Aadhaar is a unique digital identity issued by Unique Identification Authority of India (UIDAI). It is a database with no duplicates which serves as an identity and address proof. More than 1.25 billion residents have enrolled themselves in it. It has been a game-changer in streamlining digital payments in India, including G2P payments. In the midst of COVID 19 crisis, the Indian government has been able to support the vulnerable sections of society via cash transfer support. The government transferred USD 7 billion benefiting more than 200 million households in the country.

Innovations and coping strategies for food security at the time of COVID-19

COVID-19 is likely to have a widespread, deep, and prolonged impact on every sector and segment. Farmers and cultivators in countries like India are rapidly starting to bear the brunt of the pandemic, even though restrictions and lockdowns have largely spared agriculture and allied sectors. The disruptions have affected the long value chains between cultivators and consumers. Retail prices have shot-up, wholesale prices continue to fall, while producers struggle to find buyers for their produce. In many areas, farmers lack access to adequate labor or equipment to harvest standing crops.

The impact on the next cycles of cropping is going to worsen as several factors start to play out. These include constrained logistics of input supplies to farmers, an anticipated shortfall in the availability of credit, subdued demand, unpredictable consumer behavior, and reduced buying power. Sadly, the worse may be yet to unfold!

What can players in the ecosystem do amid the gloom? Are there innovative and practical solutions to aid food security? Can we prevent massive wastage or losses and protect the livelihoods of smallholders?

Lessons from innovative ideas and approaches, and their rapid replication

India is known for its frugal and rapid innovations, termed colloquially as jugaad. Agtechs and other stakeholders in agri value chains are trying innovative approaches to reduce the fallout of COVID-19.

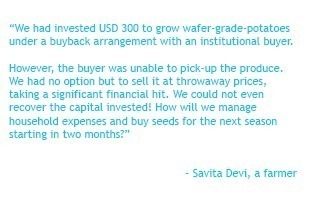

Savita Devi, an Indian Farmer

Lessons must be learned quickly, evaluated, and those that work should be scaled up. Governments, private players, investors, and start-ups will need to recognize solutions with high potential and invest in them to expand them rapidly. These are trying times like never before. Yet they also offer opportunities for unprecedented innovation, learning, and evolution of collaboration models.

Let us start at the consumer end. Household demand for staples and perishables is still high. We can say that this demand is reasonably inelastic, especially in urban areas and in the near-term. Closure of restaurants and workplaces has expanded demand somewhat, at the household level. Moreover new demand centers like community and government-sponsored kitchens have surfaced.

Entrepreneurs have developed simple demand aggregation solutions using Google Forms or over WhatsApp messaging. Once logistically feasible demand is generated, for example, a suitable truckload, entrepreneurs are completing fulfillment directly from farm gates. Agri-techs can do this either directly or in collaboration with active farmer cooperatives or producer organizations. Noteworthy examples include Praakritik, Sahyadri Farms, and Loop from Digital Green.

Based on anecdotal evidence, farmers who have been able to connect through these entrepreneurs are harvesting under-ripe fruits and vegetables. Earlier, market intermediaries would undertake the ripening process down the value chain. However, the current trend—and fear of coronavirus—makes consumers store fruits and vegetables for a couple of days before consuming them. This means that ripening is now happening on the shelves of consumers. This is beneficial for farmers as it reduces wastages. Moreover, the farmer has factored the increased time required to get the produce to the consumers with the prevailing lockdown in place.

Governments, such as in Maharashtra, are trying to devise innovative solutions. They have tied-up with leading farmer producer organizations to supply produce directly to households. However, logistics and fulfilment needs considerable strengthening. Getting to scale with such models is the challenge. Agri-techs that have robust farm-to-fork supply chains can provide important lessons.

Governments should collaborate with agri-techs that have the outreach and are capable of scaling up, rather than trying to create impromptu farm-to-fork supply chains.

Governments should collaborate with agri-techs that have the outreach and are capable of scaling up, rather than trying to create impromptu farm-to-fork supply chains.

