Technological developments from the Fintech industry are making waves in developing markets and many have the potential to be customized for developing ones also.

Blog

Why Most Agents Networks Will Fail

The Soul of an Agent Network:

The Helix Institute has evaluated and advised all types of agent networks in countries around the world. Big ones, rural ones, new ones, bank ones, and even imaginary inactive ones. Despite the differences in operational strategies, all agent networks should have one element in common – they are crafted to deliver a value proposition to a target market.

That value proposition – the product/service that agents deliver – is the soul of the agent network. It determines the network’s optimal size, growth rate, geographical placement, agent demographics, and the level of training and support that agents receive. It is the foundation upon which all strategic operations are built.

Ironically, despite it being such a defining factor, the value proposition is rarely the issue we are asked to evaluate. Most providers feel like they have got the product right, and remain concerned with secondary issues, such as inactivity in the network, illiquid agents, or a competitor that erodes their market share. However, in our experience, those are generally indicators of larger problems.

Sitting with providers to dissect these problems, we separate the symptoms observed from the drivers that need to be addressed. We unpeel the layers of operations to find elements that have not been correctly woven into the governing strategy. Following these leads frequently guides us to the same place – a value proposition that is simply not very alluring.

An agent network will only ever be as good as the product it delivers. In digital finance, most business models need high volumes to make profits on small margins. Hence, a poor value proposition that is seldom used is going to be a perennial problem. If it does not regularly solve a key concern of the target market, it will constantly struggle to generate income for the business.

Back to the Basics of Product Development

This is not just a problem for small agent networks in the far corners of the world. It is an issue for many of the networks that we evaluate. In our latest paper, Finclusion to Fintech: Fintech Product Development for Low-income Markets, we point out that most of the formal financial products that banks and mobile network operators offer are generally not very useful for low-income people. The resultant uptake and usage speaks volumes:

- Low Registration Rates: The GSMA 2015 State of the Industry Report states that in countries where mobile money is offered, only 10% of mobile connections are linked to mobile money accounts. The 2014 World Bank Findex data shows that only 28% of adults in low-income countries have a formal financial account (bank or mobile money).

- High Inactivity for Those That Register: The 2016 GSMA State of the Industry Report states that only 21% of registered users are active on a 30-day basis. The Making Access Possible (MAP) project studied bank account usage in six countries and found that in one country, 76% of accounts were dormant, while in the other five, 50%–71% of accounts were used as ‘mailboxes’, only to receive an occasional payment.

- For Active, Registered Customers, Usage is Limited and Infrequent: Beyond the statistics shared above on bank accounts, the GSMA 2016 State of the Industry report shares that 97% of volumes and 90.7% of values of mobile money transactions are limited to three usage cases airtime top-ups, P2P transfers, and bill pay. Moreover, the average active user only conducts 2.9 transactions per month (excluding cash-in, cash-out and airtime top-ups).

While lack of access is often touted as the key driver of the low registration rates for formal finance, the inactivity and limited, infrequent usage clearly show that the problem is much greater than just access to these services. In short, most low-income people do not register for formal finance accounts, those that do hardly use them, and those that use them, only do so for limited tasks.

Informal Foundations for Formal Solutions

What is needed is an appropriate set of tools to help people manage their money on a daily basis. Almost nothing we have seen in the market thus far comes close to this. Even when access to formal finance is extended, at best, the mass market incorporates it as yet another tool, but rarely replaces the informal systems and strategies that it uses.

In our paper, Finclusion to Fintech, we compare formal and informal financial solutions and show that the formal ones are not obviously superior as many assume they are. In addition, we review prominent financial inclusion literature and recent data from the Findex and Financial Diaries projects. These help explain why formal financial solutions are not necessarily better, and where product development needs to go to be more valuable for mass-market customers.

