Based on over 2,000 mobile money agent interviews carried out in 2014 all over the country, the Pakistan survey report highlights findings on the mobile money agent landscape in Pakistan covering agent profitability, transaction volumes, liquidity management and other important strategic considerations.

“Nothing is as powerful as an idea whose time has come”- Victor Hugo

Recently, a new partnership has emerged between digital financial service providers and microfinance institutions to address the challenges of financial access among the un/under banked populations globally. The partnership can potentially offer benefits to not only the two partners but also other stakeholders including customers, MFI frontline staff and mobile money agents. In this blog, we discuss the benefits that the partnership is likely to bring to the stakeholders.

Benefits for MFIs

The partnership can help MFIs reduce costs, increase outreach, mitigate risks, deliver customer-centric products, and improve customer experience through increased convenience.

We discuss below some of the benefits that the MFIs are set to achieve.

i. With the use of digital finance, MFIs can mitigate cash risk as well as increase operational efficiency. The prevalent group lending microfinance model is highly cash intensive where both loan disbursement and repayment is made in cash, generally at customers’ doorsteps. The MFIs (and their customers) are thus exposed to cash risk (storage and transit) and incur cost to manage cash and related risks. This also eats into the MFI’s frontline staff time. They could have used this time more gainfully by sourcing new clients or perhaps providing more quality service to their existing customers. Carrying of cash to and from group meetings to the MFI’s branch and for deposit at the bank branch poses a threat to the lives of MFI’s frontline staff. As a result of all of these factors, the operational efficiency of MFIs is affected. With digital finance, customers can deposit cash into the MFI’s accounts at the nearest agent outlet. However, in such cases, the agent bears the cash handling risk.

ii. The MFIs can offer multiple products efficiently using digital finance. Traditionally MFIs have been providing a single credit product to their customers. Numerous research studies have shown that the clients require other financial products including, varied credit products, savings and other deposit products, insurance, pension, remittances etc. The need to diversify product offering for MFIs is more pronounced in India, especially after the Andhra crisis. (See Video: Going Beyond a Single Use of “No-Frills” Account: The Concept of Deferred Payments). Partnership with digital financial service providers gives MFIs the access to their partner network. Thus, the MFIs can offer complementary financial and non-financial products and services which they might not have been able to offer otherwise. In India, where MFIs are not allowed to accept savings, such partnerships have provided MFIs the opportunity to offer ‘saving deposit accounts’ serviced at the client doorstep. The product diversification helps the MFI to further strengthen their relationship with clients and at the same time gain insights on their financial behaviour. Since the customer transaction information is available in digital form, it can be used for detailed analytics to design and deliver customer-centric products.

iii. Digital finance, when deployed as an alternate delivery channel can help the MFI increase outreach in a cost-effective manner. The MFIs can leverage the digital finance distribution channel to design and deliver micro-credit products to non-MFI customers who regularly transact at such agent outlets. The prevalent microfinance models are resource intensive and sometime serving customers in remote geographies and difficult terrains becomes prohibitive. The large network of agents prove helpful to increase outreach to such remote locations.

Benefits for digital finance service providers and agents

The digital finance service providers through partnership with MFIs not only get access to the customer base of the MFIs but can also leverage the relationship that the MFIs have with their clients. This ensures a permanent catchment of customers for the agents who carry out regular transactions on account of loan repayment and saving deposits, if applicable. It also generates the possibility for the agents to cross-sell other products and services such as mobile airtime recharge, utility bill payments.

Benefits for customers

The partnership of MFIs and digital financial service providers also benefit customers. Microfinance clients get the flexibility to repay loans through their mobile phones without even going to MFI branches and avoid cash in transit risk. Additionally, they get access to other financial products and services, including saving, insurance, pension and remittance – all serviced through their mobile phone.

Several MFIs have already started to get into partnerships with digital financial service providers to leverage these benefits. Faulu and KWFT in Kenya are now using mobile banking services to allow clients to make loan repayments and deposits using their mobile phones.

Though many MFIs have started using digital finance, there are obvious challenges that need to be overcome. Some of the challenges such as reluctance of clients to pay mobile money charges, impact on group cohesion, low penetration of mobile money agents and bringing change in customer’s existing behaviour to adopt mobile money still need to be carefully addressed.

Weak Bank Mitr networks (with a reported annual attrition rate of 25-35%) in India could severely undermine the PMJDY and the DBT plans of the Government of India. Many Bank Mitrs have stopped offering services because of low commissions for processing G2P payments. However, the government released an Office Memorandum on 16th January 2015 setting the DBT commission rate for rural areas at 1% – much below the costs of delivering the monies and could potentially derail the entire financial inclusion effort of Government of India.

