We’ve reached an inflexion point in banking, more pronounced and more fundamental than any which has preceded. The financial technology (FinTech) revolution promises dramatic improvements in customer experience and fundamental changes in how banking is informed and how it is conducted. Financial institutions must make critical choices if they are to compete in the new digital finance world.

1. Given the pace of change financial institutions can no longer take a passive view towards the digital future. A point made by leading authors such as Chris Skinner in his book: “Digital Bank: Strategies to Launch of Become a Digital Bank”. Today, the number of fully digital banks is growing, the product range that they offer is typically limited but is evolving largely on business to consumer lines. These banks are starting to appear in Africa, after being based mainly in Asia, Europe and America. For traditional ‘brick and mortar’ banks, the question is how best to respond.

2. Foresight in a forest. It’s not easy for bankers to see what is happening, and therefore, how banks should respond; bankers in Africa have asked us – “How should we be concerned about the innovations happening in London or Europe, given our different banking and regulatory environment”. The FinTech world is vast, changing and growing rapidly, this makes it much more difficult to determine digital trends when observing a single market1, a single time-period or a single FinTech solution or type of solution. However, by comparing markets temporally and spatially, and grouping solutions, it is possible to determine tends, and through isolating these to derive insights.

3. There is a growing maturity in successful FinTechs. Two years ago, we would see FinTech ‘solutions’ pass through our offices which seemed to be looking for a problem to solve. Successful FinTechs are built around real, demonstrated customer needs that have a commercial use case, often filling a gap in the market which banks have failed to adequately address.

4. The business case of successful FinTech’s is evolving, to second generation use cases, typically these are evolutions around the core theme. Kopo Kopo, for example, in their first generation, processed payments for merchants and provided a user-friendly merchant dashboard. In later enhancements, Kopo Kopo used data gathered to offer loans to merchants based around their cash flows. After establishing a loyal merchant base Kopo Kopo rolled out QR codes. Today, Kopo Kopo offers their business operating system and intellectual property internationally.

5. Fintech’s struggle financially until they reach scale and/or multiple use cases, though investments are flowing into FinTech companies at an increasing rate – Disrupt Africa for example, reports an 84% increase in African FinTech start-ups securing funding. Nevertheless, the investments required for scaling financial technology offers opportunities for financial institutions to collaborate with FinTechs to build a unique solution for their customer base. Financial concerns can mean that some FinTechs initially opt to target customer segments where a high return can be guaranteed.

6. Beyond the fully digital banks many financial institutions are struggling with how to change. Many changes are not fundamental, but merely digitisations of the customer facing front end. However, this usually implies that aspects of the customer experience are lost, specifically turn-around time. Fast turn-around time invariably means straight through processing and digitisation of as much of the underlying process as is practical.

7. Many banks are poorly structured to exploit data. Data often exists in silos, held in legacy systems, data needs to be liberated so that it can be used. This point is clearly demonstrated when considering a FinTech’s approach to data – Fintech’s often take many more data points than banks in coming to their digital decisions – merging data from multiple sources to improve their algorithms, though sometimes they simply manage data better. Leading banks are already responding to this challenge, by combining their huge internal datasets with data derived externally, cleaning data and analysing before warehousing it for further analysis and use. The question is whether banks will be nimble enough to exploit their data archives.

8. Bank’s often fight their own internal culture. Fundamental questions exist related to whether banks have the right drive, culture, and people, to support the data driven approach to drive efficiencies and develop and improve products and services based on data.

9. Bank-Fintech collaborations are increasing. Banks frequently sponsor FinTech labs to have the first opportunity to work with or invest in FinTech, for example, in May 2017 Barclays’ opened their flagship start-up incubator at The Rise, as Europe’s largest FinTech co-working site. DBS in Singapore has established its own FinTech innovation centres. The thirteen largest European banks are investing heavily in mature FinTech. Others like Equity Bank, in Kenya collaborated with a mobile network operator to launch a mobile virtual network.

10. Managing the culture divide is the key partnership challenge. However, while partnerships are logically the next steps managing partnerships and bringing vastly different cultures together in a sustainable way is the key challenge. Attempts to bridge this cultural divide are being made by creating platforms bringing together potential partners such as the FMO’s FinTech platform for African Banks.

11. The lack of human touch creates limitations for FinTech solutions as well as opportunities. Despite growing maturity, there is a recognition that solutions designed around the absence of human touch can create limitations on the type of solution which can be successfully delivered – particularly in the context of low income, often illiterate/innumerate communities, and in FinTech lending.