The expansion of agent networks across countries has been exciting, but too often the products they deliver are not. New products should avoid trying to improve upon those that people seldom use. They should be built with an understanding that low-income people have unique financial needs and ways of thinking about money management that are still not being met by formal providers. Providers should aim to improve and formalise the often risky informal financial solutions people cling to even when offered formal accounts.

This philosophy should lead the next generation of product development as fintech companies vie to reach the mass-markets of the developing world. Our latest paper is meant to serve as a proverbial Rosetta Stone, translating decades of financial inclusion research into the business opportunities they uncover for fintech innovators. By providing more value for customers, more people would use these products with increased frequency, alleviating many of the most common problems we have seen with agent networks around the world.

View the full report: Finclusion to Fintech: Fintech Product Development for Low-income Markets

Finclusion to Fintech – Product Development for Low-Income Markets

The Helix Institute of Digital Finance is excited to release our new paper by Mike McCaffery and Annabel Schiff, “Finclusion to Fintech” which is designed to help fintech innovators understand the unique money management strategies used by low-income people in the developing world. The paper is aimed to serve as a tool to help fintech providers design appropriate financial products that underserved individuals will want to use on a regular basis. To understand the needs and desires of low-income people, the paper presents detailed insights from 15 years of financial inclusion research, along with the latest industry data. In addition, through illustrative examples, informal money management techniques are compared to formal techniques used by high-income people. To read through the report, please click here.

Interoperability – A Regulatory Perspective

Basis great inputs and discussions from Amrik Heyer, FSD Kenya, Stephen Mwaura former Head of Payments, Central Bank of Kenya, Uma Shankar Paliwal, Former Executive Director, RBI, Dennis Njau, Head of Channels, Kenya Commercial Bank, Gang Chai, Payment Policy Manager, Central Bank of Nigeria and Johnah Nzioki from Eclectics.

In a recent workshop organised by MicroSave’s The Helix Institute, leading DFS industry players including providers, regulators, aggregators, and technology providers, came together to deliberate on innovative ways to address the key challenges facing agent networks. They divided into three groups to look at the key issues in the context of: 1. policy and regulation; 2. strategy and market evolution; 3. operations.

The policy and regulation group noted that:

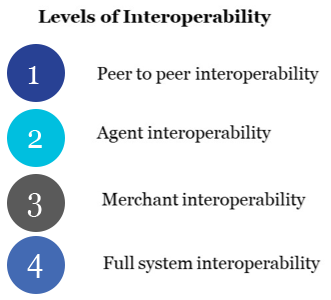

Countries around the world are at different stages of payment system evolution. There are different  levels of interoperability as defined by the Better Than Cash Alliance. From peer to peer interoperability, to agent interoperability, to merchant interoperability and full system interoperability. Peer to peer interoperability sees individual institutions connecting one on one through individual connections; agent interoperability, sees agents able to operate transactions between providers; merchant interoperability where merchants can accept payments form any provider; and full systems interoperability sees institutions, banks, mobile financial service operators or both connecting to a common platform or switch, thereby facilitating transactions.

levels of interoperability as defined by the Better Than Cash Alliance. From peer to peer interoperability, to agent interoperability, to merchant interoperability and full system interoperability. Peer to peer interoperability sees individual institutions connecting one on one through individual connections; agent interoperability, sees agents able to operate transactions between providers; merchant interoperability where merchants can accept payments form any provider; and full systems interoperability sees institutions, banks, mobile financial service operators or both connecting to a common platform or switch, thereby facilitating transactions.

Interoperability offers benefits for the wider ecosystem – these include: wider adoption; higher transaction volumes; and greater velocity of money in the ecosystem. From consumers’ perspective, interoperability means more convenient and efficient services. For regulators and policy makers this translates to reduction in expensive cash in circulation; expansion of the formal financial economy and a direct impact on advancing financial inclusion.

However, countries have different paths to interoperability, driven partly by the circumstances in their market and partly by regulatory philosophy. Some espouse competition on the basis of products and services provided by individual institutions, rather than on channels, which everyone needs to use. This view underpins the shared agent initiative in Uganda, for example. For others like the Better Than Cash Alliance, interoperability is a key aspect payment system evolution.