Task Force on Aadhaar-Enabled Unified Payment Infrastructure estimated that a 3.14% DBT commission would be adequate. A new MicroSave costing exercise found that the cost for processing transactions through the agent network is at least 2.63% for each transaction– much higher in more remote rural areas. Prima facie cost to the government for paying DBT commissions appears high, however it could be offset by huge potential savings from reduced administrative costs and reduced payment leakages. A 2011 McKinsey & Company analysis of India’s government payment system, estimated it to be Rs. 1 lakh crore annually (US$22.4 billion).

If the Bank Mitr network needs to be made more sustainable and ensure quality services, an adequate commission rate (MicroSave estimates this to be a minimum of 3%) for the first few years of PMJDY should be considered which can be reduced as the programme scales.

When you buy a bottle of Coca-Cola, are you buying it from the store or from the Coca-Cola Company? Whose customer are you? In digital finance, the provider (usually a bank or telecom) designs and brands the service, but it is the agent that provides the ability to cash-in and cash-out (CICO), and earns 40-80% of the revenues from it.

So, whose customer is it? The strategic answer is that both parties are providing a service, and the customer can choose to buy a different provider’s service (e.g. Airtel Money vs. M-PESA), or the same provider’s service at a different location (e.g. walk to a different agent). Hence, both the provider and agent should have an interest in ensuring the customer is satisfied, and incentives should be aligned to achieve this.

While conducting CICO for a customer is similar to selling a bottle of Coca-Cola, registering a customer for digital finance is different. Most agents are used to conducting transactions, not actively selling a service. Agents interviewed for this research reported the perception that providers benefit from registering customers, not them. Hence, when conducting a registration they were serving the provider’s customer, not their own.

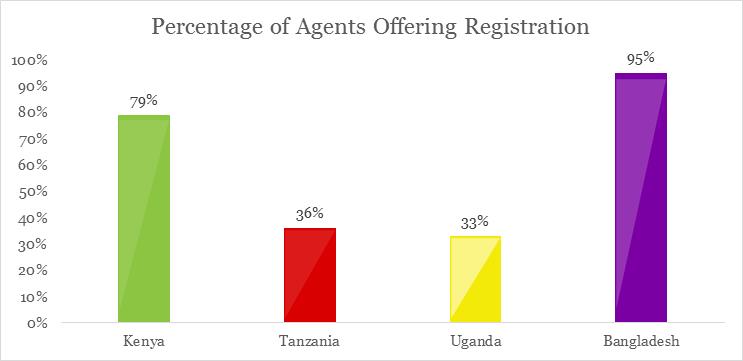

This helps explain the data from The Helix Institute below, showing not all agents are offering registration, especially in Tanzania and Uganda*. This is important because in most digital finance models registration has to happen before any transactions are done, and therefore any revenue is generated. The provider should design a support, training and incentive scheme to align the agent’s interests with theirs, but the first step is it to understand the agent’s underlying perceptions that drive their behaviour.

Registration is for Your Service not My Shop

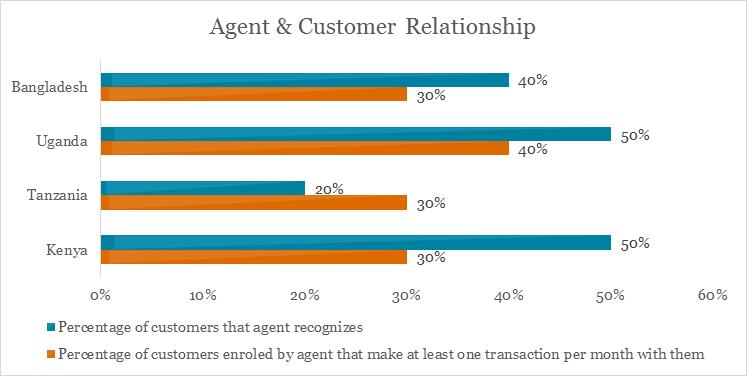

Agents report only 30-40% of customers that they register, return to transact at least once a month (orange bars in the below graph). This means on average they are registering customers that are not going to give them a lot of subsequent business and may become clients of competing agents in the area.

Agents questioned why they should actively recruit customers since they have no guarantee that new customers will be loyal to them. An agent said, “The customer may get to know about services from me, but go to another agent. What will be my reward for my efforts to sell to such a customer?”

