There is growing concern about customer protection. This can be seen from initiatives such as Code of Conduct for mobile money players by GSMA, the update of the SMART Campaign’s client protection to create principles for DFS. These initiatives represent industry-wide commitments to build awareness, better practices, and standards that could contribute to strengthening customer risk mitigation in the financial inclusion space.

Customer protection plays a direct role in reducing risks faced by customers. It plays a major role in building and maintaining trust of customers in digital financial services.

MicroSave’s study for the Omidyar Network on customer protection, risk and financial capability in India tried to understand the extent to which customer protection practices were embedded into DFS offerings in India. The research examined the effectiveness of these customer protection practices and the ease with which customers and agents could access them.

The following sections discuss the important SMART Campaign Principles which are applicable here:

- Recourse: The grievance mechanisms available for customers and agents

- Transparency: How terms and conditions are communicated to customers and agents

- Data Privacy: How customers and agents safeguard their data (and money)

1. Recourse

1. Recourse

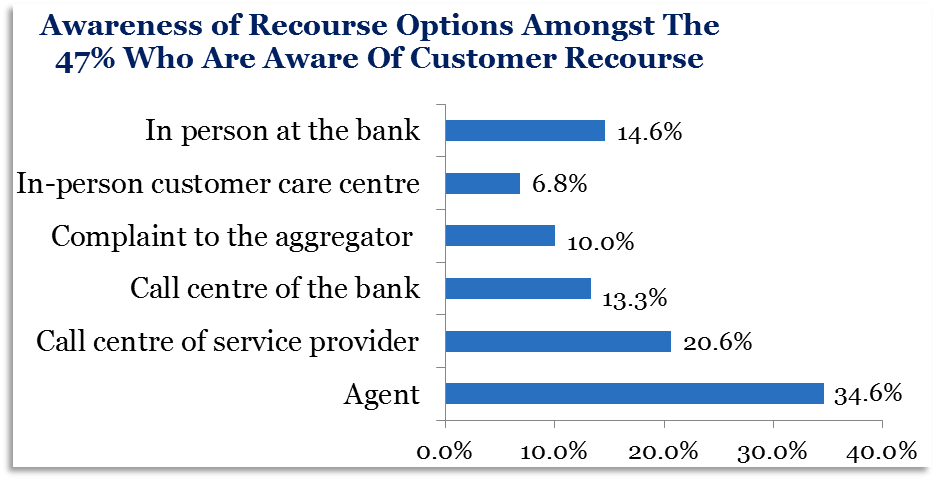

Only 47% of customers were aware of recourse options and their primary source of information was the agent. Low awareness of customer recourse can reduce customer trust in FSPs. Furthermore, it makes customers highly vulnerable and dependent on agents.

Even though experienced users have shown that they use the call centre more often than inexperienced users, overall awareness level is still very low.

The agent is the most important source of recourse options. Evidence in the FII research and CGAP country case studies confirms that DFS customers often look to agents to resolve problems. 98% of Indian customers say that the agent will be able to support them in case they face any risk in future. When compared globally, in Ghana, for example, 61% of mobile money users say they turn to an agent, and in Rwanda 52% report doing so (InterMedia, 2015). This highlights the emerging nature of DFS in India, where awareness levels are low and dependency on the agent is extremely high.

So what happens when customers have complaints about the agents?

Only half of customers say that they know what to do if they have problems with an agent. The research showed that customers prefer to discuss agent-related issues at the bank branch or by contacting the service provider’s call centre. A small percentage of customers complained about agent-related issues to the agent himself. This phenomenon could have two possible (though inter-related) explanations:

a) the agent is from the same community or from a nearby location, which results in high level of association with him/her; and

b) the absence of a proper recourse mechanism.

88% of customers believe that the recourse mechanism is efficient enough to resolve any issue faced by them. This could be a case of misplaced belief, as instances of risk have been low and, therefore, the need to actually access recourse has been limited to date.

And what of agents’ ability to resolve problems?

