The Tanzania Country Report is based on a national representative sample of over 2,000 mobile money agent surveys carried out in 2013 all over the country. The report paints a picture of a dynamic and competitive mobile money market in Tanzania with profitable agents, focusing on the country’s operational factors of success and persistant challenges.

Key findings from the report:

– Agents are overwhelmingly profitable, with 49% earning at least $US 100 per month in profits, compared to only 40% in Uganda.

– Over 70% of Agencies are ‘new’ (having been in operation for a year or less) demonstrating aggressive growth in the market, however the small percentage of ‘old’ agencies suggests they have a short life-cycle.

– Rapid growth and the non-exclusivity of agents is putting pressure on agents’ liquidity, with 5 transactions a day being denied due to lack of float

– Competition is resulting in better support, with 79% of agents receiving training, but improvement are still needed in targeted areas.

The Helix Institute of Digital Finance’s second Agent Network Accelerator (ANA) report based on a nationally representative survey of 2,052 agent networks in Tanzania, coupled with extensive qualitative interviews across the country, provides extraordinary insights into agent networks in Tanzania.

The survey includes all providers offering agent banking or mobile money services, taking special interest in the country’s three main providers: Vodacom, Airtel and Tigo. These three providers absolutely dominate the market and continue to grow at quite robust rates, pioneering a unique model for developing agent networks which can be used as a paradigm for providers around the world. The data also shows where providers need to focus their energies in order to improve the quality of the agent networks in the country, which is imperative at this juncture when many providers are looking to stack more sophisticated services (like banking products) over them.

Uniquely Non-Exclusive Agents:

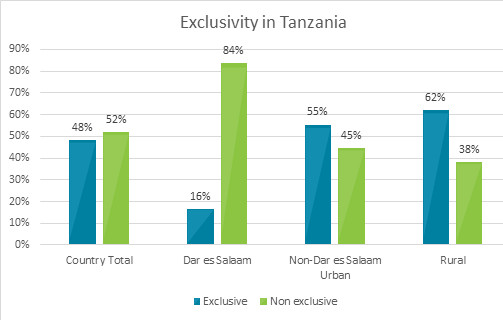

If an agent offers services for more than one provider, it is considered “non-exclusive” and in markets like Kenya, and Uganda where there is a clear market leader, the majority of agents are only able to serve the leading provider. However, most markets do not have that dominance, and Tanzania is a better model for them. In Tanzania, about half of all agents are non-exclusive, and in the capital of Dar es Salaam, it is 84%. This means agents are able to conduct transactions for and earn commissions from multiple providers, leading to a very small number of agents being unprofitable (4%), and agents earning a healthy median profit of $US 95 per month.

It is however, noteworthy, that almost two thirds of agents in rural Tanzania are still exclusive. This is an artefact of Vodacom being the first to aggressively expand beyond urban areas, but now competitors are following suit and therefore we expect it to be increasingly non-exclusive in the future.

Agent Liquidity Shortages:

While the high levels of non-exclusivity of agents buttresses profits, it also causes liquidity shortages for the agents (agents are forced to manage separate liquidity pools for different providers since systems are not interoperable). This is compounded by agents who are not motivated to actively manage their liquidity, preferring to wait in their shops until customers make transactions which gives them the needed liquidity instead of traveling to a rebalance point.

This has many effects on the character of the agent network. For providers, it means that it is hard for them to maintain agents where rebalance points are far away (rural areas). In the paper,Where’s The Cash? The Geography Of Cash Points In Tanzania, Ignacio Mas and Agathamarie John found that 83% of Vodacom agents are located within five kilometers of a bank branch. The Agent Network Accelerator (ANA)report highlights that 69% of agents take 15 minutes or less to reach their rebalance point, reinforcing the finding that agents are still tethered to rebalance points, and it is constraining the expansion of agent networks to rural areas.

Insufficient liquidity further damages the business model and reputation of agents where they are located. The ANA report emphasizes that lack of liquidity at the agent level causes the loss of an median of five transactions per day (14% of median transactions per day), and of course will damage agents’ reputations as dependable and trustworthy service provider complicating the future ability to offer banking services through these networks. Clearly there is a huge potential for providers to help improve liquidity management at agents – through the use of master agents (commonly called aggregators in Tanzania) and, in the longer term, interoperable systems that will eliminate the need to keep multiple liquidity pools. In the meantime agents are setting up informal arrangements with other agents and shopkeepers in their locality to try to mitigate the liquidity challenges.