Some agents view new customers as “suspect”, and thus choose to avoid any potential losses they may incur in serving the new, possibly “fraudulent” customers. These agent views stem from either their own, or another agent’s experience with fraud. In digital finance, agents report only recognizing 20-50% of clients (blue bars in the above graph), meaning this is a very common situation. One agent explained:

“When a customer I do not know walks into my shop I am on full alert. Sometimes if he looks suspect to me, I do not serve him. I just say I do not have float.”

Many agents prefer to serve customers with whom they are familiar, even though they know this may limit their profits. In these cases they are much more likely to view the customer as belonging to the provider, and some agents seem to only provide service to strangers on a case by case basis. Given these situations, where agents are not necessarily perceiving strangers as customers, it is important for providers to focus on support, training and agent incentives to try and encourage the provision of service.

Agents are Passive, so Support Them

Customer acquisition is not a natural role most agents play. As one agent reported, “It is not my job to look for new customers; that is the work of Safaricom.” Thus the provider needs to make the customer aware of the product, and curious enough to go and start asking an agent about it. Generally, the agent will not start this conversation for the provider. This awareness and curiosity is built through highly visible and sophisticated above-the-line (ATL) marketing strategies common in the telecom industry, and must be done by all providers, or else agents will not feel supported.

Agents also compare their affiliated provider’s marketing efforts to competitors. Some Airtel money agents do not engage in active recruitment of customers because they perceive Airtel to be passive. An agent explained:

“Airtel should encourage more customers to join their network just like Safaricom does. Every day Safaricom is doing an advert in the dailies, and that is why they have many customers.So if Airtel is not as actively engaged as Safaricom and is struggling to get customer numbers, what about us agents?”

Providers need to do the requisite marketing to bring the customers into the agency, already on their way to wanting to register, and then incentivize and train the agents to close the sale and process the registration.

Agents need Motivation, so Train & Incentivize Them

MicroSave has consulted a lot of providers on designing their agent training curriculums. One of the major trends is that usually the training manuals are focused very much on compliance, and processes, and seldom do they have a sales component. It must be understood that agents need this type of training to understand how to pitch the value proposition with confidence, and tact.

The marketing and training support are crucial so that customers come in to the store, and agents know what to do when it happens, however, the agent also must be motivated to employ their training. Successful providers understand this and report paying over one U.S. dollar per customer acquired. Good incentive schemes make commissions payment contingent on the customer making at least one deposit so the provider can better ensure the customers interest in the service, and some incentive schemes also give the agent commission on some of the ensuing transactions the customer makes, to ensure the agent makes more than a one-time fee.

It would be interesting to further look at transaction commissions to investigate if agents could offer loyalty schemes (e.g. make five transactions with me this month and get the sixth free) to customers to encourage more ownership of them as well.

Conclusion

Theoretically customers are shared by agents and providers, but practically, the agents perception is different for different customers (ones they know vs. strangers) and the activity required (registration vs. CICO). Providers need to understand this to better support agents with marketing efforts, training, and aligned agent incentives, so that they feel more ownership over the customer relationship. This should help improve agent motivation to provide a consistently high quality of service to all customers.

*More data on service offerings is available from The Helix Institute country reports on Kenya, Tanzania, Uganda, and Bangladesh. Data in East Africa was collected in 2013, and Bangladesh data was collected in 2014.

How much does an agent need to earn to be satisfied, and stay motivated enough to provide a high quality of service to customers? Behavioral science teaches us that people anchor their appraisals of value to other numbers around them in the ecosystem. Marketing firms understand this concept well, often enticing us to perceive a product as affordable by placing it next to a similar higher priced product (e.g. different brands of wine) on a supermarket shelf. In this example, people anchor their judgment of what the product is worth relative to the high priced item, and subsequently judge the other of good value, hopefully then happily buying it.

However, people do not always anchor judgments of value to what is physically around them, sometimes the anchor comes from past or predicted future experiences. When a product in a store is discounted, people are more likely to purchase it as they anchor their perception of its value to what it used to cost them, even if that price was inflated to begin with!

With regards to agents, it is important to understand to what they are anchoring their revenue, as that is effectively what will determine their level of satisfaction with it. There are a number of obvious options, like the monthly wage of the person they employ to conduct the transactions, or the revenue they earn from another product they sell like Coca-Cola, and more research would be revealing as to what determines how these anchors are chosen.