As we move up the value chains, wholesalers and aggregators are facing a slowdown in demand from retailers and vendors. This is because of a combination of issues related to logistics and the partial closure of retail markets. Overall, wholesale prices are being driven down while the agriculture value chain from farm to fork faces many roadblocks. The friction in the supply chain has multiplied because of the lockdown. Reduced wholesale prices and increasing retail prices reflect the situation—not a happy one for either the farmer or the consumer.

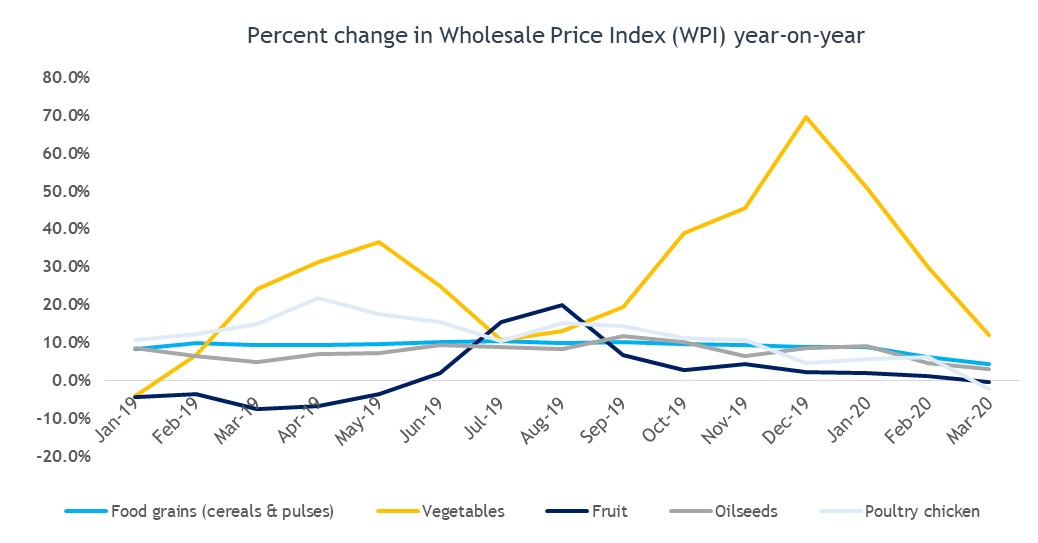

The year-on-year trend in the Wholesale Price Index (WPI) for food grains, oilseeds, vegetables, fruit, and poultry exhibits a sharp downward trend. The disruption in retail supply chains of food grains and perishables is causing uncertainty in supplies and fluctuating prices. Meanwhile, panic buying and hoarding by high-income segments have started to create shortages for low-income segments.

Department of Co-operation, Marketing and Textiles, Maharashtra

Percentage in Wholeprice Index

Source: Government of India, MSC analysis

Governments and local bodies need to streamline operations of agri-markets even as they ensure safety. Some states have staggered the working hours in markets, with separate timings for buying fruit and vegetables and longer opening hours throughout the day. Wholesale agri markets are functioning from midnight to early morning in some districts in Uttar Pradesh. This discourages retail buyers from flocking to these markets in search of bargains. Other states are identifying new marketplaces to expand space for agri-transactions while reducing mass gatherings.

The critical role of self-help-groups

Low-income segments receive a significant part of their food supplies through the Public Distribution System (PDS) in India. Women self-help groups (SHGs) can play a vital role in strengthening the distribution of food grains. In the state of Bihar, SHG members undertake distribution of a select basket of food grains for the low-income households. This is managed through a World Bank-supported Food Security Fund (FSF) program.

In the state of Uttarakhand, SHGs and village organizations are actively involved in cleaning, sorting, packaging, and distribution of a basket of food grains. The state government has gone a step further to broaden the food basket to include local millets, which add nutritive value while catalyzing demand from local smallholders—thereby adding to their revenue streams.