The Future of Digital Finance in Tanzania

Tanzania has certainly crafted a unique and impressively successful ecosystem for mobile money. It is much more developed than Uganda in terms of the quality of agent support, and the profitability of agents. It is even leading Kenya by pioneering the non-exclusive agent network model. However, the Agent Network Accelerator report shows that fraud is still plaguing its network, liquidity management issues are rife, and it is still having trouble with account opening for new customers.

Tanzania is full of potential, yet really still in its infancy with product development. While agents in Tanzania mainly only provide cash in/out services for people’s mobile wallets, there is a lot of talk about deeper integration with banks to offer services like savings and loans, and there is already the beginnings of a merchant network being built where people can use mobile money to pay at retail outlets. However, these frontier innovations will continually be stifled by some fundamental operational issues in the agent network that need to be addressed in order to support these and other more sophisticated services to be offered across the country.

Attracting household savings and private sector investments will speed up WASH coverage and can be considered to be one of the most cost effective public health interventions. Microfinance can play a catalytic role in increasing the uptake of WASH improvements by poor households. But WASH financing differs from the generic income generating loan (IGL) product significantly, and there are several other strategic issues that determine the suitability for rolling out WASH finance. MFIs have to consider these issues carefully before embarking on a WASH product development exercise. In this Note we explore some key strategic issues that determine the potential for a WASH finance portfolio including ecological factors, the public good nature of WASH, usage level of existing WASH infrastructure, capital for WASH financing, collaborations with WASH product/service providers and awareness amongst potential WASH financing customers.

No one really disputes the idea that both financial inclusion (defined by the Reserve Bank of India (RBI) in a recent report as “the spread of financial institutions and financial services across the country”) and financial depth (which India’s central bank describes as “the percentage of credit to GDP at various levels of the economy”) are important, necessary—and very possibly in trouble.

At least in India. Others around the globe, including of course the World Bank, agree that formal banking and related services may help improve economic prospects for the estimated 2.5 billion currently unbanked. They also readily acknowledge the problems involved.

Almost none of these others, however, have quite the same daunting numbers and demographics that India must deal with—269.3 million, or 22 percent of the population, living below the national Planning Commission’s poverty line of Rs.26-Rs.33 (45-55 cents) per day, depending on the area, already far less than the $1.25/day World Bank norm for “extreme poverty”. And approximately double the numbers politically-defined as “poor” are still unable to read a bank statement.

In the past five years, RBI has worked harder than many central banks in developing countries to offer at least limited financial services, especially in rural villages, and to coerce retail banks to comply with financial inclusion directives. Nevertheless, RBI’s recently released Mor Committee Report, referred to above, reveals new and worrisome realities:

– Almost 90 percent of small businesses in India still have no links with formal financial institutions

– 60 percent of the rural and urban population do not have a functional bank account.

– Bank credit to GDP ratio in the country as a whole is 70 percent, but in a large, very poor state such as Bihar, it is dramatically less at 16 percent.

– Savings, even for the not so very poor,are declining and, in certain areas, moving away from financial to physical assets. And less than fully regulated savings often include less than fully scrupulous providers.

Reasons cited for this trend include lack of positive real return and difficulties in quick, direct access to savings accounts.

Savings as a proportion to GDP have fallen from 36.8 percent in 2007-08 to 30.8 percent in 2011-12 (most recent figures available) and household financial savings declined from 11.6 percent of GDP to 8 percent during the same period.

– Credit and access to equitable financing for low-income households and small businesses is, in very poor areas, even less encouraging.

Many retail banks fail to comply with RBI’s Priority Sector Lending (PSL) guidelines, which require a full 40 percent of their lending to these sectors, for the simple reason that their non-performing assets (NPAs) are almost double.

For more on Mor Committee, please see MicroSave’sblogs:

Independent, external sources fail to paint a rosier picture. The World Bank’s Global Findex pegs India’s unbanked at 65 percent, not 60, and note that only 4 percent use formal bank accounts to receive welfare payments. In theory, all beneficiaries of India’s many, various welfare and pension must have a basic savings account. The reality is that many districts still use CICO (cash in/cash out) agents for distribution. A MicroSaveoverview explains some of the reasons why.

Of the 182 million-plus such accounts that are on RBI’s books, at least half—possibly far more—are either dormant or “pass-through” accounts only. (Beneficiaries pull out their full government disbursement each month and fail to save in small increments or invest in micro-insurance policies).

