In 2012 Ignacio Mas worked with MSC to look at the state of digital financial services in India, the type of products that poor people want, and the role of microfinance institutions/SHGs in digital financial services systems. In this video he shares some of his thoughts on digital financial services systems not just in India but worldwide. He stresses that a product must be simple yet useful for being relevant to poor people. He further elaborates his point by addressing the following questions.

What is the real value proposition of a basic No Frills Account?

How can we make them more relevant for poor people?

Do we really need a bouquet or range of products?

How can we reconcile relevance with simplicity/use-ability?

MicroSave Policy Brief #9 describes the true reach and quality of India’s BC networks, the design features of successful agent networks, and the policy and regulatory interventions that could help catalyse the roll-out of denser, higher-quality agent networks in poor communities across India. The Brief details the impressive growth in the number of agents but highlights that a very high proportion of them are dormant or simply unable to make transactions for want of liquidity or hardware. The Brief highlights the reasons for the high levels of dormancy amongst agents and the danger that it is irreparably damaging trust in the agent-based system. This clearly has significant importance for both the Aadhaar-enabled direct benefit transfer programme and the financial inclusion agendas of the Government of India. It further underlines the need for immediate remedial action by policy/regulatory actors, as well as commercial players, to make a concerted push to resolve the remaining barriers – before the complete break-down in the agent system, and the loss of the trust of India’s masses, become a lasting impediment.

MSC supports financial institutions across the world to develop and implement effective performance management and staff incentive systems. In an effort to promote effective staff incentive system our Senior Analyst Amit Garg shares the key concepts that a consultant or practitioner developing staff incentive system should pay attention to.

Regulation is instrumental in development of microinsurance in any country. Microinsurance regulations have been, and are being, developed in several developing countries, with variable success rates. The microinsurance sector is trying to understand what aspects of regulation create an effective and efficient microinsurance market in any country. This note discusses a framework for comprehensive analysis of microinsurance regulation through assessment of three broad aspects: regulatory capacity, clarity in regulation and promotion of microinsurance.

In Finding the Right Job for Your Product, Clayton Christensen implies that customers may not use a product/service strictly for the benefit intended by those offering it; rather they are more often driven by their situation or a job they want to get done; and include the emotional elements such as fear, fatigue or frustration; anxiety or anger; panic, pride or pain etc. An exploration of the purchasing behavior of the customers through the traditional constructs of demographics or functional might not take into account all the situational factors. Ignacio Mas further elucidates the importance of this approach in his blog.

Understanding customers’ purchase decisions are at the core of the marketing challenge. We know it’s about segmenting in order to get more granular customer insights; identifying customers’ alternatives in order to put a given product in a wider context; evaluating the needs and the benefits; as well as the barriers to adoption. But all too often the analysis becomes mechanical, customer and product market lines are drawn rather arbitrarily, and it is all expressed in a cool technocratic language that customers themselves wouldn’t recognize.

We wondered whether Clayton’s approach could be applied to the choice of financial services by users. We set out to find out that. We identified three methodological challenges which later became our research objectives. These were:

First, what is the ‘product for hire’ we were interested in: Is it money? Is it any financial service? Is it a particular savings vehicle like a bank account or the mattress?

Second, how concretely should the ‘job to be done’ be specified: Should it relate to planned expenses or the underlying psychological needs?

Third, what is the right ‘situation’ to ask those questions in: When you earn the money? In a quiet reflective moment when you are thinking about the family and the future? When you kneel down in front of your mattress to stuff it some more?

We used two approaches to find answers to our questions. The first approach was to understand the role of money in the lives of people. In discussions, we referred to the highly abstract, psychological, or at times even philosophical need for money. We discussed the general role of money in the life explored about jobs they wanted to get done by using the money. The discussion focused on why money is so important for, and beyond, fulfilling the basic needs. Respondents felt comfortable talking about their latent needs and their job characteristics. We were able to understand a broad level of abstract needs that exist in the subconscious mind. Further discussion on prioritization provided insight on the level of importance a job had amongst various jobs which they wanted to get done. The discussion, however, did not provide an understanding on “job candidates” or options that the person might choose to fulfill the job.

