In the past five years the domain’s work has spanned a great width, right from scheme based assessment and evaluation to policy design and implementation. We believe that the most effective knowledge is shared knowledge. Therefore, GSI domain is also leveraging years of experience from India to assist countries in other geographies to better design their financial inclusion and implementation policies.

Blog

India Needs More Women Business Correspondent Agents

The 2018 budget of the Government of India has taken a number of initiatives to empower women in the country. These include increased gas connections through subsidies to 80 million women under the Pradhan Mantri Ujjwala Yojana (from the earlier 50 million) and a 37% increase in loans to women Self-Help Groups (SHGs).

The 2018 budget of the Government of India has taken a number of initiatives to empower women in the country. These include increased gas connections through subsidies to 80 million women under the Pradhan Mantri Ujjwala Yojana (from the earlier 50 million) and a 37% increase in loans to women Self-Help Groups (SHGs).

These initiatives are expected to contribute towards women’s social and economic empowerment. However, it is critical that the government strengthens its commitment to women empowerment and continues to introduce and support programmes that enable greater financial inclusion for women. The Financial Inclusion Insights Wave IV India report reveals a significant gender gap in terms of access to formal financial services. As of June, 2017, 33% of women had active bank accounts as compared to 47% of men.

The agency banking channel, which has been the backbone of financial inclusion efforts in India, is yet to succeed in serving as many women as men. As per the ANA India Wave II study1, women comprise 43% of the customer base of agents. The study highlights a vast gender imbalance in the agency banking channel with only 8% of agents being women2.

|

The Financial Inclusion Insights Wave IV India report reveals that only 6% of Indian women are advanced active account users3. This indicates that in India, women with bank accounts do not utilise them to their full potential. Women find female agents easier to approach, more trustworthy, and better at maintaining confidentiality as compared to male agents. ANA data shows that half the customers served by a woman agent are women, while two-fifths of customers that male agents serve are women. This shows that a woman agent is more likely to have women customers than a male agent. Clearly, more women agents on the ground are likely to boost the agenda of financial inclusion. |

Women Agents in India – Current Status

The ANA Wave II study finds that women agents have a mean age of 31 years. More than half have a bachelor’s or a higher degree. Predominantly, it is women agents who serve rural areas, with a presence of 71% as opposed to 54% male agents. Approximately 65% of these women agents are dedicated solely to agency banking 4 as opposed to 44% male agents. The ANA Wave II findings also reveal the following:

a) Women agents perform at par with the male agents in terms of running the business