So, if full financial inclusion is NOT happening in India, and probably not even progressing by most important metrics, why is this the case and how might things improve?

MicroSave has spent the last several years trying to answer these questions by talking directly to the financially excluded all over India, to the bankers required by RBI to serve their needs, to the “business correspondent” managers and agents in both urban and rural locations who actually do serve their needs, and to the RBI and other policy-makers who are in fact trying hard to make this work.

Our research indicates the following key culprits:

– Skewed incentive structures for the agents that only rewards account opening, not transactions and active account use;

– The wrong products and services for this clientele who need, and are willing to pay for, more “normal” services such as ATM cards and limited, short-term credit;

– Poor and wrongly targeted marketing and promotion efforts for the few such as recurring flexible savings deposits and remittances which do seem viable. More corporate marketing strategies—like the campaigns one sees everywhere in India for soft drinks and mobile subscriptions—would work more effectively for these targets.

– Banks’ limited enthusiasm for low-net-worth customers and most aspects of financial inclusion (please see “Credit” and NPAs above and related MicroSave research on this topic).

This is the short list. For the much longer litany of woes, please visit MicroSave’s online library and type in “financial inclusion” or whatever keywords best suit your needs.

India is not alone in needing to address these and related problems—and, no, technology, mobile operators, and global credit-card brands are not the all-purpose solutions some would have us believe. As the world’s largest democracy and second-most-populous nation, India has a certain responsibility to think more creatively and implement more effectively for full financial inclusion. If and when it does, the rewards will also be that much more noteworthy and gratifying for all involved.

The recently released 2013 GSMA Mobile Money Unit (MMU) State of the Industry report and the State of Mobile Money Usage are filled with encouraging statistics and upbeat projections for the existing and new services the GSMA supports worldwide.

On paper, the state of the industry and usage are splendid: 219 mobile money services in 84 countries, with more in the works for 2014, with 203 million registered users (as of o6/13), compared with 108 million a year earlier. Approximately 61 million were “active”, (one transaction in three months), 37 million were “more active” (at least once in a month).

The Global System for Mobile communications, an open, digital cellular technology used for transmitting mobile voice and data services, also enjoys 80 percent world dominance (or “market share “ if you prefer). Adoption and usage figures, in particular, are interpreted differently from what MicroSave sees in daily fieldwork and CGAP (the World Bank’s Consultative Group to Assist the Poor) discovered in an extensive follow-up several years ago.

Even the GSMA acknowledges that only 13, or a very small 6 percent, of their MMU services, have reached “scale” with at least one million users. MicroSave’s a recent blog on mobile bill payments and sustainability and an earlier one, Mobile Money–Rosy vs Real, point up the many unresolved security, fraud, interoperability issues and basic user problems like a widespread inability to remember passwords that tend to be glossed over in the blockbuster reports.

The interesting part of this problem, however, is not the figures or forecasts—glowing or glum—regarding relative rates of adoption, but WHY. What are the reasons behind quick uptake and regular use versus general indifference to sending and receiving money by phone?

Here is a brief list that may prove helpful from our own experience:

– Mobile operators often play the most important role. Others–including Cash In/Cash Out (CICO) agents, employers, government welfare payments—are also key to customers successfully adopting a mobile money service, but it begins with the network operator. Unlike the banks, operators want these customers and most are only too happy to add payment services to airtime top-up and more phone sales whenever the law allows.

– Providing a rationale. MNOs can also do mass marketing. The most famous is of course Safaricom’s “Send Money Home” slogan which resulted in 18 million active M-PESA users, but Eco-Cash from EcoNet In Zimbabwe (“I pay with Eco-Cash because I don’t like being short-changed”), Telenor’s EasyPaisa in Pakistan (“Changes my

life through convenience”) Telesom’s ZAAD (“Transfer, Save, Buy”) have all managed to convey simple, compelling propositions to an initially less than eager public.

– Those paid by phone, especially those paid via a full-frills bank account, are much more likely to continue paying by phone. If everyone reading this were still remunerated in cash, most of us would not pay bills online or use debit/credit cards for daily purchases. The real problem, as discussed by James Militzer and Ignacio Mas in a recent blog, is where the money begins.

For the non-salaried poor, it begins as wadded-up bills and coins. Which then require time, effort and, too often, a fee to convert to mobile money via a CICO agent. Periodic withdrawals always involve fees and the same difficulties in reverse so, for most migrant and domestic workers, cash stays cash.