12. FinTech lending has limitations which are still being resolved. FinTech solutions are excellent at disbursing credit, but they suffer when it comes to collections – they simply don’t have the physical footprint of financial institutions. This is one reason why draconian measures are taken by the FinTechs to blacklist customers who fail to pay small loans – FinTech’s offering small loans simply don’t have the mechanisms to cost effectively enforce collection. Because of this inherent limitation millions of people are potentially blocked from accessing future credit because of failing to pay a $10 loan. For these microloans much work is required to consider repayment dynamics, whitelisting mechanisms and consumer education and protection in this space. These lending limitations will become more pronounced for larger loans, particularly those outside a natural repayment structure like a value chain. In the short to medium term, this may define a collaborative space between the FinTechs and financial institutions, or will result in FinTech’s investing in collection mechanisms for larger loans, such as Funding Circle in the UK.

13. FinTechs talk of User Experience – Banks of Customer Service. FinTech’s solution is digital end to end – their point of contact with the consumer is vital, hence they ensure that the interface is very easy to use. Compared with this, financial institutions strive to deliver customer service, which is much broader in nature with the cause of the service issue often opaque. Banks may struggle to replicate FinTech user experience through their own legacy systems.

14. FinTech’s apply Agile approaches to product development. FinTechs usually apply an Agile approach to developing financial services, a core focus in this approach is to learn & fail quickly, innovate the fail again until the solution is perfect. Fintech’s often compare the Agile approach to the Waterfall methodology which is to get everything right first before testing. These approaches are derived from the software development world. In contrast conservative financial institutions pilot test products and services with more rigour, typically preferring to succeed rather than to fail fast. Certainly, financial institutions need to be nimbler in product development. But in our view, a hybrid approach which combines slightly more in depth front end market research, user based pilot testing, and agile approaches can derive products faster and better than either approach on its own. It’s worth noting that the mobile payments doyen M-PESA was pilot tested for 18 months before it was launched, and was considerably more successful that its later – supposedly agile – imitators.

15. FinTech’s exploit social media. FinTech’s are a product of the digital age, much like social media. FinTech’s exploit social media, for communications, for marketing, for data analytics and in the case of some peer-to-peer lending methodologies for determining credit limits through social media contacts. Leading banks are already embracing social media as a key communication channel.

16. Social media is set to exploit FinTech. One of the biggest banking revolutions is set to take place as and when social media/technology platforms exploit their reach to absorb FinTech services – whether this is person to person remittances by WhatsApp, Facebook Bank, Amazon or Alibaba vertically integrating from e-commerce into payments.

17. Policy changes will make it easier for many FinTech’s to compete. Policy changes including biometric identity, eKYC, and open data standards (PSB2) will make it easier for FinTech’s to sign up large numbers of customers with confidence, and in some cases using bank acquired data. There are huge systemic implications – which will flow from this, conferring significant competitive advantages to institutions able to make strategic use of data – of any type.

18. Interest in regulatory sandboxes is increasing. Regulatory sandboxes are applied in the UK and in Singapore, however, regulatory interest in sandboxes is increasing with sandboxes being discussed in Nigeria, by the BNM in Malaysia, by the Bank of Uganda and in other African countries.

19. Compliance is a FinTech’s minefield particularly when spreading across borders. Successful FinTechs can spread across borders relatively easily in the absence of well-defined regulatory environments. However, compliance standards for FinTechs are evolving and change from market to market. A FinTech operating in a low compliance market may find it very difficult to move across markets, as a result successful FinTechs such as Jumo apply the standards existing in a tough reference market. Despite these constraints it is usually much more challenging for a financial institution to move across borders given the regulatory and capital requirements around new banks. An exception to this would be rapid moves from regulators to regulate FinTech market markers to ensure they can be monitored, in areas which threaten their wider central bank roles, such as crypto-currency.

20. Collaboration within the financial sector country by country appears to be increasing. Financial institutions often struggle to collaborate especially in competitive markets. However, what can be seen is strengthening of Banker’s Associations. The re-birth of the Kenya Banker’s Association with new leadership, effective advocacy and lobbying has been well documented. The Uganda Banker’s Association has also revived, and now meets regularly with the Governor of the Central Bank to discuss issues within the financial sector. Banks are coming together to discuss the issues confronting their industry much more readily and systematically than in the past. The question will be whether they can come to any agreement on industry-wide approaches.

In conclusion, the following stands out: Consumer needs are being and can be met in ways previously unimagined, and this is being done through new digital or digitally focused institutions, whether FinTech’s or financial institutions. Given this, financial institutions must make an active choice to participate in a digital future or risk stagnation and decline. This digital future must combine the best that banking and FinTech’s can offer. Realising the opportunities represented by the digital future requires significant changes in institutional culture – and attitude towards data which will see fundamental shifts driven from an executive level. Regulating this digital future represents a similar seismic shift for Central Banks and policy makers worldwide.