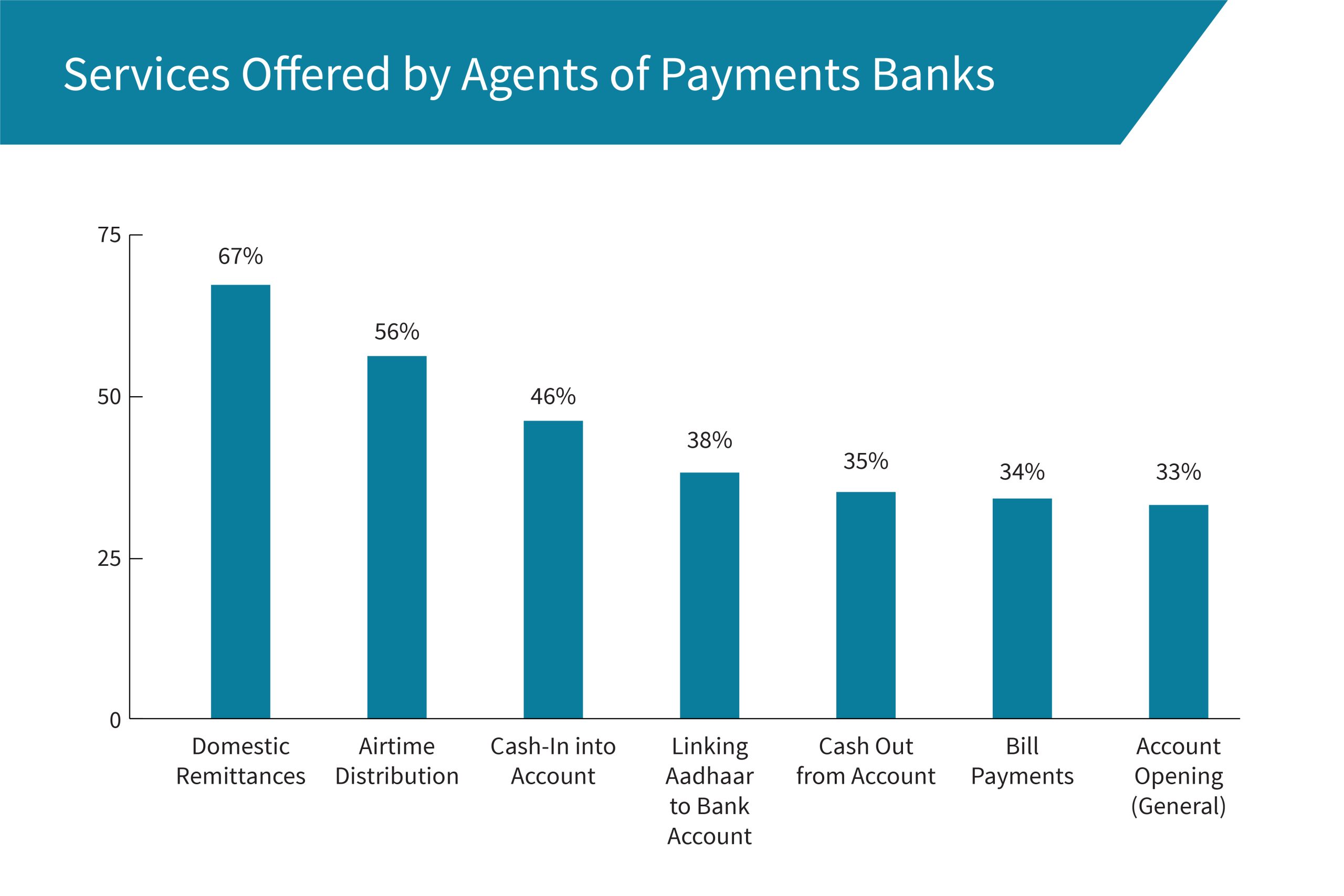

There is a myth that women are less enterprising than men. The ANA data reveals a contrary reality. The portfolio of services that women agents provide is quite exhaustive. At the country-level, the median number of services that women agents provide is seven, which is slightly more than male agents, who provide six services. The proportion of women agents who provide various services is roughly equivalent to, or greater than the services that male agents provide (see below graph). The one exception is domestic remittance, which is mainly an urban phenomenon. The presence of women agents in these areas is much lesser (metros – 4%, non-metro urban – 6%) compared to rural areas (10%).

Eighty percent of women agents provide a Government-to-Person (G2P) facilitation service, such as insurance registration, pension registration, scholarship registration, subsidy registration, and linking the Aadhaar card, among others. The range of services is much higher when compared to male agents (68%). This indicates that women agents are more likely to serve customers even if the transaction does not generate as much revenue 5.

In terms of business viability, at the country-level, women agents generate less revenue. However, they also incur less operating expenses when compared to their male counterparts. In rural areas, where almost 71% of the women agents operate, there is almost no difference in their profitability levels as opposed to male agents (see below graph).

Additionally, the proportion of women agents (33%) who incur losses or achieve break-even is actually a little lower than male agents (34%).

b) Providers do not offer similar levels of support to women agents

Women agents receive much less support from service providers. Only 8% of women agents have cash or e-money delivered to them (that is, they do not travel for it) as compared to 16% of male agents. A widowed woman agent in Kapurthala, Punjab observed, “there are training sessions that service providers conduct, but there is no such regular monitoring. I think it is important to be regularly monitored by the service providers. It is all the more important, especially for women – it makes things easier for us.”

c) Women agents face a lot more challenges

MicroSave’s research indicates that women agents find it difficult to establish a good rapport with the staff of service providers, who are mostly male. For example, women agents cited instances where they struggle to get answers to their queries from the support staff. This results in forfeiting new opportunities that may arise from new services and products. Furthermore, women agents often cite challenges in handling a difficult customer, particularly men. Women agents emphasise that previous experience of dealing with customers is a prerequisite for running a successful agency business 6.

Way forward

It is time for financial service providers and policymakers to put policies and practices in place to ensure higher participation of women in their agent workforce. Here are a few points that could potentially make it happen:

|

|

In India, more than 137 million women are still excluded from formal financial services. There is evidence that women agents handle clients more professionally and perform at par with male agents in terms of business. In fact, women agents do more transactions and are preferred by women customers. These developments together indicate a business value proposition that we simply cannot ignore.