G2P and remittance beneficiaries may receive electronically, but the urge is overwhelming—and common sense would certainly encourage most recipients—to pull the money out when it arrives. Periodic withdrawals are too expensive and without easy access to ATM cards and machines, too inconvenient. (Please see MicroSave’s two recent blogs on the specific logistics of G2P payments in India for more details.)

– Tempting though it is to blame the agents for everything wrong in financial services for the poor,and critical though their role is in selling mobile payments to customers, there are other key links in the chain that also need strengthening—specifically merchants, institutions, individuals willing to receive non-cash payments.

No m-payees, no m-payment system. This is the tricky bit too many policymakers and planners gloss over. In the mid-1980s, no one—not even VISA and MasterCard—wanted to participate in online payments. And supermarkets emphatically didn’t want debit-card/PIN readers cluttering up the check-out counter and slowing traffic. Change is only easy and obvious in retrospect. (See below for why everyone ultimately came around. It wasn’t just because paychecks became virtual.)

– Seeing is believing…sometimes. MicroSave recently observed a group of rural Indian women who, when offered the opportunity to repay their monthly microfinance loan by phone, all declined. With all the usual excuses. Their husbands had never heard of such a service. Nor had their far more tech-savvy children. Why would they trust something unknown no one else was using?

Live demos helped. Targeted marketing and advertising with trusted, recognizable logos helped even more. One person in the group trying and succeeding was perhaps the most effective, but adoption remains cautious.

Trust is hard to build and difficult to maintain. Introduce any extra fee, however small, during the transition from cash to mobile payments, or make PINs too hard to remember or recover, and no amount of marketing and hands-on help will bring your users back to the phone.

We also have a fundamental disconnect in transferring the idea of digital payments—be they by phone or point-of-sale cards—from industrialized Western economies to developing parts of the world where most people still don’t have bank accounts

In the West, the rationale was uncomfortable but simple: sales clerks, ticket sellers, cashiers, tellers, accounts payable & receivable departments are all too expensive; machines, even the ones that need 24/7 maintenance, are cheap and incur no extra cost when they break or become obsolete. Sold to customers as faster, more convenient, and always available, these never were and still aren’t the real reasons banks, mobile operators, utilities, and merchants tirelessly promote and improve electronic funds transfers, online banking, ticket machines, bar-code scanning, and all other, ever-expanding New Ways to Pay.

The real reasons change in places where human labor is as cheap if not cheaper, and often more reliable, than technology. Most banks and mobile operators, not to mention the m-payees (see above), need a stronger impetus than increased mobile use and financial inclusion to invest in the significant demands digital payments will impose. Fraud and authentication, already a ~$3.5 billion cost for U.S. mobile payments, will be argument enough for many to pause and reconsider.

We should do it anyway. Even though users don’t really want mobile payments yet. (They aren’t faster, more convenient, more available, and probably won’t be for a good long while.) Even though most mobile operators and others won’t enjoy much, if any, return on their investments for the same longish, discouraging time periods.

The GSMA MMU and Safaricom are, maybe, just this once, right to over-hype their successes. Mobile money and a mobile account are still a better, more secure alternative than cash. And until we come up with a more viable idea, they will only become more so.

Speaking with us, Puneet Chopra, MSC’s Domain Leader- Digital Financial Services: Banks/Product Innovation, shares his views on business correspondent model in India and explains how interoperability of BC channels can enhance the confidence of stakeholders, such as the government, banks and BCNMs, in the system. Taking the conversation ahead, he observes the dichotomy of what is available to the mainstream consumers versus the poor and voices the pertinent question on everyone’s minds — Do the unbanked population really need interoperable services? Do they need services like their mainstream counterparts or peers?

Sighting MSC’s study findings, Puneet observes that there is a strong business case for banks and BCNMs in support of greater integration and interoperability, underlying usage of technology, better security that can be enabled through this channel and greater interoperability to benefit the end client.

Manage Consent

We use cookies to ensure your experience on MSC Global is secure, reliable, and optimized. By continuing to browse www.microsave.net, you agree to our use of cookies as described in our Cookie Policy.

Strictly Necessary Cookies

Always active

Required for website security, authentication, and essential functionality to provide a secure and optimized experience on Microsave.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Performance and Analytics Cookies

Used to improve website usability and reliability through anonymous analytics and usage insights on Microsave.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Functional Cookies

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.