This report summarises the intent, activities, outputs and key lessons from an ambitious program of field work which sought to capture vividly and succinctly the essence of how ordinary people think about the management of their money and resources.

Blog

Paint by numbers: Profiles of bank agents in India

India’s financial inclusion efforts remain in a difficult transition period. And agents, or business correspondents, as they are known here, are not the all-purpose, “last link” solution everyone had imagined between banks and low-income, remote or migrant customers.

Despite the Reserve Bank of India’s (RBI’s) commendable efforts to move financial inclusion aggressively forward (this year’s target is ~200,00 agents, a fourfold increase from 2011), almost no one immediately involved with these efforts is happy right now. (Please also see MicroSave’s blog on RBI’s new, more relaxed rules regarding businesses and banking licenses.)

It has been tempting in some circles to imagine that agents and their managers are simply not trying hard enough. Both are too easily discouraged and too quick to complain when easy profits are not forthcoming.

One reason for these assumptions is that much of the evidence thus far has been either anecdotal and qualitative, or one-sided (usually from the banks’ or microfinance institutions’ perspective).

MicroSave decided that a careful look at the agents’ books might help all parties better understand the specifics of the underlying problems and how best to address them. (Please see MicroSave’s Rapid Agent Assessment for more details.)

The specifics do indeed help explain the agents’ discontent.

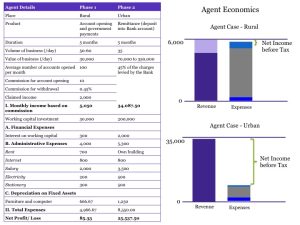

Urban business correspondents who offer migrant-worker remittance services, the most lucrative source of revenue, in shops that attract constant traffic can clear almost Rs.10,000(~US$185) in monthly profits. But these instances are rare (only 2-3%).

The more normal situation for these agents is close to break-even with little hope of achieving their net-income expectations of Rs.20,000-30,000 per month. Rural agents fare far worse with less access to remittance income and markedly lower commissions (sometimes by as much as a factor of 10).

Agents’ books also reflect:

- Erratic commissions and late payments;

- Technology delays that cost them money and customer trust;

- Little support for marketing and advertising;

- Even less contact with the banks they are representing.

The agents’ managers aren’t making money either. Their woes include:

- Low/no cooperation with the banks;

- Agent inactivity, which MicroSave estimates to be as high as 73%, and churn (many new agents quit after nine months or sooner);

- Unreliable bank servers and connectivity, particularly in rural areas;

- Liquidity management, insurance, security risks for both their cash-in and cash-out agents;

- Late bank payment of agent commissions.

Perhaps the worst indictment of the agents’ role in financial inclusion, however, is that the intended beneficiaries—poor people without access to full banking services—are also unsatisfied. Most would preferto deal with local agents they know, especially if they are more patient with the illiterate and elderly.

Perhaps the worst indictment of the agents’ role in financial inclusion, however, is that the intended beneficiaries—poor people without access to full banking services—are also unsatisfied. Most would preferto deal with local agents they know, especially if they are more patient with the illiterate and elderly.

Nevertheless, the almost daily server downtime, plus high agent turnover in many areas, mean rural customers in particular have two unappealing choices: a less than trustworthy agent and transaction, versus the travel time and long queues involved in making deposits and withdrawals at bank branches a far remove from their village.

A number of solutions are under discussion including better agent training, improved incentives, and shared insurance that helps protect agents’ liquidity risks at lower costs. The real dilemma, of course, is human fallibility. India’s finance ministry has committed to doubling the number of ATMs to 200,000 in every corner of the country by the end of next year, despite the high costs of installation and maintenance, at least in part due to the insoluble problems posed by agent networks.

However, for the foreseeable future, two lakhs worth of ATMs can hardly hope to serve the needs of 1.2 billion citizens, of whom ~41% remain unbanked, according to the Bank of India. Agents, like the poor, will probably always be with us. Better solutions for these last links are important for financial inclusion to move forward and succeed.