In the case of Rwanda a national policy on interoperability sought to: create a cash-lite society, encourage financial inclusion, and promote payment system efficiency. The goal for in interoperability was to: improve productive efficiency; increase the customer value proposition to use electronic payments; increase customer convenience; and increase efficiencies due to specialisation in payments. This policy dialogue preceded circulars mandating peer to peer interoperability and work on a national switch for real time micropayments.

Why the rush for interoperability? – especially when some regulators opine that digital financial services is in its infancy and there is a danger in being too prescriptive, whilst the industry is still learning. From a policy maker’s perspective, interoperability facilitates an efficient payment system, as it enables real time micro payments to be made and cleared between any account or any wallet. Subject to the application of Know Your Customer (KYC) requirements it facilitates visibility within financial transactions supporting national and international requirements for Anti Money Laundering (AML) and Combatting the Financing of Terrorism (CFT).

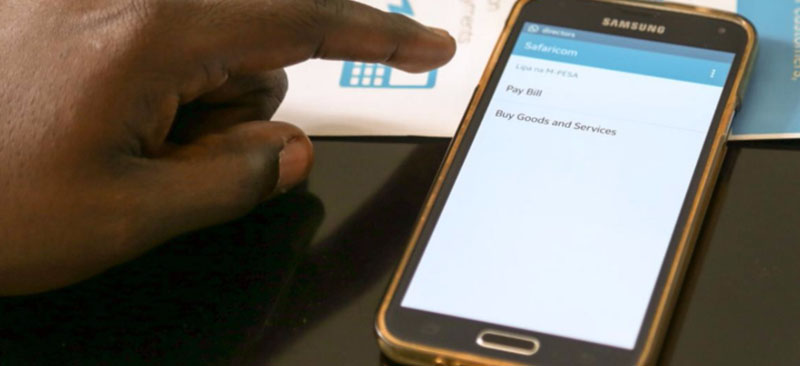

Practically, what difference can it make? In Kenya Safaricom provided widespread peer to peer interoperability with the M-PESA platform, thereby enabling transfers from bank accounts to wallets and in doing so, facilitating the widespread adoption of merchant payments. The Kenya Interbank Transaction Switch (KITS) operated by the Kenya Banker’s Association facilitates real time transfers of up to approximately $10,000, through participating bank accounts. In India through accounts linked to the digital national identity – the Aadhaar and the Unified Payments Interface (UPI) is providing access to financial services for millions through low cost agency operations operated by special purpose payment banks or small finance banks, besides traditional commercial banks. Interoperability combined with digitised information will enable Indians to shop for loans between multiple institutions.

Enabling interoperability is different from having a system which embraces interoperability. This is due to multiple challenges, one of which is pricing. For example, in Uganda it is possible to transfer funds between mobile money providers and to ‘cash out’ across networks. However, few chose to do this directly in part due to high cash-out fees on intra-network transactions.

There is a debate amongst policy makers and regulators on conceptual frameworks for interoperability – whether to use market- or state-based. In Kenya, the regulatory philosophy is for market based interoperability where the market defines the price and there can be multiple providers; hence the provision of services through KITS in addition to most players connecting directly to Safaricom’s M-PESA. In Nigeria, the government stepped in to create the Nigeria Interbank Switch (NIBSS), which it then mandated that institutions should connect to. This was a policy decision influenced by perceived inaction in the marketplace. In India, there are multiple solutions providing interoperability.

Price sensitivity is a factor in some markets. Market leaders often use pricing to stifle competition. Digital finance enables very low-cost transactions, but still in some markets pricing discourages wallet to bank and bank to wallet transactions. This makes it uneconomic, for example, to save small amounts to a bank account through a mobile provider’s wallet.

