduced interest rate caps through the Banking (Amendment) Act 2016. The act limits banks from charging more than 4% above the Central Bank lending rate, while the deposits attract a minimum of 7% on the benchmark. As at 28th May 2018, CBK had set its benchmark interest rate at 9.5%.

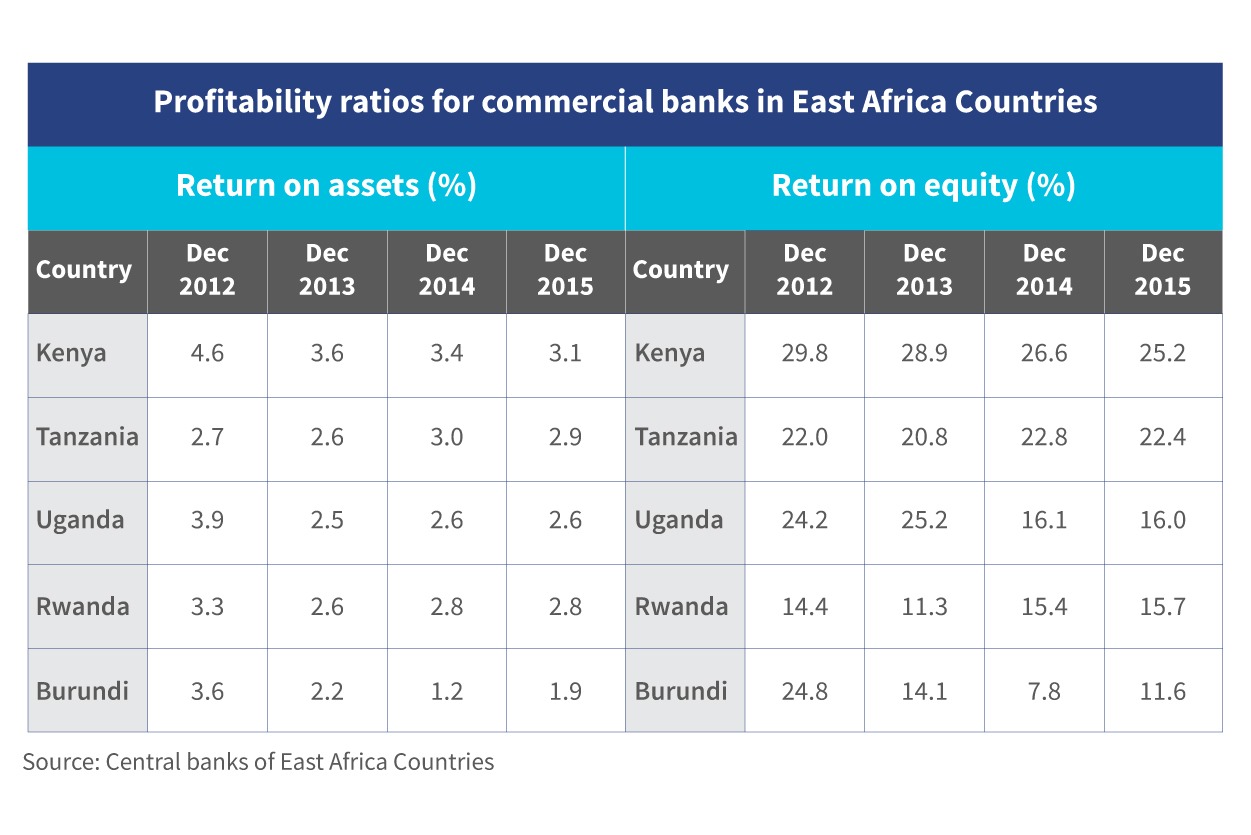

The drive towards the capping of interest rates was meant to stop arbitrary hikes in the lending interest rates, make credit more affordable, and hence promote access to credit to the private sector. Through this intervention, it was envisaged by CBK that the reduction in rate would spur economic growth and lead to the creation of more jobs while ensuring that the operations of the banks remain sustainable. An assessment of the profitability of commercial banks in East Africa countries shows that Kenyan banks were the most profitable over the period between 2012 and 2015.