Mobile money: Rosy vs real

Most people reading this blog already understand that the headlines trumpeting the advantages and steady gains in moving money around via mobile phones, and even edging out credit/debit cards (The Wall Street Journal , the BBC and Marketing are recent examples), refer to the projected 894 million mobile-banking users of smart phones and tablets—not the simpler feature phones, the ones without 3G or 4G capability and usually without reliable internet access, that the 2.5 billion who have no bank account are far more likely to be using.

Kenya’s M-PESA is of course the notable exception, but Kenya’s regulatory environment is also exceptional, and a surprisingly long list of technical and distribution problems exist behind the poster child’s cheery façade. (For a more thorough understanding of these issues, please see MicroSave’s Riding the M-PESA Rails.)

Meanwhile, the reasons the Samsung Galaxies and iPhones/pads seem to be doing so much better than the un-fancy phones are often ignored. The general supposition in poor, unbanked communities seems to be that the need is there and the numbers are there, so why aren’t more people using phones to send money home, pay bills, save for the dry season, or even just “pet their money”? (Rich or poor, many enjoy constantly monitoring their cash.)

MicroSave has done some useful research on this topic recently and here are some of the findings:

- Afghanistan’s mobile money efforts are hindered by security breaches and poor literacy (many customers can’t read the text messages in the transactions), but in general, women and soldiers—both highly limited in their mobility for different reasons—find loan repayment (female borrowers) and pay deposits (military personnel) to work faster and cheaper via their phones than the taxis, travel time, and other complications imposed by their previous banking methods.

- Abdullah Sawiz, Project Management Specialist, USAID, has more to say on these and other issues in a podcast series sponsored by MicroSave and Mobile Money Gateway.

- Debbie Watkins, a Shore Bank International project manager for bKash in Bangladesh, also participated in this podcast series. Focusing on customer needs, rather than the various and bank and telecom partner directives. Ms. Watkins reminds us that changing habits, even the informal bordering on illegal habits, for customers’ hard-earned, precious cash is never easily accomplished. Without trust and proof of reliability, the features of a bKash mobile wallet are irrelevant to most prospective users. Allowing them to decide what bKash can usefully offer will improve its chances for success.

- A separate CGAP study on remembering PINs in rural Bangladesh also takes the customer perspective on a problem that is widely prevalent in Uganda and other markets as well.

- Mobile Money–Influencers of Success is the source for those of you who want the full spectrum of mobile money offerings around the world (16 services covered), useful detail on the various regulatory environments, and a more comprehensive understanding of service providers (bank, mobile operators, and others) and how they can work together, the technology and the more limited and potentially confusing user-interface issues, distribution, customer value propositions, and the many ways marketing, branding, and incentives have failed or succeeded thus far.

- No discussion of mobile money is complete without a full review of possible fraud techniques, an uncomfortable—and expensive –reality that the service providers for both rich and poor customers must address.

- The GSMA’s Managing the Risk of Mobile Money estimates that the billions of dollars lost each year will continue to harm both reputations and revenues until more rigorous controls are in place. Which is easier said than done. Customer and agent-driven fraud is usually possible to detect and deter over time; the inside jobs perpetrated by employees, systems administrators, and business partners are much more difficult.

Mobile money is still one of the best and brightest hopes for full financial inclusion moving forward. Nevertheless, a bit more caution and realistic assessment of the technical and business issues—and the even more troubling customer hesitation and disenchantment issue- will improve the long-term chances of success.

Can Mobile Banking Deliver on the Promise of Financial Inclusion?

We interviewed Ignacio Mas to find out what he thinks about mobile banking and its role in increasing financial inclusion.

Musings on money: The household money management model of mass market

This research report discusses how behavior is governed by perceptions and aspirations around financial goals, income patterns, and financial instruments. The paper ends with “ten governing rules” that the mass market segment considers intuitively when managing money.

Success Factors of Equity Bank’s Agency Banking

Equity Bank started its agency banking business model in 2010. Since then, the model has become very successful. Currently, the platform has over 2.3 million registered customers with around 80,000 transactions taking place daily through over 6,000 agent outlets. This briefing note, discusses in detail, the key strategic and operational factors behind the success of Equity Bank’s agency banking model.