The second approach was to understand what causes an action. We explored two distinct situations in this approach. One in which a person has just received some money. This was the moment when we could understand how the person starts planning to use the money. The second situation was to talk to a person who is putting the money to its intended (or otherwise) uses. The discussion focused on getting the person to trace back to the moments of determination and discuss the situation around that moment. We understood the risks in both these situations. In the former, while responses would be more virtuous than the real actions and with the latter, the responses were a retrospect and could be more rationalized. The discussions were rather short lived as they focused on the current situation only. At the same time nevertheless, it enabled the respondent to think deeply about the importance attached to his current job and the selected job candidate. This enabled us to understand the thinking process. The discussions also enabled fair discussion on the choice of a job candidate, their preference, and comparison with other options that could have suited the job.

Both approaches were useful in eliciting jobs that people get done, while the former gave insights about some situations where people make decisions or choices, the latter helped us understand this situation in deeper detail. We recently used these approaches while conducting Metamon research in India and Bangladesh. Please read more about Metamon research here and here.

We weren’t expecting to nail down a pithy Christensonian statement with ease, and the challenge loomed larger as we got more into it. Financial considerations seem to touch every aspect of sentient living: the desire for your children to lead a better life than you had; to minimize life’s daily hassles and humiliations; to feel like you are keeping up and fulfilling your obligations to kith and kin; to reduce the feeling of present or future dependency etc. In addition, financial considerations stretch over time; they don’t appear in our lives momentarily unlike deciding to drink a milkshake or eat a snack. Yet despite these difficulties, we felt that centering the conversations with people on the situations rather than on themselves, seeking the deeper emotional motives they felt at the time and not just recording their financial choices, led to more meaningful exchanges.

Financial decision making and the corresponding behavior of financial service users is indeed complex. The researchers may need to move away from traditional (question-answer based) methods to start to use more sophisticated research techniques – many of which we have discussed in “Qualitative Research Tools for Market Research: Experiences from MetaMon Research”. Exploring situations in which a financial decision is taken or put into action, is definitely one of such method.

Krishna Thacker, Sonal Agrawal, Mukul Singh, and Ritika Srivastava conducted field research. Ignacio Mas and Graham A.N. Wright guided the team.

We acknowledge the support of MicroSave’s Partners; Bank of India and Lok Biradari Trust for gracefully providing us with an access to interview their customers.

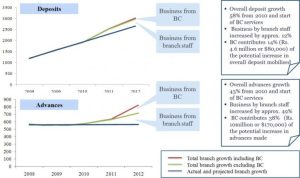

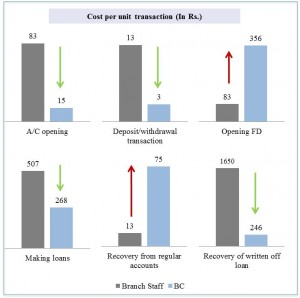

Earlier in the year we highlighted the remarkable progress that Equity Bank has made as it rolls out its agency banking, and how more transactions are now performed at agent’s than in the bank’s branches. This blog presents data from work done by MicroSave in 2012 to look at how agent banking worked for a bank in India. This bank runs its own agent network, supervised from, and working closely with, the branches as a “distributed banking” system. MicroSave has already calculated the type of savings that a bank might make at the aggregated level, concluding that the annual average cost of saving a customer through the branches (around Rs.400-500 or circa $8) could be slashed to Rs. 65-125 (circa $2). Similarly Kabir Kumar and CGAP concluded that in Latin America, “Transaction costs at agents range roughly from $0.27 to $0.58 per transaction and are 50% the transaction costs at branches and ATMs”