1The State of the Agent Network India 2017 report, based on the Agent Network Accelerator (ANA) Wave II survey, is a nationally representative study of the business correspondent (BC) agent network in India.

2Agents who offer digital financial services are known as business correspondent agents in India. We have referred to business correspondent agents (BCA) as agents and women BCAs as women agents.

3 Advanced active account users: Users who use a financial account for services other than basic or P2P services. In the FII study, in the case of mobile money, airtime top-ups are not considered an advanced use.

4 Dedicated agent – An agent who solely conducts agency banking business

5 The commission income from G2P facilitation is lower than CICO charges; MicroSave analysis and review of commission structure of providers in public domain.

6 The team conducted qualitative interaction with women agents during the fieldwork for ANA India Wave II

Indian DFS landscape is changing: Insights from State of the Agent Network India, 2017 (ANA) Wave II Research

MicroSave recently published its ‘State of the Agent Network, India 2017’ report based on our Agent Network Accelerator (ANA) Wave II research. We conducted the research in 2017, based on a nationally representative sample of 3,048 business correspondent agents. The 2017 India report proposes a significant shift from Wave I in 2015.The report focuses on the operational determinants of success in agent networks. It provides insights on agent network structure and key performance metrics, such as agent viability, quality of provider-support, and compliance and risks related to providers. The report presents changes that have happened over two years, from 2015 (when we had conducted Wave I of the research) to 2017. This blog highlights the ‘change story’ from 2015 to 2017.During this period, a number of changes have happened. New types of financial institutions, such as payments banks have emerged, support systems have improved, while product matrices have widened. Also, agent networks have managed to successfully position themselves as delivery channels for various financial and non-financial services.

Over the past few years, the story of financial inclusion in India has shifted from account opening to account usage. This change has received support from various policy moves by the government, an interoperable payments system, and the ubiquity of Aadhaar. This makes India stand out as a successful example of policy imperatives driving the agenda of financial inclusion. The following section presents key findings from ANA Wave II research including changes from the Wave I study.

1. Banking Services and Government-to-Person (G2P) Facilitation Services have Encouraged Account Usage

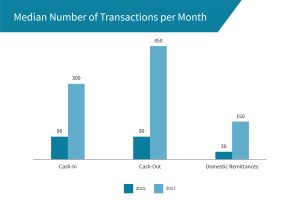

ANA research findings suggest that an increasing use of agent points for Cash-In and Cash-Out (CICO) transactions and remittances have led to increased transactions and subsequently, higher revenues and profits for agents. The graph below presents the median number of cash-in and cash-out transactions, as well as remittances in 2015 and 2017. During this time, cash-in transactions have grown more than three times, while cash-out and domestic remittances have grown five times. The growth in transactions, together with G2P facilitation services, have led to a robust use-case for agents across India. This has, in 2017, translated into higher monthly median revenues and profits, which doubled from their 2015 figures (USD 40 to USD 93 and USD 16 to USD 31, respectively).

ANA research findings suggest that an increasing use of agent points for Cash-In and Cash-Out (CICO) transactions and remittances have led to increased transactions and subsequently, higher revenues and profits for agents. The graph below presents the median number of cash-in and cash-out transactions, as well as remittances in 2015 and 2017. During this time, cash-in transactions have grown more than three times, while cash-out and domestic remittances have grown five times. The growth in transactions, together with G2P facilitation services, have led to a robust use-case for agents across India. This has, in 2017, translated into higher monthly median revenues and profits, which doubled from their 2015 figures (USD 40 to USD 93 and USD 16 to USD 31, respectively).

2. Interoperability of Payment Infrastructure and Licensing of Payments Banks have begun to Reshape the Market.

India has embraced full system interoperability, which has enabled banks and mobile financial service operators to connect to a common platform or switch, thereby facilitating transactions. ANA findings suggest that almost two-thirds of agents conduct interoperable transactions. This trend is similar across locations, be it metro, non-metro, or rural. Approximately 70% of interoperable agents offer cash-in services, while approximately 60% offer cash-out and remittances for other banks. This also explains the reduction in the number of non-exclusive agents in India. Agents are no longer required to be associated with multiple providers to be able to serve more customers. It is widely established that interoperability offers significant benefits for the wider ecosystem. These benefits include wider adoption, higher transaction volumes, and greater velocity of money in the ecosystem.