1 Websites or their archives such as Irrational Innovations provide useful infographics on FinTech’s operating in different geographies.

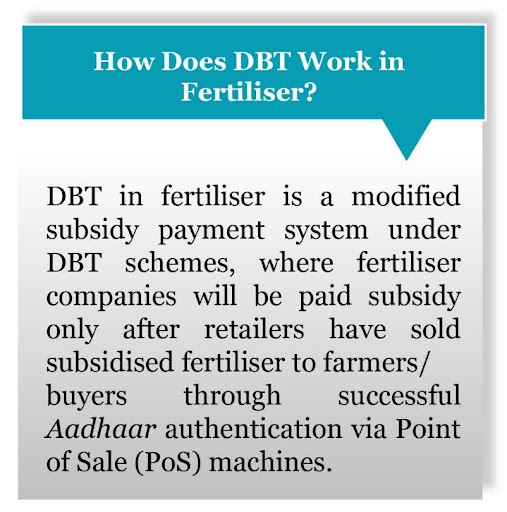

“During the last Kharif2 season, when I went to buy fertiliser, the retailer refused to sell, citing Aadhaar-based biometric authentication as a mandatory requirement for purchase. I had to go home and return the next day with my Aadhaar number (card). Yet I was unable to purchase fertiliser the following day as well because of a long queue of farmers, whose biometric authentication was taking time due to multiple attempts for authentication. I was finally able to purchase fertiliser on the third day, that too after multiple biometric authentication attempts and waiting in queue for half the day”.

“During the last Kharif2 season, when I went to buy fertiliser, the retailer refused to sell, citing Aadhaar-based biometric authentication as a mandatory requirement for purchase. I had to go home and return the next day with my Aadhaar number (card). Yet I was unable to purchase fertiliser the following day as well because of a long queue of farmers, whose biometric authentication was taking time due to multiple attempts for authentication. I was finally able to purchase fertiliser on the third day, that too after multiple biometric authentication attempts and waiting in queue for half the day”.

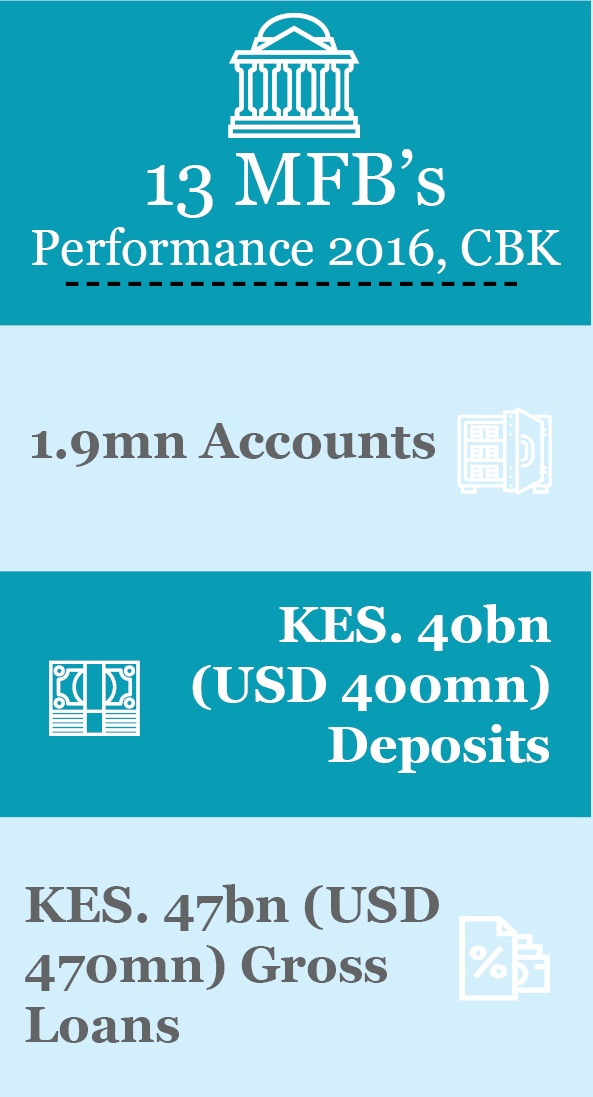

industry in Kenya. Over this period, the Central Bank of Kenya (CBK) has progressively licensed

industry in Kenya. Over this period, the Central Bank of Kenya (CBK) has progressively licensed