India shows elements of market and command philosophies; whilst there are several national payment mechanisms, the interchange fees on the switches are kept low to boost interoperability and market acceptance. Policy makers’ desire for a low-cost debit card, which any Indian could use at a fraction of the cost of EMV[1] compliant cards was a factor in the creation by the National Payments Corporation of India (NPCI), of the RuPay card.

From the perspective of financial institutions, market based mechanisms are often preferred especially by market leaders, who can use their market position to influence interchange fees. For a market leader, the commercials around interoperability are often key; they can be reluctant to share their network of agents for example with other institutions because: a) the interchange fee may not be sufficient to facilitate liquidity management and b) due to competitive positioning. Thus, for Kenya Commercial Bank, the fee structure of mVisa made it less attractive as a product for the bank.

A regulator, therefore, must contend with, and balance, policy imperatives for cheap and convenient access, with ensuring sufficient incentives for market based mechanisms to encourage the provision of the infrastructure on which interoperability relies. The challenge is to create an environment where different market players can play to their strengths and respond to the unique characteristics of the country they operate in, which can include widely disbursed populations such as in Tanzania or Zambia.

In the words of one regulator “Retail payments are dynamic – the regulator needs to provide space for this dynamism and for different actors to play a role, over time this will reduce costs”.

*Interoperability means a set of arrangements, procedures and standards that allow participants in different payment schemes to conduct and settle payments across systems while continuing to operate also in their own respective systems. Definition by CPSS

[1] EuroCard, MasterCard, Visa (EMV), a defacto standard in the payments industry

Progress and Challenges with KYC and Digital ID

Based on great inputs and discussions from Amrik Heyer, FSD Kenya, Stephen Mwaura, former Head of Payments, Central Bank of Kenya, Uma Shankar Paliwal, Former Executive Director, RBI, Dennis Njau, Head of Channels, Kenya Commercial Bank, Gang Chai, Payment Policy Manager, Central Bank of Nigeria, and Johnah Nzioki from Eclectics.

“Identification provides a foundation for other rights and gives a voice to the voiceless.” – Makhtar Diop, World Bank Vice President for Africa

At a recent workshop organised by The Helix Institute, leading DFS industry players, including providers, regulators, aggregators, and technology providers, came together to deliberate on innovative ways of addressing the key challenges that face agent networks. They split up into three groups to look at the key issues in the context of 1) policy and regulation, 2) strategy and market evolution, and 3) operations.

This blog post details observations from the policy and regulation group, as listed in the following section.

Digital Financial Services has Driven Financial Inclusion

Premised on digital and mobile solutions, Digital Financial Services (DFS) has transformed the landscape of the financial sector. It has brought about increased efficiency, convenience, and consumer options. DFS has increased access to financial services for a population that has hitherto been financially excluded. As per GSMA’s 2016 State of the Industry Report-Decade Edition, there are 500 million registered mobile money accounts globally, of which 118 million are active (on the basis of at least one transaction in 30 days). The number of active mobile money agents (on the same basis) stands at 2.3 million.

