Based on successful roll-out of subsidy transfers for cooking gas, directly into the bank accounts of beneficiaries, the Government of India in September 2015 announced Direct Benefit Transfer (DBT) for PDS beneficiaries. We conducted assessments in August 2015, just before disbursement of the first tranche of cash transfers in lieu of subsidised food grains. This Note pertains to the findings of the baseline assessment. Despite many challenges, the situation was conducive for a pilot for DBT in lieu of food grains in Chandigarh and Puducherry. However, given the market infrastructure in Dadra and Nagar Haveli, it was best that the pilot was dropped; DNH lacks an alternative market and needs subsidised food grains through FPS. There are also other fundamental challenges to DBT in PDS. One of the most fundamental is the amount of money paid to beneficiaries in lieu of food grains. At present, PDS entitles low-income families to get wheat at Rs. 2 per kg, rice at Rs. 3 per kg and coarse grains such as bajra/ragi at Rs. 1 per kg. As against this, the government has fixed the DBT amount at 1.25 times the minimum support price (MSP), which is, in essence, the price at which the government procures food grains from farmers. Recipients are not happy with the amount of money received as DBT under PDS.

Blog

Real and Perceived Risk in Indian Digital Financial Services

The risks associated with digital financial services (DFS) are varied and a growing area of attention and assessment. At the same time, digital payments and broader digital financial services introduce added complexity, with new participants constantly entering the market, new products regularly introduced, and value-chain dynamics in constant flux.

In MicroSave’s recent research for the Omidyar Network, we covered all types of risks that customers and agents face. It is important to note that fraud is just one facet of risk. There is a growing body of literature on risks in DFS, and these concepts are largely related to customer protection issues. From a customer protection perspective, both Alliance for Financial Inclusion and SMART Campaign have defined risks and vulnerabilities in DFS.

Our research also explored risks from customer protection perspective. This involved going a step further than just listing risks that agents and customers face, and analysing the medium to long-term impact on the uptake and usage of DFS.

Our research also explored risks from customer protection perspective. This involved going a step further than just listing risks that agents and customers face, and analysing the medium to long-term impact on the uptake and usage of DFS.

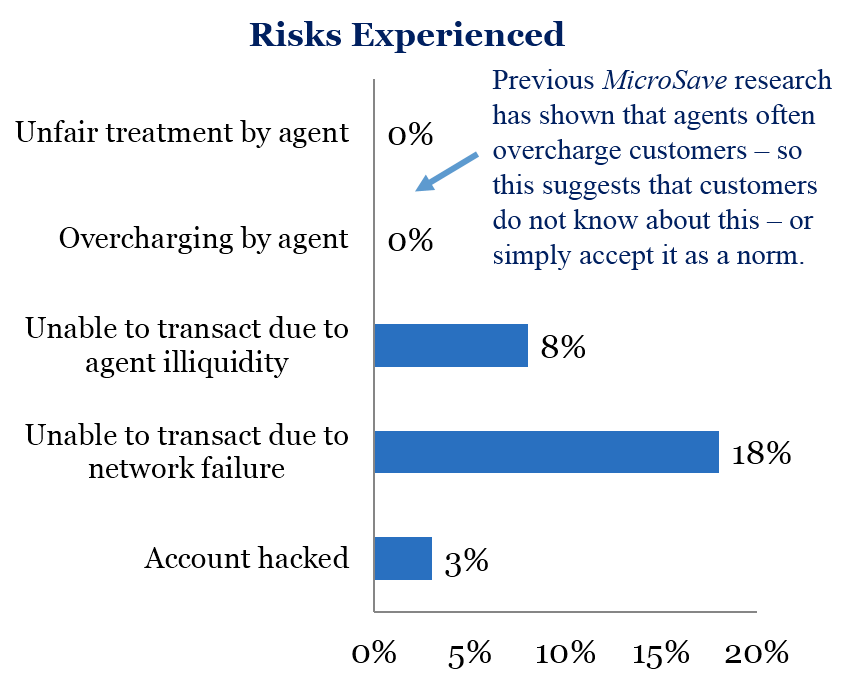

The risks and their ranking by customers (see graph) are not very different from the 16-country study conducted by CGAP. However, another risk that features prominently in India is ‘transaction data security’ or privacy of client account information. This mainly relates to agent-assisted transactions.

