The Philippines, an archipelago of 7107 islands, is an important remittance market in Asia. Over 9.5 Million Overseas Filipino Workers send over US$ 24.3 billion (10.7% of the GDP) every year which makes Philippines the third largest recipient of remittance in Asia after India and China. In this vedio, Shivshankar V., our Resident Expert in the Philippines, talks about the remittance market and about the project in which MicroSave is supporting a consortium of financial institutions in the Philippines to set up a remittance company catering to unbanked migrant population in rural areas.

Blog

Non-Financial Services for MSMEs

Besides access to finance there are range of capacity building services that MSMEs need for their growth and development. Non-financial services are such capacity-building inputs which are mainly targeted at enhancing the performance of a business enterprise. In this video, MSC’s Products and Delivery Channels Expert, Raunak Kapoor, shares his experience on the role and importance of non-financial services in complementing financing efforts for enterprises. He further talks about the role of different stakeholders including financial institutions, business development service providers and other support partners, such as donors in expanding the provision and effectiveness of non-financial services design and delivery.

Challenges to agency business – Evidence from Tanzania and Uganda (Part- I)

As part of The Helix’s Agent Network Accelerator (ANA) survey programme, we interviewed 2,052 agents in Tanzania and 2,028 agents in Uganda. We looked at a wide variety of issues including:

- Agent and agency demographics

- Liquidity management

- Provider support for agents

- Agents’ business model viability

- Core operational issues

Under the latter section, we asked about the biggest operational challenges that agents were facing. The responses were instructive.

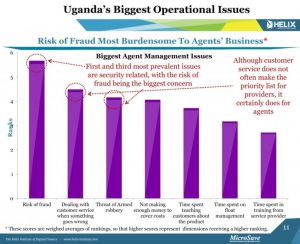

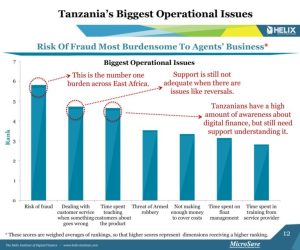

Fraud and armed robbery

Top of the list in both Uganda and Tanzania was fraud – closely followed by armed robbery. We have discussed these problems in the blog “Why Rob Agents? Because That’s Where the Money Is” about a year ago, and clearly they persist.

One of the key ways to address the challenge of fraud is through on-going support and training for agents, so that they are aware of and can respond to the latest scams being perpetrated in the market. And yet, the ANA surveys repeatedly show that agents receive very limited training.

In Tanzania, 55% of agents have never undergone refresher training, and in Uganda, 57% of agents have never undergone refresher training. In Uganda, only 33% of agents were visited by the provider, whereas 46% of agents report not being visited at all. Of those who were visited 35% report, they were with no fixed frequency. In contrast, 76% of Tanzanian agents report being visited. Of those visited about three quarters were visited directly by the provider with a frequency of at least once a month. Clearly, the agents are not getting the support they need. And given the prevalence of agents reporting “Time spent in training from a service provider”, much (if not all) of this training and support needs to be on-site as part of providers’ agent monitoring systems.

Customer service

Second on agents’ lists of challenges – both in Tanzania and Uganda – was dealing with customer services when something goes wrong. While customer service does not always appear to be a key area of focus for providers, it is a very real challenge for agents … and, if not adequately addressed, has the potential to undermine trust in digital financial services. Many, if not most, customer service issues arise from customer transaction errors and the resultant requests for reversal. This leads to the challenges of repudiation policy so well outlined by Joseck Mudiri in “Fraud in Mobile Financial Services”.

Providers can essentially choose between three policies on repudiation:

- No Repudiation: The provider opts not to interfere with the transactions, callers are advised to either resolve the matter with the recipient directly or seek legal redress.

- Call Centre Repudiates Instantly: The provider’s call center may repudiate transactions on the strength of the sender’s request only without consulting the recipient.

- Funds are Suspended Prior to Repudiation: Under this scenario, the customer calls the provider’s call center and requests for repudiation. The call center immediately suspends the funds to ensure that they cannot be withdrawn. The recipient is then called. If the recipient insists that the funds are genuinely theirs, the call center employees release the funds to the recipient. However, if the recipient accepts that the funds belong to the sender, the funds are reversed back to the sender.

Each of these policies has advantages and disadvantages – but all require a careful agent and customer education to manage expectations and behavior.

Effective fraud management, security and customer service require investment from the agents and/or mobile money providers. This, in turn, affects profitability and the ability of agents to educate/market to customers and offer a range of products. These aspects will be discussed in the next blog in the series.

G2P Payment: A Job Half Done

Direct Benefit Transfer program was thought to be effective method of achieving goal of financial inclusion. Its effectiveness was thought to be an outcome of necessity of making payments to individual bank accounts and also because of regularity of payments. However, due to operational issues its progress does not inspire much hope. At best DBT as tool of financial inclusion is a job half done.

Agent Network Accelerator Survey – Kenya Country Report 2013

The Kenya Country Report is based on a nationally representative sample of over 2,000 mobile money agent surveys carried out at the end of 2013, all over the country. The report finds that after seven years of market development, Kenya continues to be dominated by one strong provider with an army of exclusive agents. These agents are well supported, and generate very high transaction levels but only offer a limited suite of products and have fairly low profits. Download to read the report in full for more exlusive insights and data

Mobile Money Merchant Payments – What does the Future Hold?