SHGs and women cooperatives have proven their agility in this time of crisis. They are actively involved in producing new categories of products that are in demand. These include fabric masks, aprons, sanitizers, and soaps. The state rural livelihood missions (SRLMs) drive most of the SHG programs. State governments need to share lessons across different SRLMs and replicate innovations and best practices to achieve better outcomes.

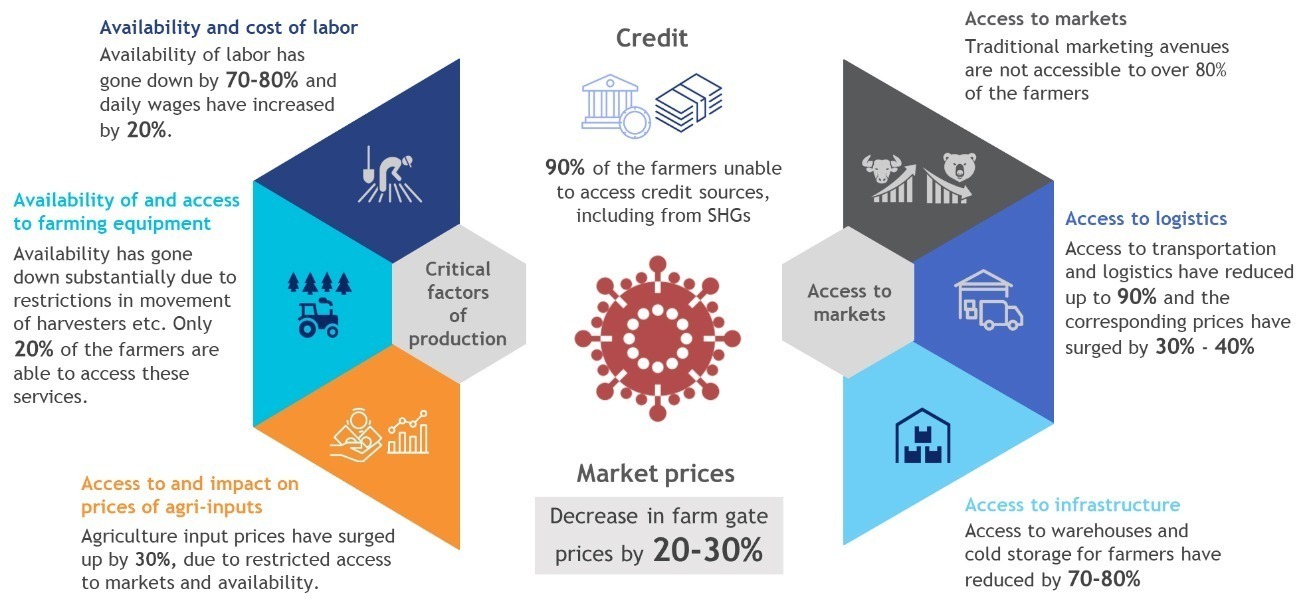

We now analyze how farmers, who are at the top of agri value-chains, are coping. MSC conducted a short research exercise with a few farmers, rural aggregators, and traders. The following exhibit summarizes the situation of the farmers and the distress they face.

Indian Market price and production illustrator

Farmers are suffering substantial economic losses due to disruptions in market access, logistics, and prevailing uncertainty.

They are uncertain and scared of threats and challenges related to their harvest-ready Rabi (winter) crops.

Harvested crops are either being sold at extremely low prices or are being stored in non-conducive conditions. Reports have emerged of farmers burning their standing crops, as the economics of harvesting them and transporting them to markets are not feasible.

Harvested crops are either being sold at extremely low prices or are being stored in non-conducive conditions. Reports have emerged of farmers burning their standing crops, as the economics of harvesting them and transporting them to markets are not feasible.

Burnt crops

Farmers are even more apprehensive of the upcoming Kharif (summer) cropping season. They are uncertain about the crops to plant. The situation of the market and the logistics at the time of harvest are unpredictable. The farmers are also concerned about the unavailability of farm inputs and credit.