Most of the issues in India are operational in nature. Our qualitative research also shows that most significant risks perceived by the customers related to issues like network downtime, system and technology risks, agent unavailability, and agents lacking liquidity.

However, even these operational issues can have serious implications. Frequent service denial, incomplete and interrupted transactions, inaccessible funds, etc., leading to delay or loss of opportunity ― all negatively impact customers’ trust in DFS.

Agents face similar risks. Their key concern is also related to systems/technology and network downtime/outages while trying to serve their clients. We also explored four different types of risks individually in the research. These were:

- Account being hacked/compromised,

- Inability to transact due to network failure,

- Inability to transact due to agent liquidity issues, and

- Overcharging by the agent.

While (most) customers have not actually experienced these risks, the perception of risk has an effect on the usage and uptake of DFS.

Under the ‘Fraud Framework’, described in MicroSave’s ‘Fraud in Mobile Financial Services’ paper, India would still be classified under the “customer acquisition” stage.

This phase in India is led by government schemes like PMJDY and G2P payments. As a result, most risks rank low in terms of their occurrence. However, as the markets evolve and move to the “value addition” stage, different types of risks will evolve.

On the agent side, it is clear that poor commission is key ― both a bottleneck to growth and a driver of fraud. Field observations reveal that to maximise commissions, agents may commit fraud, or what agents call ‘workarounds’. Some frauds which often go unnoticed are

On the agent side, it is clear that poor commission is key ― both a bottleneck to growth and a driver of fraud. Field observations reveal that to maximise commissions, agents may commit fraud, or what agents call ‘workarounds’. Some frauds which often go unnoticed are

- Agents conducting round-tripping (cashing in and cashing out the same amount) transactions to earn higher commission;

- Splitting single big ticket transactions into multiple small transactions – again to maximise commission; and

- Agents overcharging customers to maximise earnings.

In response, financial service providers and agent network managers will need to:

- Contextualise risk management frameworks to the Indian context and according to the state of the evolution of the market

- Integrate this risk management framework into their operations and train agents accordingly

- Develop indicators for monitoring risks

- Regularly monitor risks and

- Develop risk-mitigation strategies

As part of this, providers and agent network managers will need to:

- Address the “hygiene factors” of system and agent reliability – see Solving Customer Service Issues in Digital Finance – Can Do, Must Do;

- Implement a comprehensive and formalised system of monitoring (something that has been largely absent to date – see Training, Monitoring & Support – Necessary, or An Opportunity To Cut Costs?

- Monitor agent performance, develop a system for warnings, censure and penal action, including termination; and

- Establish and enforce minimum disclosure and transparency requirements for product features, pricing, and terms of use.

Emergence of Mobile Insurance Models

More than 262 million people are insured by micro-insurance policies across the globe. Of these, 166 micro-insurance programmes have been identified to reach scale (i.e., more than 500,000 clients/policies in Africa, and greater than 1 mn in Asia and Latin America). However, none of these programmes match the scale and/or the pace achieved through the mobile insurance models in recent years.

The elation over mobile insurance is great, and it has crossed the first milestone of outreach. However, to make it the next ‘Uber’ of insurance, one has to look through

whether the design is aligned to the business objectives

whether the value chain is well incentivised and managed to sustain the product/s

whether the product (loyalty or paid) is able to provide business value to the insurer and/or all the value chain members, and

whether clients are adequately protected (consumer protection issues) in mobile insurance.

Over the Counter (OTC) Money Transfer in India: Mapping the Customer Experience (CX)

In our previous blog, OTC Money Transfer in India: The Remittance Silver Bullet for Migrants, we explained how OTC remittances work in India, and described the typical transactional processes. In this blog, we map the customer’s experience (CX) while conducting OTC transactions. To understand the real experience of customers, MicroSavestaff posed as customers, visited agent outlets, and conducted OTC transactions using a mystery shopping tool. As explained in the previous blog, almost all transactions are P2B (person to bank); hence, mystery shopping was conducted only at origin point of remittances (in Delhi and Mumbai). While doing so, we selected different sets of agents on the basis of following indicators:

- Marketing collateral, so as to cover agents working for different providers

- High and low customer footfall; and

- Working hours ― peak and off-peak hours.