In October 2012, GSMA MMU asked the burning question; ‘Can mobile money work for merchant payments?’ Across the developed world cards are being swiped, dipped or waved to pay for everyday purchases, but the question remains if mobile money can, or will, have the same levels of usage in the developing world.

Currently mobile money providers have thousands of agents who facilitate the exchange of cash and electronic money. They are usually small retailors, and are paid a commission for offering the service. In contrast, mobile money merchants generally do not facilitate these exchanges, but simply accept electronic payments in exchange for the goods or services they provide. The merchant, the customer, or neither is charged a fee by the provider for using the mobile money service. These merchants are still very new, but the 2013 State of the Industry Report, shows adoption of merchant payments is slowly gaining traction, with 65% of the mobile money deployments now offering the service. Although activation rates are still very low, this is to be expected with mass market strategies that target micro, small and medium enterprises, and in places like Kenya, we see the numbers already improving.

In this blog we’ll discuss why merchant payments are important, what they mean for the evolution of the agent network, and where they might be headed.

Why is it important?

Why is it important?

Currently, mobile money is only being popularly used for a small subset of payment purposes, mainly small airtime top-ups, infrequent bill payments or transfers to a friend/family member (P2P), which cumulatively account for 97% or transactions by volume or 89% by value globally (State of the Industry 2013). Even in the famous Kenyan market, the CEO of Safaricom, Bob Collymore notes that 98% of transactions are still done in cash. Further, people are using their mobile wallets for savings, but the amounts stored are very low, and the majority of funds are still withdrawn from the system quickly after they are received.

Merchant payments add another use case for mobile money by enabling customers to pay for goods and services from the value stored on their mobile wallets. This additional service for the customer encourages them to transact with electronic money more often as there are more options for doing so, and also incentivizes them to store money electronically as it becomes more useful tool for making payments.

This is attractive to the provider as both these changes in behaviour can increase their revenue, and potentially goes a long ways towards increasing usage of the systems as payments to merchants are made so frequently. According to industry insiders “the ratio of merchant payment transactions to P2P transfers is 16:1 in a developed market.” Although we cannot directly compare the developing world to the developed, it does seem that this indicates that there is a huge opportunity for digital merchant payments. Therefore this is a key element in making mobile money more relevant on a daily basis, and evolving the payments system away from cash and onto the digital platform.

What does this mean for the evolution of the agent network?

When mobile money hit the market, many providers engaged existing Fast Moving Consumer Goods (FMCG) retailors to try and reach scale quickly. They convinced the retailors in these networks to additionally provide cash-in and cash-out services, and therefore evolved their functionality. Many predict that these agents will be converted into merchants, accepting digital money for their goods and services rather than exchanging it for cash. However, for customers, paying in digital money in some cases incurs a fee and takes longer than paying in cash, and for agents receiving a commission, transitioning to merchant payments likely means forgoing it. This makes it a hard transition to sell and means providers around the world are struggling with a number of different models to try and make it work.

In Kenya, the Lipa na M-PESA merchant payments service that Kopo Kopo and several other aggregators help manage charges the merchant 1% of the value of the transaction, enabling the customer to conduct it for free. Kopo Kopo entices businesses to become merchants by providing them with business analytics from the transactions they make on the system, and focusing their pitch on specific value propositions like reducing pilfering associated with cash businesses. However, the design of this system means that it is generally more alluring to more sophisticated businesses that generally were not previously targeted as mobile money agents. The result in Kenya is that instead of building on top of the agent network, the merchant network seems to be evolving mostly alongside it, increasing the overall places in the country where mobile money can be used.

Where are we and how might we move forward?

Where are we and how might we move forward?

From Lipa na M-PESA in Kenya, to TigoPesa in Tanzania, ZAAD in Somaliland and EcoCash in Zimbabwe, there are a myriad of different attempts to build models in this field. After about two years of market development it is safe to say we are still not sure which ones will succeed, but in Kenya we now have two years of data from which we can make some astute observations to help the industry understand what we do know.

Kenya is obviously a unique market because of its maturity where 62% of the adult population actively uses M-PESA already. Merchant payments should be easier in an environment like this where people already trust the system, and are accustomed to holding some digital money on their phones that they can use to make purchases. Emulating this stage of market maturity is likely something providers will need to do first before launching merchant payments, as Ignacio Mas quips, you cannot make payments with an empty wallet.

However, Kenya is also a success story in part because of the innovative work Kopo Kopo is doing to select, acquire, train and support new merchants. Launched in 2012, it now manages over 12,000 merchants for the ‘Lipa na M-PESA’ (‘Buy Goods’) service. It has designed analytics to reduce inactivity in the network, and has even launched Grow, a merchant cash advance service to encourage merchant usage and retention, which caught the whole industry’s attention. Some of the techniques used are similar to those used for managing agents and can be important, and others are just being learned.

This marks the first blog in a series that will explore the emerging world of merchant networks in mobile money to shed light on what some of the best practices in the industry currently are and where the industry seems to be headed.

The blog was co-authored with Ben Lyon – Director of KopoKopo Inc