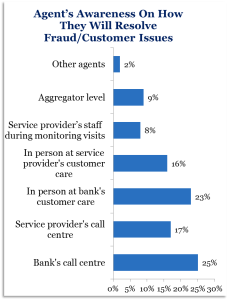

While 79% of agents are aware of recourse options, only 24% of agents who faced problems actually used a recourse mechanism. This figure is disturbing since three-fourths of the agents didn’t even try to resolve problems, suggesting a broken system/process.

While 79% of agents are aware of recourse options, only 24% of agents who faced problems actually used a recourse mechanism. This figure is disturbing since three-fourths of the agents didn’t even try to resolve problems, suggesting a broken system/process.

As a proxy, this is also corroborated by the low use of call centres. The ANA India Research shows that only 52% of agents say that they know about call centre option to resolve queries.

Call centres can and should play an important role in customer service and protection in digital finance deployments. Given India’s world leadership in call centre management, it is to be hoped that the current situation will not persist for too long. That said, the pitifully slim margins for DFS providersmean that they will always be looking for opportunities to cut costs.

In the next blog in this series, we will look at Transparency and Privacy.

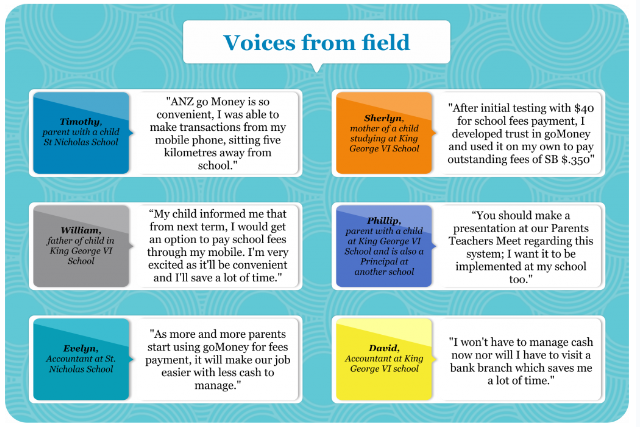

With a big smile on his face, Timothy can’t help but show his friends and family, the newest feature of his mobile phone. When people ask him the reason, he proudly says “You know what I have done using this? I have paid school fees for my daughter Jessy, right from the comfort of my home!”

With a big smile on his face, Timothy can’t help but show his friends and family, the newest feature of his mobile phone. When people ask him the reason, he proudly says “You know what I have done using this? I have paid school fees for my daughter Jessy, right from the comfort of my home!”

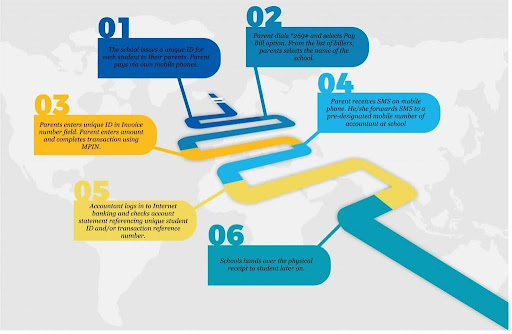

The project team, consisting of relevant stakeholders- ANZ Bank, PFIP, Microsave and the Premier Group, met authorities of various schools in Honiara to explain to them the value proposition of the digitised system. Once the school authorities were convinced of the merit of the system, approvals were sought from school’s boards.

The project team, consisting of relevant stakeholders- ANZ Bank, PFIP, Microsave and the Premier Group, met authorities of various schools in Honiara to explain to them the value proposition of the digitised system. Once the school authorities were convinced of the merit of the system, approvals were sought from school’s boards. Once the schools went live on the ANZ goMoney platform, the bank trained the parents in making fees payment transactions through it. The school authorities also received training to reconcile transactions made through ANZ goMoney and how to settle amounts in the manual record books of the schools. The team provided constant handholding support to the school authorities and parents during the entire process to build their skills and confidence to use the platform.

Once the schools went live on the ANZ goMoney platform, the bank trained the parents in making fees payment transactions through it. The school authorities also received training to reconcile transactions made through ANZ goMoney and how to settle amounts in the manual record books of the schools. The team provided constant handholding support to the school authorities and parents during the entire process to build their skills and confidence to use the platform.