Livestock farmers are equally distressed. For example, poultry prices have dropped more than 90% during the past two months. This is partly due to the unfounded belief that coronavirus can be transmitted through poultry.

Potential solutions for farmers

At this point, governments must undertake widespread communication with farmers and MSMEs in agri and allied sector value chains to allay fears, address misperceptions, and outline measures and interventions being taken.

MSC is planning to undertake a research project with farmers, traders, and other intermediaries. This will generate last-mile insights for policymakers and the sector at large, based on ground validated realities. Governments and policymakers should make informed decisions, determine appropriate responses, and calibrate actions to support smallholders and their families.

Under the leadership of JEEViKA and with support from the Bill & Melinda Gates Foundation, farmer producer companies (FPCs), MSC, DeHaat (Agrevolution), and other partners have been working together to support smallholder farmers in Bihar. One of the interventions is to provide timely offtake and optimal value realization for the harvest-ready maize crops of farmers. DeHaat has an innovative model of continual physical and digital (phygital) engagement with farmers throughout the year by meeting their needs for inputs, advisory, marketing, and credit linkages.

Under the leadership of JEEViKA and with support from the Bill & Melinda Gates Foundation, farmer producer companies (FPCs), MSC, DeHaat (Agrevolution), and other partners have been working together to support smallholder farmers in Bihar. One of the interventions is to provide timely offtake and optimal value realization for the harvest-ready maize crops of farmers. DeHaat has an innovative model of continual physical and digital (phygital) engagement with farmers throughout the year by meeting their needs for inputs, advisory, marketing, and credit linkages.

MSC is also exploring partnerships with innovators like GrainPro to provide low-cost hermetic storage facilities to farmers and FPCs. Farmers are unable to transport produce to warehouses or to markets. Temporary storage solutions at their farms or homes, therefore, can provide immense value. These will allow farmers to store grains for the short-term without infestation, degradation in quality or moisture levels, and thereby allow them to retain value.

A bag of grains

India has several innovative models similar to those of DeHaat and GrainPro. They include Kamatan, Crofarm, Ninjacart, WayCool, and many others. These institutions work across India on diverse agricultural or horticultural commodities while others like S4S Technologies, OurFood, and Ecozen provide smart and low-cost primary agri processing and storage solutions.

The country now also has a range of custom hiring centers (CHCs), some with Uber-like models. They can meet the shared needs of farm equipment economically and efficiently, particularly when availability is severely constrained.

The current situation provides an opportunity for governments and other stakeholders to collaborate and scale-up outreach that many of these MSME models find it difficult to achieve on their own. Farmer producer organizations and companies too can be important partner institutions in this multi-stakeholder approach, as the country prepares to ensure food security for all and to protect the livelihoods of farmers.

MFI client awareness comic on Coronavirus

The COVID-19 pandemic has brought upon us the responsibility to create awareness, influence precautionary behavior, and drive safety of the weak and the vulnerable segment. These books can be customized to meet the needs of country-specific guidelines, institutions, and customers. Feel free to spread them around and join us in fighting back. #staysafe

The work has been commissioned by MetLife Foundation.

Access the global version with social distancing (1 meter) here.

Access the English version (with group meeting) for Indian MFIs here.

Access the English version (for individual meeting where group meeting is not permitted) for Indian MFIs here.

Access the Hindi version (with group meeting) for Indian MFIs here.

Access the Hindi version (for individual meeting where group meeting is not permitted) for Indian MFIs here.

Access the Bangla version (with group meeting) for Indian MFIs here.

Access the Bangla version (for individual meeting where group meeting is not permitted) for Indian MFIs here.

Access the Bengali version for Bangladesh MFIs here.

Access the English version for African MFIs here.

Access the French version for African MFIs here.