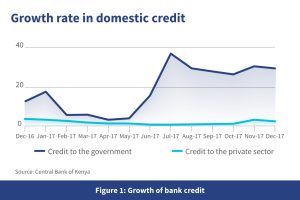

The growth of credit to the private sector registered a decline during the first nine months of the year 2017, while

credit to the government registered a huge growth as shown in figure 1. The decline in credit to the private sector was attributed to the uncertainty around the elections period as well as the stringent loan requirements following the interest rate cap. There was an increased appetite by the banks to lend to the government because of the inherent minimal risk—hence the huge growth registered in 2017.

It has now been over one and a half years since the interest rate cap came into being. Borrowers now repay loans at a maximum of 14% per annum while depositors earn a higher interest rate on their deposits. This is also true for loan contracts made before the law was passed. However, the Kenya Bankers Association’s economic bulletin of Q3 2017 shows that non-performing loans (NPLs) have continued to soar. Between the second and third quarter of 2017 alone, the gross NPLs increased by 6%. Because of the small-ticket loans from digital credit, these did not have much impact on the overall NPLs in the banking sector. The NPLs were generally attributed to the harsh business environment in the country. Figure 2 shows the trend of NPLs since the year 2011.

There have been specific impacts and outcomes in the Kenya banking sector since the enactment of the Banking Amendment Act 2016. Key among them are:

• Conversion of savings accounts into transactional accounts by commercial banks, which allows them to avoid paying interest

• An increased focus on digital lending models—Equity Bank, Co-operative Bank, and KCB have been disbursing small loans using digital channels; digital loans are usually priced higher than the cap

• An increased focus on digital channels with banks, such as Bank of Africa closing down some of its brick-and-mortar channels

• Tightened loan requirements to mitigate default risks previously covered by higher interest rates—Loan requirements have become more stringent, particularly for entrepreneurs that do not have immovable collateral to secure loans

• A decline in consumer lending, as the segment has now been profiled as “risky”, following the caps

• Increased fees, such as loan processing fees to mitigate declining income from loans

• Increased demand for credit from SACCOs, MFI, MFBs, and informal financial lenders—while the interest margins for these lenders are quite exorbitant, they do offer stress-free collateral requirements compared to commercial banks.

What is next for the banking industry and the borrowers?

