Stanley is a 35-year-old trader who sells second-hand shoes in one of the largest open-air markets in Nairobi. He makes good profit during peak hours and often reinvests the amount into his business. At times when the profits drop and become irregular, Stanley often requires a line of credit to stay afloat. On average, he borrows USD 300 per month from digital lenders to replenish his stock. He repays the loans on time to avoid a reduction of his loan limit and being negatively listed.

Stanley is a 35-year-old trader who sells second-hand shoes in one of the largest open-air markets in Nairobi. He makes good profit during peak hours and often reinvests the amount into his business. At times when the profits drop and become irregular, Stanley often requires a line of credit to stay afloat. On average, he borrows USD 300 per month from digital lenders to replenish his stock. He repays the loans on time to avoid a reduction of his loan limit and being negatively listed.

Stanley is just one among the many digital borrowers who have improved their livelihoods successfully through digital credit. Seven years since digital credit emerged, almost 6 million Kenyans either have used the service or continue to use it. Yet the question remains—is the reach of digital credit wide enough to help all Kenyans who need instant credit? To answer this question, we interviewed a sample of 50 digital borrowers. We used our Market Insights for Innovation and Design (MI4ID) approach to gather insights on the use of digital credit, segment-specific behaviors, adequacy of customer protection, and product awareness.

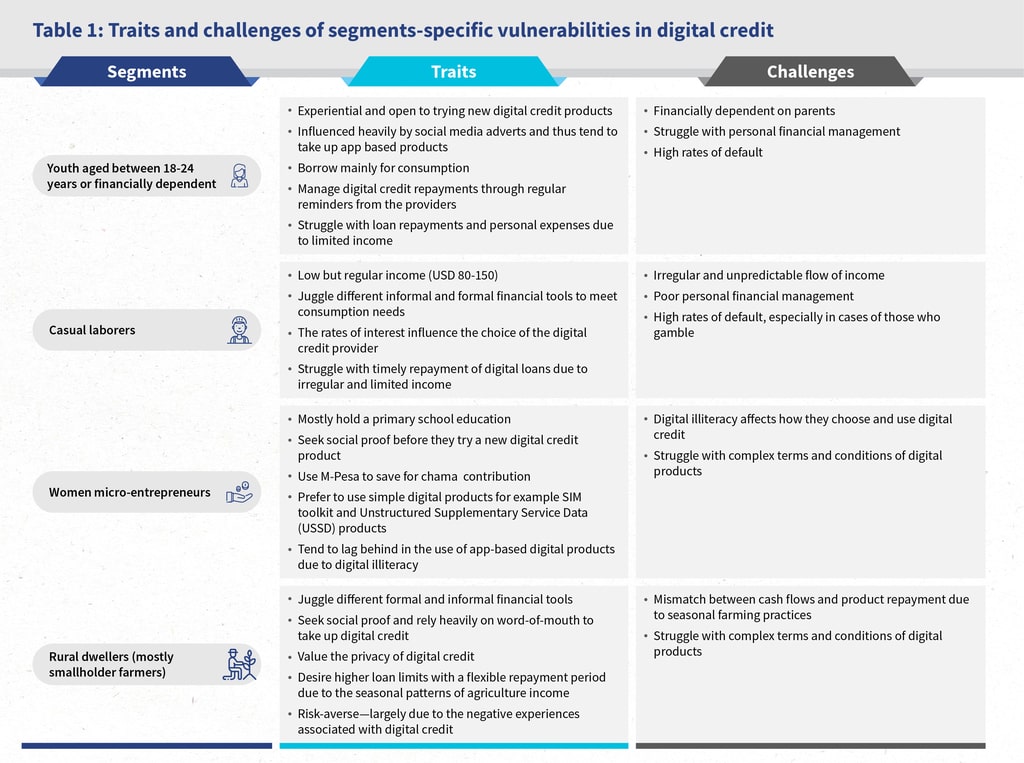

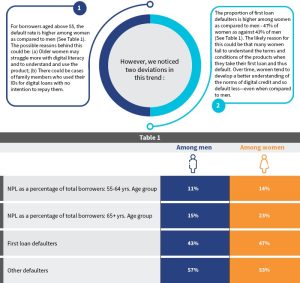

Our research focused on the neglected segments as elaborated in this report “Digital credit in Kenya: evidence from demand-side surveys”. In Table 1, we explore some of the traits and challenges of these segments that have resulted in low to moderate rates of uptake. These segments use nearly half of the total amount borrowed for consumption.