Large Numbers Still Lack KYC Compliant Identification

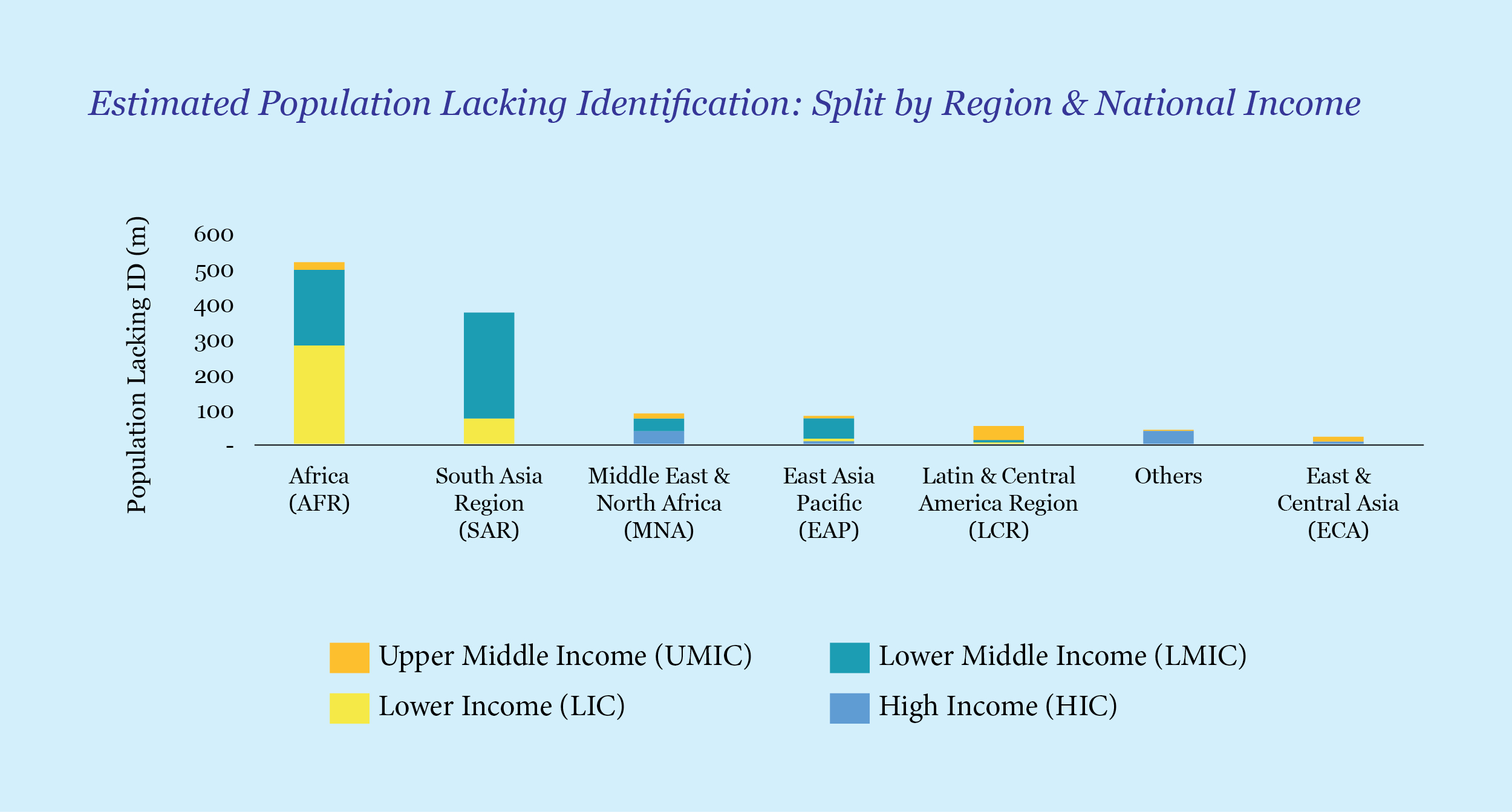

Historically, opening a bank account in many markets has proved to be a challenge due to Know Your Customer (KYC) guidelines, which require proof of identity and address. Unbanked groups often suffer disproportionately as a result of their inability to offer proof of identity. Such identification is generally based on birth certificates and passports, and proof of address based on utility bill payments. Over a billion (17.7 %) of the world’s population [1] remain unable to meet official KYC requirements. The World Bank ID4D 2017 Global data set shows the estimated population that lack identification, as seen in the adjoining graph.

Lack of KYC Compliance Excludes People from Accessing Formal Financial Services

Lack of KYC Compliance Excludes People from Accessing Formal Financial Services

People who fail to meet KYC requirements are excluded from accessing formal financial services, including savings accounts, loans, remittances, insurance, and pensions, among others. However, the problem goes deeper, and often such people are unable to digitally receive benefits from the government, including payments for social security, basic health care, and primary and secondary education. Lack of identification also prevents them from receiving international remittance through formal channels.