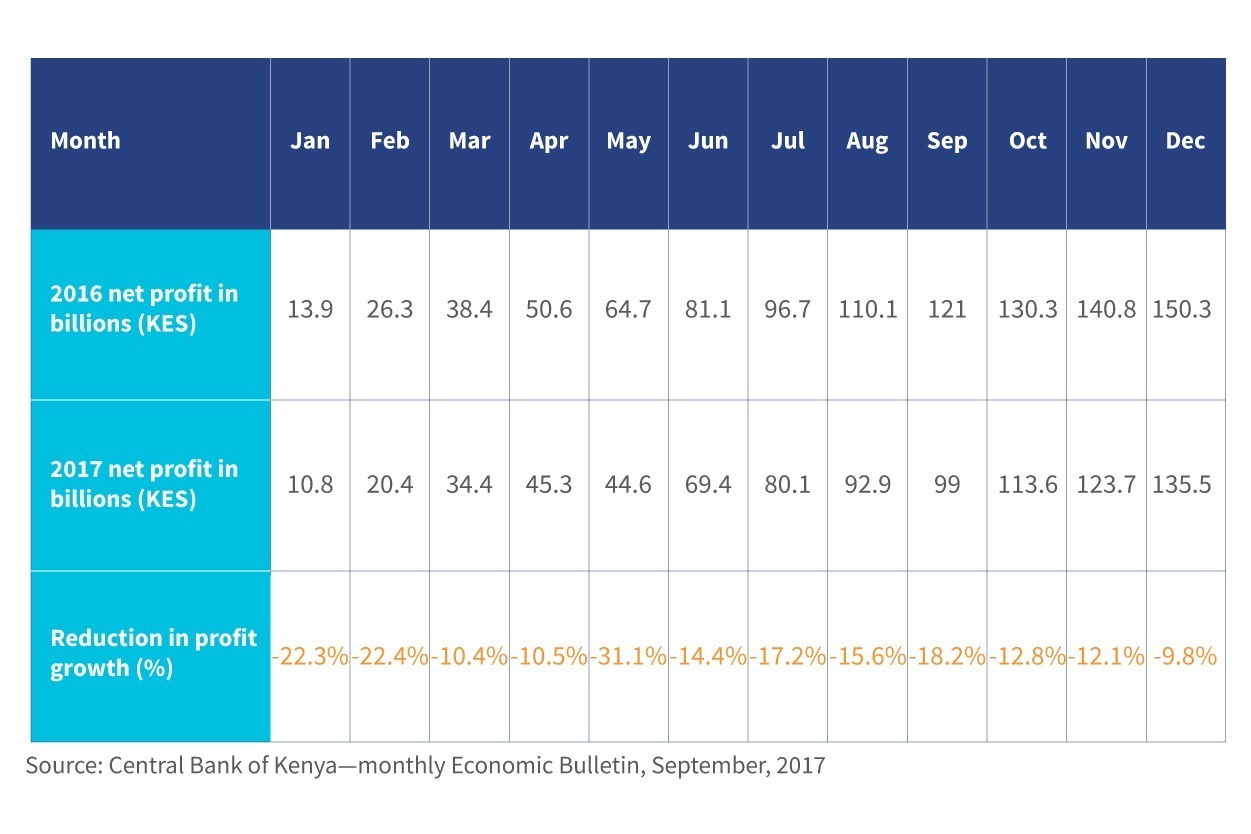

The strategic changes made by commercial banks to comply with the interest rate caps and the protracted disputed election of 2017 have had an adverse effect on the Kenyan economy. Profitability for the commercial banking sector in 2017 slowed down compared to 2016. The table below shows the profitability of banks in Kenya over 2016 and 2017.

In addition, the enforcement of the International Financial Reporting Standard (IFRS) #9, which took effect on 1st January, 2018, has triggered a preference for shorter loan tenures and relatively smaller loans to reduce the risk of default among borrowers whose credit rating is low. With all these in mind, banks are likely to be even more stringent in lending to minimize default. Access to finance, especially for entrepreneurs, is likely to be even more difficult.

The question is—where do these dynamics place the borrowers? If they wish to access loans easily in the future, borrowers need to have a good repayment record. Borrowers may need to be educated and sensitized on these developments to promote awareness and thus improve their loan repayment discipline.

Applying more stringent loan requirements means a reduction in lending, which may lead to reduced profitability. For the borrowers, a reduction in access to credit may further slowdown wealth creation and thus slow economic growth.

Banks have been pushing for the act to be repealed since its enactment. IMF has also supported the proposal to repeal the act. During the 2018-2019 annual budget speech, the Cabinet Secretary to the National Treasury proposed a repeal of the Interest Cap Act, citing its adverse effects on financial access and economic growth. Kenya has already witnessed a reduction in credit growth to the private sector from 13.5% in 2016 to 2.8% in April, 2018.

On 14th March 2019, the high court of Kenya ruled that the law that caps interest rates at 4% above the Central Bank rate is unconstitutional. However, a 12-months’ window has been provided from the date of the ruling for the parliament to reconsider the provisions of the act. Given this ruling, consumers of credit, that is, the private sector, are not sure whether interest rates will increase once again to previous levels where credit affordability was a burden. Meanwhile, the question remains—which is the better option for credit consumers, the financial sector, and other stakeholders?

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.