MFI employee training comic on Coronavirus

The COVID-19 pandemic has brought upon us the responsibility to create awareness, influence precautionary behavior, and drive safety of the weak and the vulnerable. MSC has developed a series of collaterals in the form of conversational comics that can help microfinance institutions (MFIs) inform their frontline staff members on workplace safety, safe cash handling, customer etiquette, and personal safety measures. These books can be customized to meet the needs of country-specific guidelines, institutions, and customers. Feel free to spread them around and join us in fighting back. #staysafe

Access the global version with social distancing (1 meter) here.

Access the English version (with group meeting) for Indian MFIs here.

Access the English version (with individual meeting where group meeting is not permitted) for Indian MFIs here.

Access the Hindi version (with group meeting) for Indian MFIs here.

Access the Hindi version (for individual meeting where group meeting is not permitted) for Indian MFIs here.

Access the Bangla version (with group meeting) for Indian MFIs here.

Access the Bangla version (for individual meeting where group meeting is not permitted) for Indian MFIs here.

Access the customized version in Bengali language for Bangladesh MFIs here.

Access the English version for African MFIs here.

Access the French version for African MFIs here.

Access the Arabic version here.

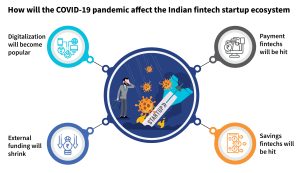

How will the COVID-19 pandemic affect the Indian fintech startup ecosystem: Four predictions and one suggestion

Around the world, the COVID-19 pandemic has changed the way we think about life and work. India remains in lockdown as field operations have been shut down and work-from-home is implemented across the board. Much of the fintech startup ecosystem will have to wait and watch to see how the situation unfolds after the official lockdown is over.

However, some early trends signal what is in store:

Digitalization wave

We will see digitalization happening across the board, from processes, to how employees interact with each other, to how the banks, fintechs, and other players reach their customers. Let us look at a few examples:

Functioning of microfinance institutions (MFIs) and non-banking financial institutions (NBFCs): MFIs and NBFCs have traditionally been driven by physical methods of cash collection, physical verification and onboarding of new customers. With the new normal of curtailed physical interactions, these institutions will seek ways to transform their physical and manual processes into automated and digital ones. They will look toward fintechs, especially start-ups, as they can support the MFIs and NBFCs in making this change with lower costs and quicker turnaround.

Agricultural practices: The COVID-19 pandemic will affect the incomes and modes of payments of farmers. In India, agricultural practices are largely labor-intensive and manual. This applies to tilling, plowing, sowing, and harvesting. Farmers also need to physically visit lenders—private money-lenders in most cases—and must get cash to revisit and repay their loans. The farmers, especially small landholders who have feature phones and even smartphones generally use them to consume entertainment content. We anticipate a big change coming here. Due to the restrictions imposed because of the pandemic, many lenders will embrace the idea of digital payments and farmers will thus be aligned to do so as well. In the coming months, digital payment collections should see large-scale adoption in rural areas through methods, such as UPI, IMPS, and auto-debit facilities, such as NACH.

E-commerce and its effect on payment fintechs

A major bulk of revenue for fintechs that work in payments comes from transactions in the e-commerce industry. E-commerce platforms like Flipkart and Amazon India sell a mix of non-essential and essential items. Because of the COVID-19 pandemic, these online retailers have recently stopped selling non-essential items in the short to mid-term, or between a few weeks and a few months. Since the essential items that are now sold on these platforms have low margins, the private digital payment companies or payment fintechs in India will see their revenues shrink. This will be because their margins ride on the volumes and values of transactions. With essential services being sold more frequently, despite higher volumes being sold, the effect on the margins on these low-priced goods will have a more drastic impact on their revenues.

Hit on short-term savings

With the uncertainty around the availability of food and essential items in the market, many people will switch from savings to keeping money (cash or digital) readily available to spend at short notice. This behavior will lead to a decrease in the usage of short-term savings instruments for the near future.

Survival or not

As private investors get jittery over making any new investments, they are trying to first selectively invest any available money to protect companies in their portfolios in this hour of crisis. Hence, fintechs with weak business models that rely heavily upon investor money will fizzle but the ones with solid though smaller revenue models, especially the bootstrapped ones will have a good chance to come to the fore, provided they have or can build their runways for the next 6-12 months at least.

