GSMA’s State of the Industry Report 2014 tells us there are 255 mobile money services in operation across 89 countries; digital financial services (DFS) are now available in over 60% of developing markets. An increasing number of services are reaching scale: 21 services now have more than one million active accounts, but 234 have failed to do so. So what separates these 21 “sprinters” from those deployments that limp?

There are, of course, many factors, but at the core of all the successful deployments has been a serious investment in at least three core pillars: 1. Understanding the market; 2. Technology; and 3. Building a robust & reliable agent network development.

This presentation highlights these three core design principles for successful Payment Banks and the lessons from international experience.

Weak Bank Mitr networks (with a reported annual attrition rate of 25-35%) in India could severely undermine the PMJDY and the DBT plans of the Government of India. Many Bank Mitrs have stopped offering services because of low commissions for processing G2P payments. However, the government released an Office Memorandum on 16th January 2015 setting the DBT commission rate for rural areas at 1% – much below the costs of delivering the monies and could potentially derail the entire financial inclusion effort of Government of India.

Task Force on Aadhaar-Enabled Unified Payment Infrastructure estimated that a 3.14% DBT commission would be adequate. A new MicroSave costing exercise found that the cost for processing transactions through the agent network is at least 2.63% for each transaction– much higher in more remote rural areas. Prima facie cost to the government for paying DBT commissions appears high, however it could be offset by huge potential savings from reduced administrative costs and reduced payment leakages. A 2011 McKinsey & Company analysis of India’s government payment system, estimated it to be Rs. 1 lakh crore annually (US$22.4 billion).

If the Bank Mitr network needs to be made more sustainable and ensure quality services, an adequate commission rate (MicroSave estimates this to be a minimum of 3%) for the first few years of PMJDY should be considered which can be reduced as the programme scales.

There is increasing evidence from countries such as Pakistan, Brazil, Columbia, Mexico and South Africa that the government-to-person payments offered through digital and branchless banking channels could be a stepping stone to financial inclusion. The Government of India and the Reserve Bank of India have adopted a similar path to financial inclusion in India. While the target beneficiaries and the channels used under social benefit schemes and subsidy programmes and FIP are the same, financial inclusion is not being achieved as the efforts of the stakeholders driving these are not aligned. This Note analyses the demand as well as supply side impediments to realising the potential of G2P payments to further the cause of financial inclusion in India.

Eight NBFC-MFIs received ‘in-principle’approval from RBI to set up SFBs. However, a few big NBFC MFIs missed out or did not apply for SFB license. Once transformed SFBs will enjoy better legal identity, access to public deposits and capacity to expand varied market segment. However, it may be not the end of the road for non-SFB MFIs. The transformation phase of SFBs likely to provide short to medium term advantage to non SFB MFIs. SBFs may face challenges in producing majestic growth numbers as funding under priority sector lending and managed loan portfolio will dry up gradually. This will be time for Non-SFB MFIs to strengthen operational processes and develop robust control structures to increase their competitive advantage. Non-SFB MFIs can also find ways to increase their market share, some may – Expand through strategic tie-ups, take up segments/geographies that SFBs may vacate and expanding off balance sheet portfolio. This note discus all these aspects in details.

The consolidation of multiple audit reports into an organisational level audit report is often a challenge for the audit department. This is mainly because of the large volumes of data that come from different levels and regions of the organisation. Consolidating them into a coherent report that highlights key issues and gives a comparative picture of the different operational levels requires a lot of time and effort. MFIs can overcome these challenges by using a Score-based Audit tool, which is designed using audit-checklists. This Note highlights the advantages of using the Score-based Audit tool, the types of audit tools to be used, designing a methodology and the procedure to use it.

In Indonesia, microfinance is offered by a variety of institutions, namely credit and savings cooperatives, BPRs/rural banks, venture capital firms, rural branches of commercial banks and informal village banking institutions. Despite this, only 36% of the total population above 15 years of age has access to formal financial services. This indicates that there is a huge untapped market wherein MFIs could reach out to those financially excluded from formal financial services. MFIs could do so more efficiently using the technology and, particularly, digital financial services. And this could be instrumental in increasing financial inclusion.