Lack of KYC Compliance Impedes Mobile Money and Agent Banking

Volume is the main factor that drives the business-case for institutions that offer digital financial services. This means that providers must increase their customer base and focus on onboarding large numbers of new customers – a process that becomes easier if simple and effective ways to satisfy KYC requirements are introduced.

KYC Acts as a Multipurpose Enabler

Conversely, the existence of KYC-compliant documentation that enables efficient onboarding of customers can have a number of enabling effects. These include a) facilitating mechanisms that may not require a branch, b) allowing harmonisation of government databases for Government-to-Person (G2P) payments, c) enabling transaction mechanisms that do not require signatures, and d) facilitating access to tailor-made financial services suited to a range of customer groups.

Identity Comes in Several Forms

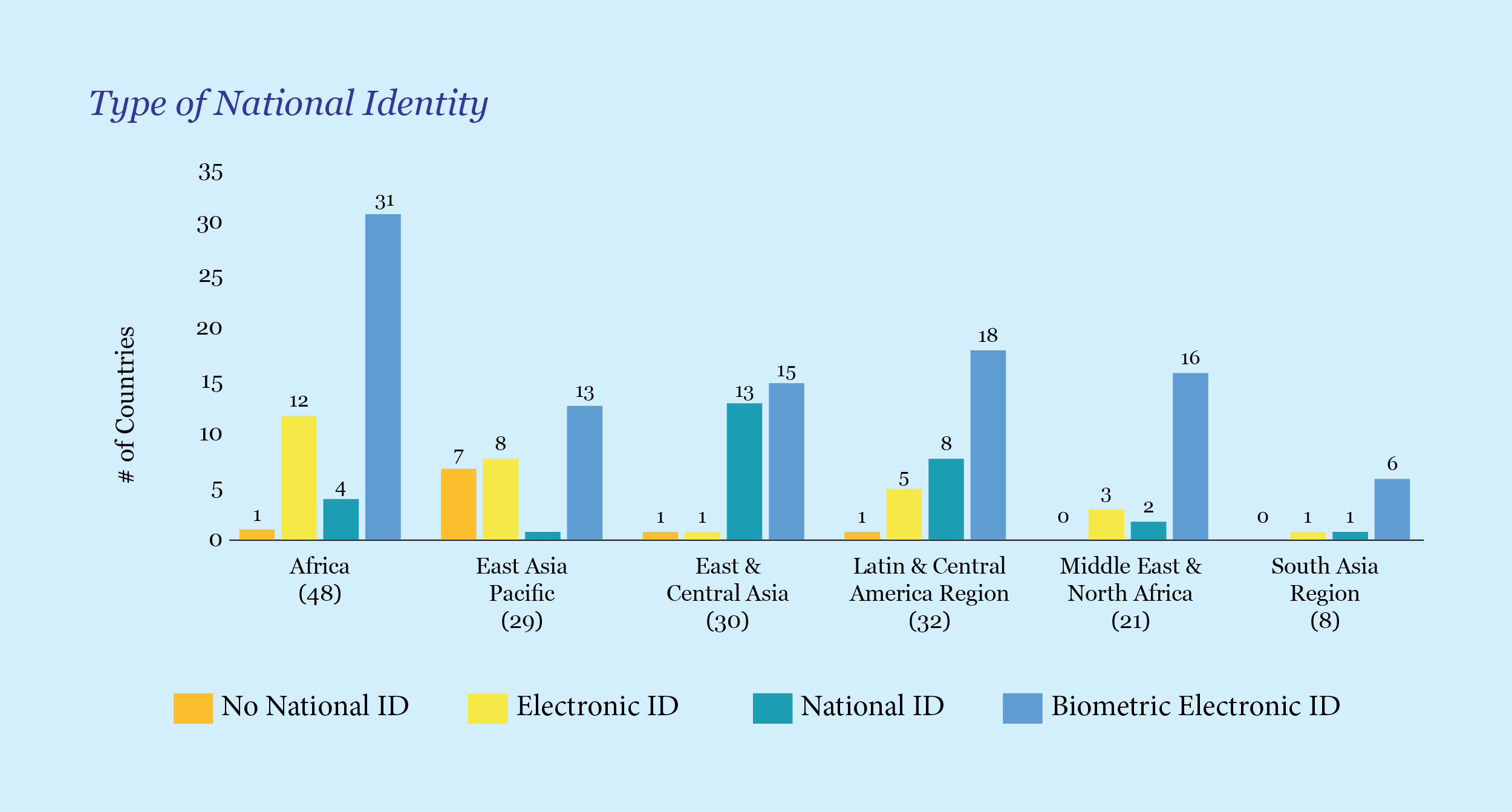

The World Bank ID4D 2016 data set (see adjoining graph) indicates the progress of national identity card systems of various countries and regions as per the World Bank Group’s Identification for Development initiative.

Digital forms of identification are gradually replacing paper-based national identification documents. Electronic ID is a form of identification that can be used for online or offline identification purposes, often in the form of a photo-card with an embedded chip that contains information. A biometric electronic ID adds another layer of identification, usually based on fingerprints. In this context, it is useful to note that a few countries still lack a system of national identity. These are usually countries in conflict.

Digital forms of identification are gradually replacing paper-based national identification documents. Electronic ID is a form of identification that can be used for online or offline identification purposes, often in the form of a photo-card with an embedded chip that contains information. A biometric electronic ID adds another layer of identification, usually based on fingerprints. In this context, it is useful to note that a few countries still lack a system of national identity. These are usually countries in conflict.

The KYC Journey Often Starts with Simplified KYC Requirements

In most markets, subscribing to mobile money is easier than opening a bank account. The required level of KYC varies between mobile money and bank accounts. Higher levels of KYC are usually required for opening bank accounts due to the higher transactional value and volumes, as well as nature of banking products. This is a key reason for the growth of mobile money when compared to agent banking in many markets.