India has embraced full system interoperability, which has enabled banks and mobile financial service operators to connect to a common platform or switch, thereby facilitating transactions. ANA findings suggest that almost two-thirds of agents conduct interoperable transactions. This trend is similar across locations, be it metro, non-metro, or rural. Approximately 70% of interoperable agents offer cash-in services, while approximately 60% offer cash-out and remittances for other banks. This also explains the reduction in the number of non-exclusive agents in India. Agents are no longer required to be associated with multiple providers to be able to serve more customers. It is widely established that interoperability offers significant benefits for the wider ecosystem. These benefits include wider adoption, higher transaction volumes, and greater velocity of money in the ecosystem.

In 2015, the Reserve Bank of India (RBI) gave “in-principle” approvals to 11 payments banks. These payment banks are able to provide all banking services with the exception of credit. New to the financial system landscape, payments banks are beginning to show their presence. However, they have some distance to travel. Agents of payments banks presently conduct a median of nine transactions compared to 33 conducted by agents of other banks. Payments bank agents earn median monthly revenues of USD 54 as compared to USD 93 earned by agents of other banks at the country-level.

3. Support systems have improved

Providers in India have institutionalised the agent induction process by providing training to agents in the first three months, followed by refresher training. There has been a significant rise in the proportion of agents that received induction and refresher training in 2017 (77% and 87% respectively) as compared to 2015 (59% and 61% respectively). From our earlier assessments, we know that trained agents are able to perform better, are more compliant, and extend better customer service. Evidence from ANA India Wave II further supports this hypothesis. Our findings indicate that trained agents conducted almost 10% more transactions on a daily basis than untrained agents.

Providers in India have institutionalised the agent induction process by providing training to agents in the first three months, followed by refresher training. There has been a significant rise in the proportion of agents that received induction and refresher training in 2017 (77% and 87% respectively) as compared to 2015 (59% and 61% respectively). From our earlier assessments, we know that trained agents are able to perform better, are more compliant, and extend better customer service. Evidence from ANA India Wave II further supports this hypothesis. Our findings indicate that trained agents conducted almost 10% more transactions on a daily basis than untrained agents.

However, regular monitoring by providers has seen a dip. With increasing transaction volumes at the agent points, providers need to ensure that monitoring remains a top priority. The findings of the ANA Wave II suggest that agents that were monitored regularly conducted four more transactions per day than those not monitored regularly. Anecdotal evidence further suggests that regular monitoring of agents builds the trust of agents in the provider.

4. Instances of money loss (fraud) have increased

Instances of agents experiencing incidences of money loss (fraud) have increased from 2% in 2015 to 22% in 2017. New compliance concerns have also emerged from the ANA Wave II study. Among agents, 35% reported assisting customers by entering transaction PIN or password on their behalf. Moreover, 24% of agents reported that they provide handwritten slips as proof of transaction to customers as opposed to printed receipts. Providers therefore need to incorporate fraud typology and mitigation measures into training modules for agents.

Driven by ever-changing global standards for delivery of financial services, regulators have been updating regulations and enforcing existing rules. In 2015, the Reserve Bank of India (RBI) issued a ‘Master Circular on Frauds – Classification and Reporting’. The circular has placed the primary responsibility for fraud prevention on banks. Providers in India have been upgrading their systems and incorporating recent technological advancements, such as cloud-based systems and adopted SMS or IVR-based payments to prevent instances of fraud.

Agent networks in India have proven to be not only resilient but unique. This can be attributed to policy initiatives, such as interoperable payments systems and market dynamics. While the sector has made positive strides and appears to be stabilising, risk and challenges remain. Provider must therefore address increasing incidence of fraud and compliance issues related to interoperability immediately.

To ensure agent viability, either a more efficient distribution strategy or product matrix or both would be required. Meanwhile, a few issues needs to be understood. Why is it that operating costs at agent points are the highest in India? Does it have anything to do with the multiple front-ends required for acceptance of card and Aadhaar-based transactions? Consequently, agent profitability remains a key concern in India. Agents have not yet managed to get to sustainable levels of profitability. Moreover, the likelihood of agent dormancy and dropout remain high.

In this regard, differentiated agent outlets, as advocated by MicroSave could be a potential solution to address issues of agent profitability. While sales agents would manage higher value transactions and sales of sophisticated products, service agents would do basic, everyday transactions, without requiring any sophisticated backend infrastructure.