What our research revealed is that these anchors can be quite dynamic, changing overtime as the business model for digital finance changes. This is very important to understand as the business model in digital finance always evolves as it scales and diversifies, and it is imperative to keep agents happy through this process so the quality of service remains high throughout these transitions. We interviewed 60 agents in Kenya and Uganda, and looked through data from The HelixInstitute of Digital Finance to identify some important events in the evolution of the business model that seems to affect which anchor value agents use to evaluate their satisfaction with the digital finance business.

Perceptions of Future Growth:

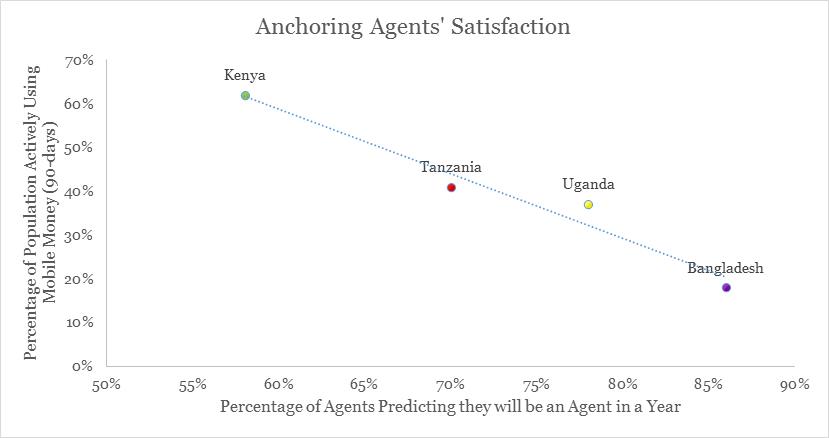

Interestingly, data from Helix Institute research in Bangladeshand Kenya, showed that while agents are earning relatively the same amount in monthly commissions US$170 vs US$175 (in PPP terms) respectively, in Kenya only 58% of agents predicted they would still be an agent in a year’s time, vs. 86% of agents in Bangladesh. When we include Tanzania and Uganda in the analysis and compare the percentage of agents predicting they will continue as an agent to the market penetration rates for mobile money in those respective countries, the results appear to show a very strong negative correlation.

This leads us to believe, as mobile money penetration in a country increases, there are less new customers to register, and the growth rate of the service starts tapering off. This would cause the median agent commissions to decrease, or at least increase at a decreasing rate (holding a handful of other variables constant), and lead to lower levels of willingness to continue, as agents are comparing their future earnings to those of the past. Therefore, in Kenya where market penetration is higher, we observe a smaller percentage of agents willing to continue as opposed to Bangladesh where the market is still ripe for growth and agents are much more dedicated to the business – even given they are earning relatively the same amounts.

Agent to Merchant Transition and Introduction of Master Agents:

In Kenya, Safaricom has reported recruiting over 32,000 active mobile money merchants (December 2014) to complement their existing network of cash-in, cash-out (CICO) agents, however they have had lesser success converting existing CICO agents to become merchants, than new business to serve as merchants. While there are certainly a number of reasons for this, one of the major ones M-PESA agents report is they were used to earning commissions on CICO and therefore they did not feel like having to pay a fee on merchant transactions was fair. In essence, they are anchoring the value of the merchant payments to their past commissions.

In Uganda, MTN recently introduced master agents after several years of operations. Whereas agents used to receive 100% of commissions, MTN agents reported they now need to give 10% of their commissions to the master agent. The agents are now faced with the problem of anchoring to the past commission level they earned. They now feel like they are not getting as good of a deal relative to how the system previously worked.

What Does This Mean For Providers?

When gauging the satisfaction levels of agents in your network, one needs to know much more than just how much agents are earning. The examples above show that it is also important to understand how it relates to what they were previously earning and how much they expect to earn in the future. Further, there are critical junctures and trends in the evolution of the business model, like the introduction of master agents, the building of a merchant network, and reducing future growth rates, which must be monitored carefully as they can easily cause agents to anchor to a value that makes them decrease their satisfaction with the commissions they earn.

Savings products and services have traditionally been designed assuming rationality and willingness of people to save and liquidate towards life-cycle goals. However, in real life, low-income mass market people continue to save in low (or often negative) interest bearing informal savings schemes, and do not commit, choose and/or continue medium or long term savings programmes designed by formal financial institutions. This Note analyses these trends through a behavioural economics lens and tracks the behavioural factors responsible for – preferences for informal savings; procrastination towards savings commitment; discontinuance of committed savings; and overwhelming preference for “fixed return” schemes. The Note suggests alternative strategies that can enhance commitment and usage of formal savings schemes, especially in low income mass market segment.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.