What can be done to help the fintech ecosystem?

In these times when the future of business is uncertain and survival of fintechs—especially startup fintechs—is doubtful, the government can play a pivotal role in supporting them. How? For instance, the central and state governments can give tax breaks, tax holidays, or other incentives to the banks and financial institutions who utilize the technology strengths of fintech startups in digitalizing their processes—especially in the priority lending sector. As discussed earlier, many NBFCs and MFIs still have either manual processes or rely on archaic technologies. They have never prioritized upgrading to more automated software systems. Yet now is the perfect time to help them do it as they look at ways to grow their businesses with a minimal workforce.

The blog was first published on News 18 Tech and then picked up by Yahoo news.

The role of DFS agents during the Covid-19 crisis

We have all seen, with mounting horror, the health and economic impacts of the Covid-19 crisis as they have unfolded globally over the past months. Unlike any crisis before, we face a challenge in that traditional humanitarian responses may not work. This crisis is unique in affecting large parts of the world at the same time, and responders who would usually be organizing ground-based efforts to specific locations and populations are themselves in lockdown, and often stunned by the scope and scale of the needs to be addressed.

We are having to work out, in a very short amount of time, how we offer humanitarian relief and solutions to these problems, and how we do this from a distance. Most are turning to digital platforms such as DFS (digital financial services) as the answer. Many donor organizations are immediately looking to replicate reactions from elsewhere in the world by organizing massive G2P (government-to-person) payment programs to alleviate missing incomes and are looking to use DFS and mobile money to execute them.

We are having to work out, in a very short amount of time, how we offer humanitarian relief and solutions to these problems, and how we do this from a distance. Most are turning to digital platforms such as DFS (digital financial services) as the answer. Many donor organizations are immediately looking to replicate reactions from elsewhere in the world by organizing massive G2P (government-to-person) payment programs to alleviate missing incomes and are looking to use DFS and mobile money to execute them.

At MSC and Caribou Data we wanted to see how we could contribute to making these programs more successful, and we asked ourselves how we can, also from a distance, use our experience and platforms to understand what the situation for mobile money and banking agents is on the ground in Kenya. We wanted to understand how they’re coping with lockdowns and curfews, social distancing and hygiene, and reduced hours of bank opening. We wanted to understand how cash flow was changing, whether liquidity was becoming an issue, and what the experience of being at the very physical frontline of a digital banking system felt like for an agent in these troubled times.

After a brief discussion, we dove directly into a research sprint, using near-live data from the Caribou Data platform and MSC’s extensive contacts within agent networks to attempt a seven day research process to understand what’s going on within these agent networks. We drew quant data from over 1,000 users in a demographically representative panel to see what real cash flows were over time, and we spoke to 20 agents, one super agent and five bank agent supervisors with a simple structured questionnaire to get a sense of the experiential issues of being on the frontline of money distribution.

Our full findings are below in this report, but in summary our findings show that:

- DFS wallet balances are volatile, with an initial cash-out spike evolving into a pattern of reduced overall transaction volume but increases in transaction size, with the net effect of a halving of average wallet balances since the crisis started.

- Agent commissions have halved, putting pressure on their own livelihoods, and increased transaction sizes are making liquidity balancing harder and harder.

- Hygiene advice is poorly communicated to agents, if at all. Without clear advice, guidance and protective equipment, agents are at risk to themselves and their customers.

- We recommend that the central role of agents as frontline workers in this crisis be recognized and supported, particularly as they will be crucial to managing cash out and liquidity as DFS social payment schemes are rolled out across large numbers of the population

Further detailed research on DFS agents’ experiences in the Covid-19 crisis is available from MSC here. We plan to investigate more areas for future research, such deep dives into gender, urban/rural differences and other countries such Ghana, South Africa and Bangladesh. We welcome other organizations support and ideas for future research topics – contact us at covid19@cariboudigital.net