Assessment of Direct Benefit Transfer in Fertiliser

This study captures the research findings from the assessment of DBT in Fertilizer for the Government of India across 14 pilot districts across 11 states.

Triple Burden of Malnutrition in India – Are We Doing Enough?

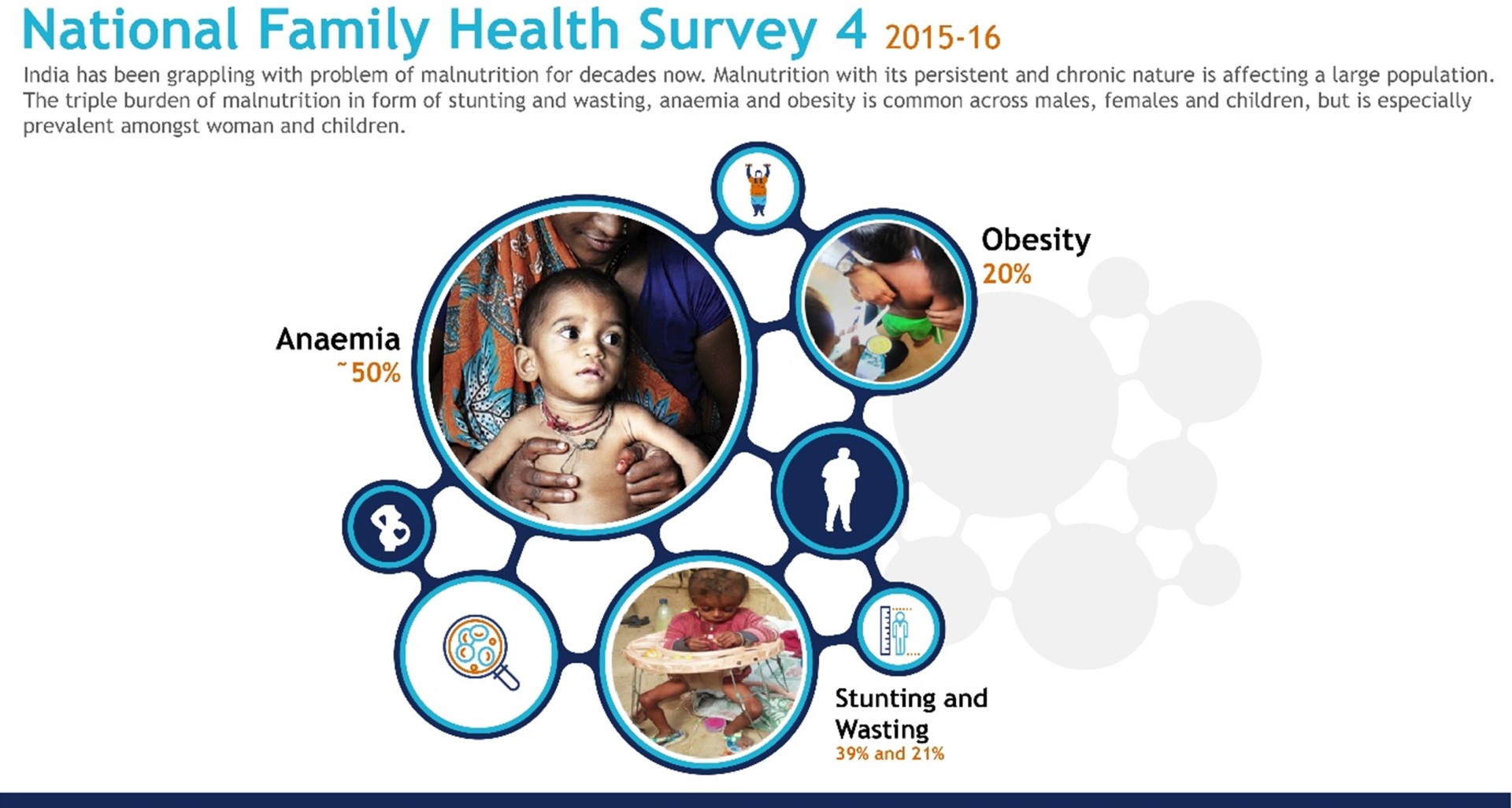

India has been grappling with the problem of malnutrition for decades now. With its persistent and chronic nature, malnutrition affects a large proportion of the population in the country. The triple burden of malnutrition in the form of stunting and wasting, anaemia, and obesity are common across women, men, and children, but is especially prevalent among women and children.