This segmentation during mystery shopping helped us to experience varied customer service at different agent outlets, and thus map out commonalities in a typical OTC remittance transaction.

The Customer Experience Map

This map is a detailed representation of CX while using OTC services for conducting remittances. As visually represented, the overall journey of a customer using OTC services can be clearly segregated into four phases:

a. Enquiry Phase

a. Enquiry Phase

The enquiry phase is mostly triggered by the inherent NEED of the customer to remit funds back home (for family). Most customers who use OTC services have almost invariably used other formal or informal mechanisms of remittances, such as direct deposits (to beneficiary’s bank account) at a bank branch, money order services offered by post office, hawala, and courier services, among others. These customers evaluate these alternatives before using OTC services using mental models/heuristics.

First-time users of OTC services are largely influenced by colleagues or relatives who have used the services before. These social groups act as key sources of information, especially for trial/first-time transactions. Customers primarily gather key information, such as agent location, charges, and ease/process of the transaction, before opting for such services. Thus, potential customers are indecisive and compare various alternatives for remitting funds at this stage.

Most providers have not adequately explored below-the-line (BTL) activities to communicate their service offerings to potential customers. They, instead, tend to rely on social proof, in the form of recommendations of friends and family who have used the service, as a mechanism for acquiring new customers. In the absence of BTL activities, awareness about OTC services is limited to a few users, who, in turn, are not able to influence potential users outside their social circles. Providers could benefit from enhanced BTL activities, as they are likely to scale-up the use of OTC services, given the direct correlation between awareness and trial. A larger number of customers using the service will also lead to more word-of-mouth marketing among customers satisfied with the service.

b. Trial Phase

Based on information gathered during the enquiry phase, customers graduate to a trial phase. It is during this phase that the customers transact for the first time. In most cases, the trial transaction is small – of around Rs.500―1,000 (US$7―15) ― as compared to regular fund transfer of Rs. 5,000―10,000 (US$70―1,500). This is done to understand the process, and develop trust, both in the agent and in the OTC channel. The agent outlet chosen to conduct the trial transaction is generally identified by referrals made by personal influencers and/or by collaterals displayed outside agent outlets. It is important to note that, initially, the choice of an agent outlet may be driven by socio-cultural factors, such as community and place of origin. However, customers soon start assessing various service aspects. During this phase, customers give much importance to the timeliness of the transaction process and service delivery (till completion of the transaction), as well as mandatory beneficiary details (these may include bank account number, IFSC code, branch name and address) and other documentation required.

This phase is critical for converting the trial customer into a long-term repeat customer. Not surprisingly, these customers, who are focused on the transactional aspect of remitting funds, are indifferent towards the underlying service providers. The agent, therefore, is the key actor, and plays a pivotal role in building positive experiences for customers, and facilitating their transition to the next phase, i.e., the transaction phase.

c. Transaction Phase

Even though there are typically many OTC providers at the sending end, most customers prefer transacting at specific agent outlets. This preference is an outcome of operational aspects such as reasonable customer charges (insofar as it is possible to assess this with the limited information available in the market), provision of receipts, success of previous transactions, and agent support, in case of any issue. Customers, in this phase, learn to trust and eventually rely on the channel, and are confident while using OTC services to remit funds.

As most agents register customers and open their wallets without the latter’s knowledge or consent, agents maintain customers’ records at the time of registration. When customers return, agents save considerable amounts of time by using the customer’s registered mobile number. A few providers have also enabled saving of receivers’ bank details and, thus, customers can simply use their mobile number to conduct a transaction without any need to remember/share the receivers’ bank details again.