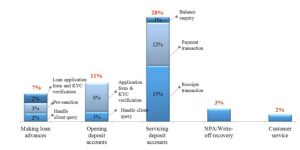

In 2012 we were able to look at this on a detailed, disaggregated basis. Conducting sophisticated activity-based costing we were able to look at the relative costs of conducting different transactions through branches and through business correspondent (BC) agents. As can be seen from the graphs, most but not all costs decreased. It is important to note in this case that the agents were conducting traditional BC (cash in/out) transactions as well as business facilitator (BF) type transactions (selling to and referring potential loanees as well as fixed depositors (FDs), collecting loans and recovery of loans that had been written-off). Indeed, this combined BC/BF role may well be essential for agents to break even given the extremely low commissions paid to agents in India for cash in/out transactions.

Furthermore, we calculated that the activities that could be undertaken by the BC agents were currently taking 51% of bank branch staff time as shown in the diagram below.

This means that if BC agents are deployed efficiently, a large part of the staff time could be freed up to focus on conducting high value-low volume transactions, as well as marketing to and servicing high net worth individuals. This, of course assumes that there is scope in the market for growth in services to high value customers. In the relatively remote area of rural India where we conducted the analysis, these customers were indeed present and a combination of the efforts of both branch staff and their BC agents yielded spectacular increases in business at both the branches and through the BC agents.

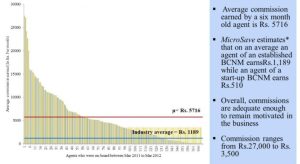

As a result the BC agents were earning an average of Rs.5,716 (circa $100 ) a month – five times the national average for BC agents in India. And the 20% most successful agents were earning more than Rs.10,000 (circa $175) a month.

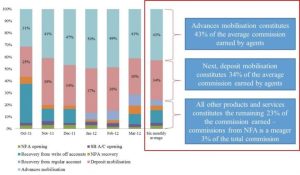

As highlighted above, three quarters of this revenue comes from two key activities: marketing loans, doing the initial paper work and referring loanees to the branch for final review and authorisation; and marketing/ servicing deposits (in particular fixed deposits).

Yet despite the clear business opportunity to serve the low income market segment, most banks remain reticent and unwilling to commit to agency banking.

Is it because banks are still unable to see the business potential or believe that the returns are higher elsewhere?

Or is it that banks are fundamentally uncomfortable with a distributed banking model and running an agent network?

Or is it that bank’s key management bandwidth is fully occupied with the battle to serve the higher value market and the burgeoning middle classes?

Or is it that the lowest quality staff is assigned to financial inclusion and agency banking as it is typically viewed as a corporate responsibility or mandated requirement.

Who knows – but the first banks to wake up and sieze the opportunity have the potential to dominate the urban and rural mass markets … as Equity Bank is demonstrating.

This site uses cookies, by continuing your navigation, you agree with our Cookie Policy.

In 2012 we were able to look at this on a detailed, disaggregated basis. Conducting sophisticated activity-based costing we were able to look at the relative costs of conducting different transactions through branches and through business correspondent (BC) agents. As can be seen from the graphs, most but not all costs decreased. It is important to note in this case that the agents were conducting traditional BC (cash in/out) transactions as well as business facilitator (BF) type transactions (selling to and referring potential loanees as well as fixed depositors (FDs), collecting loans and recovery of loans that had been written-off). Indeed, this combined BC/BF role may well be

In 2012 we were able to look at this on a detailed, disaggregated basis. Conducting sophisticated activity-based costing we were able to look at the relative costs of conducting different transactions through branches and through business correspondent (BC) agents. As can be seen from the graphs, most but not all costs decreased. It is important to note in this case that the agents were conducting traditional BC (cash in/out) transactions as well as business facilitator (BF) type transactions (selling to and referring potential loanees as well as fixed depositors (FDs), collecting loans and recovery of loans that had been written-off). Indeed, this combined BC/BF role may well be