The level of public investment in the Union Budget for the financial year 2018–19 in form of subsidy on food and nutrition security has been substantial, at INR 1700 Billion (USD 25 billion). The enactment of National Food Security Act of 2013 institutionalised the importance of food and nutrition. However, the nutritional status of India’s population still remains compromised and has been a persistent problem despite measures taken by the centre and state governments. The country has witnessed significant economic growth, but its performance on nutritional indicators and hunger levels remain alarmingly poor. India ranked 100 among 119 developing countries in the Global Hunger Index of 2017. A complex range of barriers like culture, food habits, income and gender inequality, and social exclusion continue to thwart efforts to address the scourge of malnutrition.

The Government of India has rolled out a number of schemes in the past to combat this public health concern. These include Integrated Child Development Services (ICDS), National Health Mission, Janani Suraksha Yojana, Maternity Benefit scheme, Mid-Day Meal Scheme and National Nutrition Mission. However, the results have been poor. The experience from the implementation of these schemes suggests that on-ground footprint and effective community engagement are vital to address malnutrition. Further, there is a great need to design such public interventions keeping the community in focus.

Global evidence suggests a shift from a strategy of Information, Education, and Communication (IEC) to Social Behaviour Change Communication (SBCC). This is because society and its culture have a deep impact on the habits and lifestyles of potential beneficiaries. A standardised approach to tackle malnutrition at the national level is not feasible given the social, cultural, economic, and geographic diversity in the country.

There is global evidence that suggests that having field functionaries or health workers from the community has a long-lasting impact on the behaviour of the target population. There has been a surge in the activity of these workers after the Alma Ata Declaration of 1978, which sought to address the shortages of professional healthcare workers to serve the last mile.

One plausible strategy, therefore, might be to appoint community-based catalysts for change – or voluntary field functionaries. These functionaries would understand the needs and culture of the society. They could help improve the implementation of public health interventions by serving as a link between the government and beneficiaries. Health and nutrition are dependent a wide range of variables that include culture, socio-economic status, equity, access to services and information, etc. Trained functionaries on the ground at the hamlet- or village-level would help assess and understand these complex, “softer” issues and their interplay with health and nutrition and impact on it. The functionaries would also be able to devise ways to address the issues at the local level within the constraints of the resource pool provided.

India already has its share of experiences with community workers in the form of Anganwadi workers (AWW) and Accredited Social Health Activists (ASHA) under the Ministry of Women and Child Development (M/o WCD) and the Ministry of Health and Family Welfare (M/o HFW) respectively. AWW and ASHA have been entrusted to provide adequate healthcare to rural people and educate them on issues of preventive and promotional health care. However, their performance has been below expectations for a number of reasons. These relate to issues in the selection process, lack of clarity of roles, low capacities and skill-sets, excessive workload, weak supervision, low incentives, and lack of job security.

There is a need to work more closely with the community to address malnutrition. There is a need to work at the household- or hamlet-level to build their capacities to enable them to take control of their health. Volunteers from the community, especially women could spearhead movements, such as Jan Andolan1 to transform India from ‘Kuposhit Bharat2 ’ to ‘Suposhit Bharat3 ’.

Whereas ASHA and Anganwadi workers must serve a relatively large population (that is, around 200–400 families), the proposed new field functionary will be working at the hamlet-level with 10–15 families. They will have precisely defined roles and responsibilities. This will allow a more focused approach to address the complex web of issues around health and nutrition. The recently launched National Nutrition Mission may provide a conducive platform for building additional manpower at the hamlet level.

However, we cannot consider such an initiative as a solution to solve all the problems. India has suffered from the problem of weak implementation since several decades. The success of such a programme would depend largely on the following imperatives:

- Careful selection, training and accreditation (wherever applicable) of the volunteer workers at the grassroots;

- Convergence and linkages among various government departments for better outcomes of the public health programmes;

- Active monitoring of manpower in the public health domain;

- Supportive supervision for the field functionaries;

- Provisioning of an adequate compensation structure and timely payment;

- Meticulously planned job responsibility and performance indicators for the functionaries.