Simplified KYC can Enable Limited Access for Large Populations

Countries without national identification have sometimes introduced simplified KYC guidelines to enhance financial inclusion. This includes restrictions on transaction values (deposits/withdrawals/transfers) to mitigate anti-money laundering (AML) risks. In such cases, if customers wish to upgrade from a simplified KYC account, they need to provide full KYC-compliant documentation to their financial institution.

Pradhan Mantri Jan-Dhan Yojana (PMJDY), India’s national mission for financial inclusion, ensures access to financial services through simplified KYC requirements. In almost three years, 290 million accounts have been opened under the scheme, with 60% of accounts in rural and semi-urban areas. These accounts hold USD 9.9 billion worth of savings, which translates to an average balance of USD 34.

The financial Sector may Create Financial Identity, but It Would Likely be Insufficient

Challenges in the rollout of national identification forced the Nigerian banking sector to provide all banked customers with a Bank Verification Number (BVN). Enrolment of BVN involves capturing a customer’s details, including fingerprint and facial image, after which a BVN is generated. The BVN is expected to minimise the incidence of fraud and money-laundering in the financial system and enhance financial inclusion. Prior to the introduction of national identity, Bank of Uganda mandated the Credit Reference Bureau (CRB) to create a financial identity card and to link to CRB. After signing up an initial 900,000 customers, 150,000 customers were being added annually. As it turned out, the financial identity card in Uganda was not sufficient, nor was it designed to drive financial inclusion [2].

Simplified KYC and/or Financial Sector Identification is Often a Stage in the Path to Full Financial Access

Mobile money with simplified KYC is an effective way to on-board large numbers of customers. However, in more mature DFS markets, there has been a high demand for facilitating mobile phone-based access to full banking services.

Mobile money with simplified KYC is an effective way to on-board large numbers of customers. However, in more mature DFS markets, there has been a high demand for facilitating mobile phone-based access to full banking services.