The microfinance sector in Indonesia continues to lag behind countries like India, Kenya and the Philippines in leveraging technology to optimise operations. The back office core banking solution or the information system used by MFIs to manage and track client-level transactions and financial accounting are often working fine, but the front end typically remains paper-based. MicroSave, which has worked with more than 30 of the leading MFIs in Indonesia, has found that very few of these MFIs used front-end technology, with the exception to update their regular repayment transactions.

Front-end technology includes the use of a hand-held device/mobile/tablet to digitise the information flow and update the records directly into the core banking solution. These devices are loaded with CRM (Customer Relationship Management) solutions — a system for managing a company’s interactions with current and future customers. It often involves using technology to organise, automate, and synchronise sales, marketing, customer service and technical support. MFIs have used CRM solutions to manage the entire customer life cycle right from acquisition to post disbursement servicing, all on a single platform. Most of the CRM solutions available in the market are built on an android operating system and are more user-friendly and intuitive for field staff such as loan officers and branch managers.

The figure below shows a few common functionalities which a financial CRM can offer to an MFI. (This is not an exhaustive list of functionalities and there could be many more such as analytics, etc., which can be offered by a financial CRM):

Financial CRM for MFIs

Lead Generation

Lead Generation

Bulk Lead Upload

Sales Management

Timely Reminder

Geo- Tagging

Lending Platform

Loan Application

Financial Analysis

Credit Bureau Check

Loan Disbursement

Loan Utilisation Check and Monitoring

Field Office Wise LUC Detail

LUC Reminders

Loan Repayment

Collection schedule and updating repayment transactions

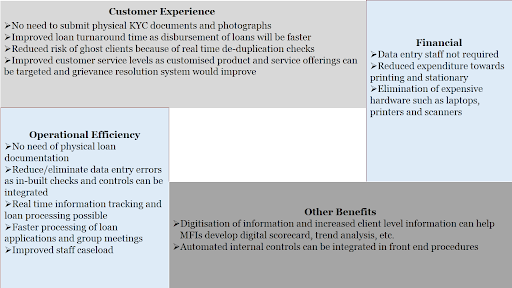

MFIs can garner the following advantages by using mobile technology:

*Above figure has been adapted from MicroSave’s DFS for MFIs Toolkit and Accion’s Case Study on Digital Field Applications

The adjacent figure shows an example of how a front-end procedure of client sourcing/loan origination will look like after adapting to mobile technology.

The benefits listed above and with the ease of processing as shown in the adjacent figure clearly demonstrate that by using mobile technology, MFIs would not only be able to streamline their operations and reduce redundant manual work flows but would also be able to increase the access to and quality of financial services.

For more details, we encourage you to watch a video of Musoni. Musoni has embraced technology in every aspect of its operations. The MFI uses M-PESA to transfer cash into the mobile wallets of customers.

While the benefits are quite evident, MFIs must carefully consider the following issues before venturing into a new technology-enabled provision of financial services:

The strategic objective of using the new technology should be clear to the management as well as all the staff of an MFI

The MFI’s existing core banking system must enable integration with the CRM module – particularly where the CRM module is supplied by a new vendor

The market environment and infrastructure (including mobile penetration and connectivity, field staff literacy levels, etc.) play a critical role in choosing the front-end technology and the user interface

The reliability of the CRM technology to not only handle the current scale of transactions but also an expected growth in the medium term

Evidently, time is ripe for MFIs in Indonesia to leverage technology and take their operations to the next level. MicroSave, with the support of MetLife Foundation, conducted a training in Indonesia on the use of DFS. The training covered a breadth of issues that will help interested MFIs to craft robust strategies in enhancing their financial services. We are keenly looking forward to working with several of them to implement these initiatives.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.