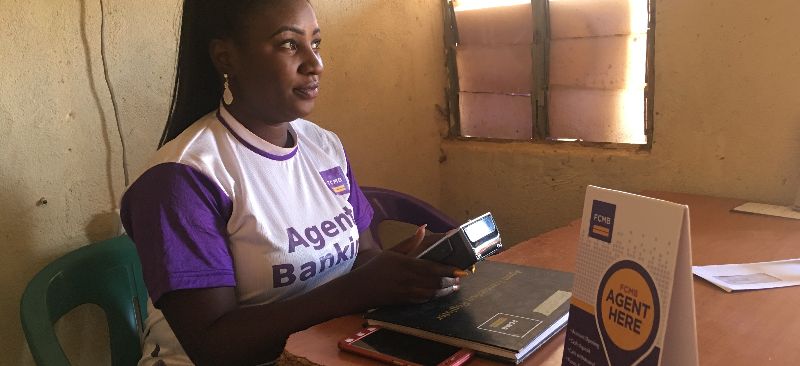

In the India Focus Note 102 we highlighted some of the challenges associated with pursuing a “bank managed/supervised” approach to agent networks in the business correspondent model. In this Note, we explore how banks can potentially address some of these challenges. This is discussed by looking at different aspects of the way a bank must manage its agent network and is completed with a case study of State Bank of India which has excelled in developing its bank-managed agent network. The Note looks at: Operational integration of the agent network with bank branches Equipping branch staff to understand and play their role in agent network management Integration of technology platforms Setting up agent support systems: structure, staffing, liquidity management and technology.

Blog

Bank Managed Agent Networks – The Challenges

Building and managing an agent network independently is not an easy task for banks. The task is challenging since banks have to develop competencies and support systems required to build and manage the network, address standardisation and scalability issues, reduce dependency and workload of branch staff, balance roles and responsibilities, reduce turn around time, and train agents and staff. This paper discusses the challenges banks are likely to face in building and managing their own agent networks. These include: The speed that banks are able to scale an agent network Achieving standardisation across the network The challenges of coordination The problems of relying on busy branch staff Establishing support and monitoring systems for the agent network Building management information systems for the agent network

M-Shwari: Market Reactions and Potential Improvements

M-Shwari, launched in November 2012, it is already receiving much attention for its mobile phone based credit scoring system, and robust growth rate. MicroSave, with inputs from Grameen App Labs, conducted market research to assess customers’ perceptions of and reactions to M-Shwari. From the research, it seems that the savings feature is used by a more upmarket demographic to circumvent the limits on saving on M-PESA; while the small loan facility is accessed by lower income customers. Of all the clients interviewed, only one had been approved for a loan larger than KES 2,500 (US$ 28.74), while all wanted larger amounts, and Safaricom reports the average loan size at around KES 1,000 (US$ 11.49). There is also widespread confusion about the basis on which credit limits are decided by the system. As a result, a great deal of the much-vaunted KES 2.8 billion (US$ 32.2 million) deposited in the first three months may have been as a result of customer depositing and withdrawing to test the system and credit appraisal algorithm. Customers also have a series of specific recommendations to improve the M-Shwari product and these are also outlined in the Note.

Role of Central Bank and regulatory environment in India

Graham A.N. Wright, Group Managing Director at MicroSave talks about the changing regulatory environment for mobile money in India. He further discusses the approach banks and regulators need to take to achieve financial inclusion in its real sense — offer a range of financial services through the accounts rather than using them as mere pass through accounts for disbursement for government benefits.”

The Case for a Bank Managed Agent Network in the Business Correspondent Model

In 2011, MicroSave examined the two modes of managing agent networks-through outsourced institutional ANMs, and directly through the banks-in the India Focus Notes 76 and 77.1 We arrived at a conclusion that institutional business correspondents were perhaps better suited both from the client as well as from the bankers’ perspective. Most banks in India have also chosen to adopt the institutional business correspondent model. However, some banks have started experimenting with agent networks they directly manage and supervise. In this Note we outline the core incentives to adopt a directly managed agent network. Bank-managed models appear to:

• Help to establish trust amongst clients

• Allow better remuneration of, and thus business cases for, agents

• Meet agents’ expectations of being associated with powerful bank brands

• Have a symbiotic impact on branch business

• Diversify the risk of agent dormancy and churn (which is concentrated with 3rd party institutional network managers)

• Improve the quality of customer service at the agent outlet where they are exclusive agents.

Mobile money – Influencers of success

In this study, we attempt to examine some notable mobile money deployments across the globe.