[1] Mass movement

[2] Malnourished India

[3] Well-nourished India

National Family Health Survey

India has been grappling with the problem of malnutrition for decades now. With its persistent and chronic nature, malnutrition affects a large proportion of the population in the country. The triple burden of malnutrition in the form of stunting and wasting, anaemia, and obesity are common across women, men, and children, but is especially prevalent among women and children.

The level of public investment in the Union Budget for the financial year 2018–19 in form of subsidy on food and nutrition security has been substantial, at INR 1700 Billion (USD 25 billion). The enactment of National Food Security Act of 2013 institutionalised the importance of food and nutrition. However, the nutritional status of India’s population still remains compromised and has been a persistent problem despite measures taken by the centre and state governments. The country has witnessed significant economic growth, but its performance on nutritional indicators and hunger levels remain alarmingly poor. India ranked 100 among 119 developing countries in the Global Hunger Index of 2017. A complex range of barriers like culture, food habits, income and gender inequality, and social exclusion continue to thwart efforts to address the scourge of malnutrition.

The Government of India has rolled out a number of schemes in the past to combat this public health concern. These include Integrated Child Development Services (ICDS), National Health Mission, Janani Suraksha Yojana, Maternity Benefit scheme, Mid-Day Meal Scheme and National Nutrition Mission. However, the results have been poor. The experience from the implementation of these schemes suggests that on-ground footprint and effective community engagement are vital to address malnutrition. Further, there is a great need to design such public interventions keeping the community in focus.

Global evidence suggests a shift from a strategy of Information, Education, and Communication (IEC) to Social Behaviour Change Communication (SBCC). This is because society and its culture have a deep impact on the habits and lifestyles of potential beneficiaries. A standardised approach to tackle malnutrition at the national level is not feasible given the social, cultural, economic, and geographic diversity in the country.

There is global evidence that suggests that having field functionaries or health workers from the community has a long-lasting impact on the behaviour of the target population. There has been a surge in the activity of these workers after the Alma Ata Declaration of 1978, which sought to address the shortages of professional healthcare workers to serve the last mile.

One plausible strategy, therefore, might be to appoint community-based catalysts for change – or voluntary field functionaries. These functionaries would understand the needs and culture of the society. They could help improve the implementation of public health interventions by serving as a link between the government and beneficiaries. Health and nutrition are dependent a wide range of variables that include culture, socio-economic status, equity, access to services and information, etc. Trained functionaries on the ground at the hamlet- or village-level would help assess and understand these complex, “softer” issues and their interplay with health and nutrition and impact on it. The functionaries would also be able to devise ways to address the issues at the local level within the constraints of the resource pool provided.

India already has its share of experiences with community workers in the form of Anganwadi workers (AWW) and Accredited Social Health Activists (ASHA) under the Ministry of Women and Child Development (M/o WCD) and the Ministry of Health and Family Welfare (M/o HFW) respectively. AWW and ASHA have been entrusted to provide adequate healthcare to rural people and educate them on issues of preventive and promotional health care. However, their performance has been below expectations for a number of reasons. These relate to issues in the selection process, lack of clarity of roles, low capacities and skill-sets, excessive workload, weak supervision, low incentives, and lack of job security.

There is a need to work more closely with the community to address malnutrition. There is a need to work at the household- or hamlet-level to build their capacities to enable them to take control of their health. Volunteers from the community, especially women could spearhead movements, such as Jan Andolan1 to transform India from ‘Kuposhit Bharat2 ’ to ‘Suposhit Bharat3 ’.

Whereas ASHA and Anganwadi workers must serve a relatively large population (that is, around 200–400 families), the proposed new field functionary will be working at the hamlet-level with 10–15 families. They will have precisely defined roles and responsibilities. This will allow a more focused approach to address the complex web of issues around health and nutrition. The recently launched National Nutrition Mission may provide a conducive platform for building additional manpower at the hamlet level.

However, we cannot consider such an initiative as a solution to solve all the problems. India has suffered from the problem of weak implementation since several decades. The success of such a programme would depend largely on the following imperatives:

- Careful selection, training and accreditation (wherever applicable) of the volunteer workers at the grassroots;

- Convergence and linkages among various government departments for better outcomes of the public health programmes;

- Active monitoring of manpower in the public health domain;

- Supportive supervision for the field functionaries;

- Provisioning of an adequate compensation structure and timely payment;

- Meticulously planned job responsibility and performance indicators for the functionaries.

[1] Mass movement

[2] Malnourished India

[3] Well-nourished India