When customers find it difficult to visit their preferred agents, they transact at outlets that are either referred to by colleagues/friends, or which they identify from marketing collateral at the outlets. Most often, customers recognise the logos of well-established banks (particularly State Bank of India) and are drawn to agent outlets that have these logos.

d. Repeat Transaction Phase

Most senders, who are typically either illiterate or semi-literate migrants, are daily wage earners. Hence, their preference for any channel (including agent outlets as well) has a direct relationship with the opportunity cost of using the channel. It is important to note that customers prefer OTC services because it requires little time (particularly as compared to banks, where waiting time is a major concern) and easier/minimal follow-up (as agents are commonly located near their places of work).

Hence, to build trust in the channel, it is essential to communicate the status of the transaction to customers on a near real-time basis at each step of the transaction. This is because customers are either unaware about any grievance redressal mechanism or believe that they have only one touch point, i.e., the agent. Most OTC providers already have a system in place to send SMS communication to their customers to inform them of the status of their transactions. This is very important for the sender, as this allows him to direct the recipient to withdraw funds from the appropriate cash-out point. Such communication assures senders about the success of the transaction and, if done correctly, almost ensures repeat transactions.

Since it is clear that repeat customers attach more importance to SMS communication than receipts provided by agents, providers should develop a system of SMS communications for both the sender and receiver throughout the different stages of transactions. This will include communication about the success or failure of a transaction, addition of recipient, etc.

Providers seldom put much emphasis on CX, focusing instead on incentivising agents to use their channel, thereby driving throughput. Since customers are indifferent to the underlying channels, it is difficult for providers to realise (and leverage) the advantage of customer stickiness without an agent incentives-based strategy. As we have seen in Pakistan (and was increasingly common in India until the recent strategic coopetition between the leading providers) this can lead to commission wars, with providers competing to pay the most attractive commissions. Ultimately, providers will want customers to insist on transactions being conducted through their channels. This will require differentiation that is clear to, and valued by, the customer.

In addition to building efficient SMS communications to allow customers to track their transactions, providers seeking to create a loyal customer base will need to look at other means to differentiate their services. In order to differentiate the channel adequately and make customers request specific services, providers may have to emphasise the other understated aspects of their delivery. These can include features such as real-time confirmatory messages via SMS, or transparency in pricing in the form of updated rate charts at agent outlets, and unambiguous voice based or text communication on charges to customers. Providers can also differentiate their services by ensuring that their systems are stable and reliable, thus minimising failure rates. Providers should also look to minimise agent-driven service denial by ensuring that the agents are well trained and compliant with organisational policies on liquidity and customer service. Finally, they can also enhance CX by educating and assisting potential customers to conduct trial transaction(s).

New entrants to the remittance space, such as payment banks and other money transfer operators, would benefit from a well-designed customer-centric approach that differentiates their service by optimising CX. Existing players, too, can start redefining their businesses by giving equal importance to CX and ensuring that their services become more attractive and efficient for their customers as well as agents, and thus build trust. For agents, interest and motivation are mainly driven by factors such as higher commission, ease of the transaction process, and timely provider support. OTC users, as noted above, choose agents instead of providers. Nonetheless, sub-optimal customer service is clearly affecting customer experience, which in turn reduces their trust and thus the uptake and usage of these services. It is, therefore, in the interest of providers to focus on both agents and customers. Focusing on delivering a positive customer experience at any touch point can act as a key differentiator for service providers in a keenly contested market space.

Full Report: PMJDY Wave III Assessment

This report captures aspects such as BM’s availability, transaction readiness, dormancy levels, and transactional details. It also focussed on Aadhaar seeding and RuPay card delivery/usage by PMJDY account holders.

Snapshots: PMJDY wave III assessment

The National Mission on Financial Inclusion is more commonly known as Pradhan Mantri Jan Dhan Yojana (PMJDY) was launched in August 2014. MicroSave has been closely following the progress of PMJDY through three waves (rounds) of surveys. PMJDY Wave-I was conducted in December-2014 followed by Wave-II conducted in July-2015. This report is the third edition of the survey commissioned to examine the progress of PMJDY. The report captures aspects such as BM’s availability, transaction readiness, dormancy levels, and transactional details. It also focussed on Aadhaar seeding and RuPay card delivery/usage by PMJDY account holders.