For digital credit to serve the marginalized segments, the lenders may address a few of the options, as listed below:

Appropriate product design

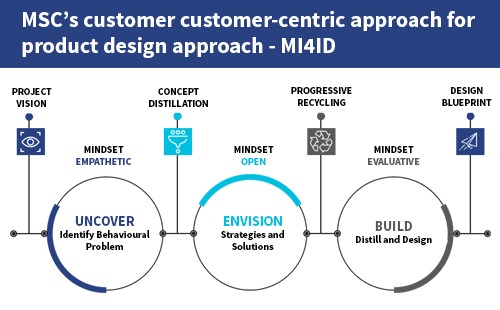

Adopt a customer-centric approach (see figure 1) to develop digital credit products that serve a majority of the segments. This would help avoid further exclusion for segments like farmers and women micro-entrepreneurs. Our MI4ID approach works on the premise that product development goes beyond the traditional process. The approach incorporates the principles of behavioral economics and human-centered design. At MSC, we believe that product development must be a two-pronged process—the generation of market insights, followed by innovation and design.

Figure 1: MSC’s customer-centric approach for product design—MI4ID

Suppliers who already operate at scale should work on more granular customer segmentation and tweak their product products and services appropriately. However, some niche players who are committed to this goal deserve better support, such as DigiFarm, Apollo Agriculture, and AfriKash

Box 1: The case of DigiFarm

In 2017, DigiFarm, an agricultural solution developed by Safaricom, partnered with FarmDrive to develop and launch a loan product. The product had flexible repayment terms that range from 30 to 120 days. As of May 2019, DigiFarm had registered over 1 million smallholder farmers on its platform who have access to digital input credit and harvest cash loans.

Use of cost-effective digital channels to communicate with the vulnerable segments

When it comes to customer engagement, specific segments, such as the rural people, do not find social media channels to be intuitive. This is because they prefer human interaction. Providers should include at least one channel that features a relatively higher “touch”. For instance, a customer care number introduces a human element that could be used for marketing and collection of loan repayments.

Product marketing as a tool to educate digital borrowers

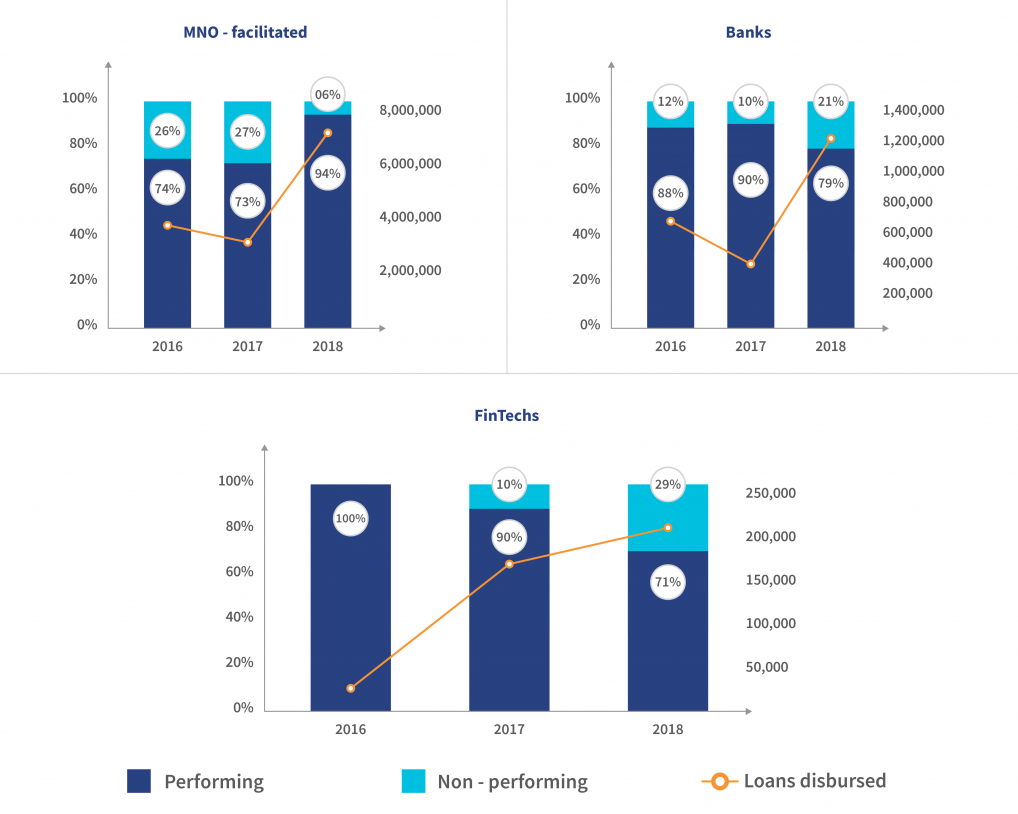

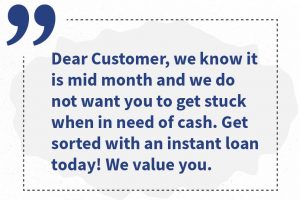

Nearly all of the digital lenders send emotive marketing messages to potential customers to persuade them to takeloans, as shown in the figure below :

However, the level of financial capacity is inadequate in some segments, such as the youth and casual laborers. They are easily influenced to take up digital loans. To encourage the responsible uptake of digital loans and higher rates of repayment, providers can introduce educational content into their product marketing strategies

Box 2: Case of Pezesha

Pezesha is a peer-to-peer digital marketplace that targets low-income borrowers in Kenya. Its customers have a data wallet that enables them to build and store their digital profile that they can use to access credit from formal lenders. Pezesha also focuses on financial education to promote and encourage responsible financial practices and credit uptake among digital borrowers. Through its solution, Patascore, the company offers financial education content that covers a variety of areas, such as savings and investment, effective debt management, ways to improve one’s credit score, and Credit Reference Bureaus (CRBs) and their role. In the event where a borrower is denied a loan, they receive tips on how to improve their scores and advice to re-apply later.

In just seven years since the advent of digital credit in Kenya, it has displayed a great potential to serve the marginalized segments. The development of more suitable products by the suppliers can prove to be a tremendous step towards the financial inclusion of these segments.

Our report based on our study of the digital credit landscape in Kenya (2019), discusses the changes in the digital credit landscape. It highlights the core challenges, emerging concerns and also goes further to formulate recommendations for both regulators and suppliers to make the delivery of digital credit more responsible and customer-centric. Read it here.

[1] Chama is a Swahili word for group savings

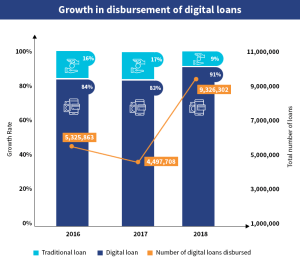

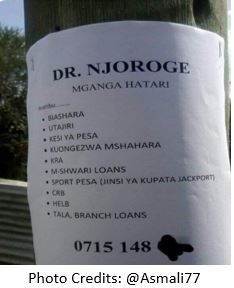

“Come and solve your problems related to M-Shwari, Branch, and Tala loans,” reads an advert from a local native doctor. These days, such adverts are a common sight across downtown Nairobi. While most Kenyans react to such “miracle cures” with disbelief, the prevalence of such posters is a reaction to the real struggle that Kenyan digital borrowers continue to face. A typical Kenyan digital borrower juggles three loans and struggles to repay on time, despite the fact that these are relatively small loans.

“Come and solve your problems related to M-Shwari, Branch, and Tala loans,” reads an advert from a local native doctor. These days, such adverts are a common sight across downtown Nairobi. While most Kenyans react to such “miracle cures” with disbelief, the prevalence of such posters is a reaction to the real struggle that Kenyan digital borrowers continue to face. A typical Kenyan digital borrower juggles three loans and struggles to repay on time, despite the fact that these are relatively small loans.