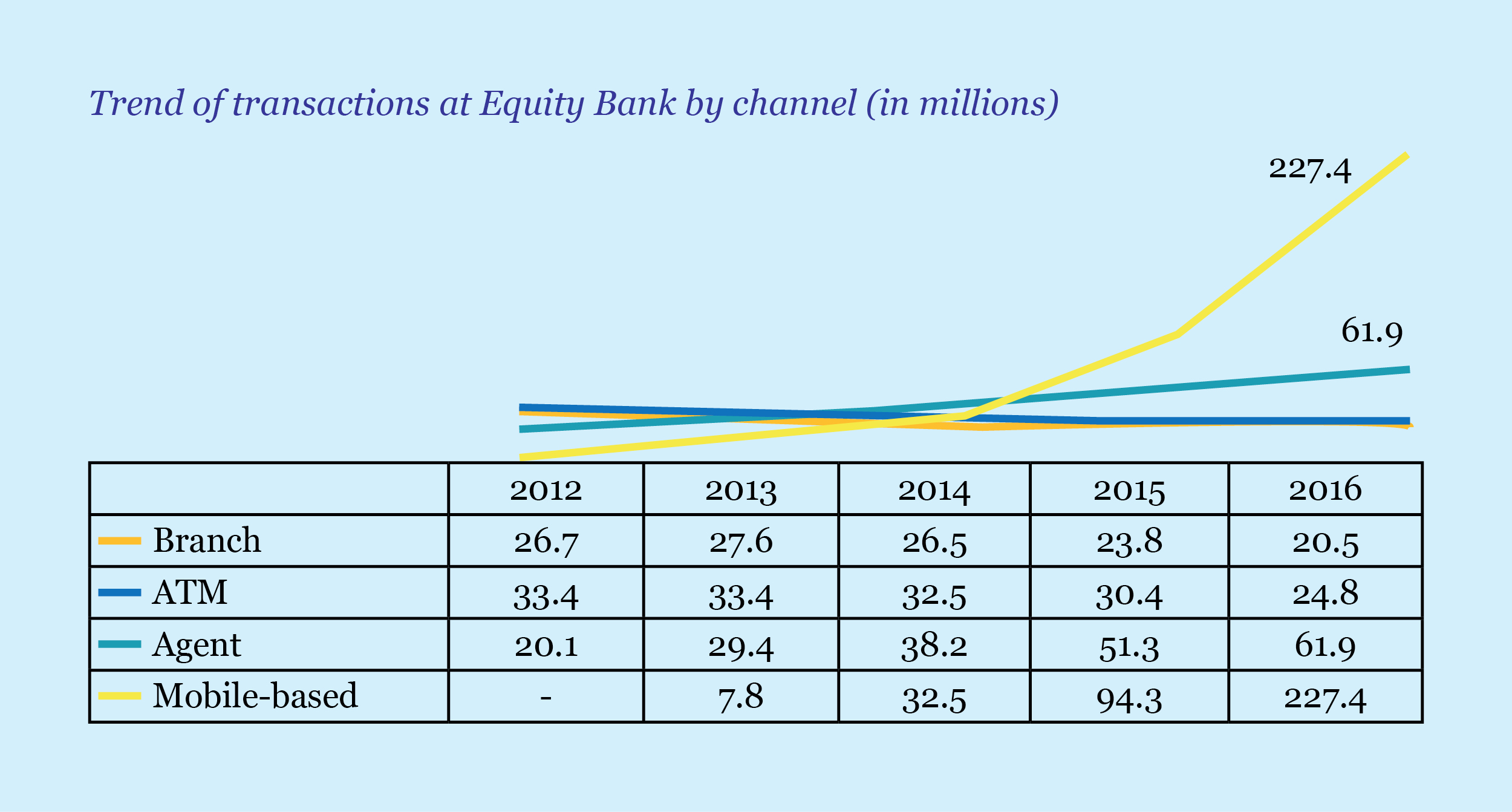

Equity Bank in Kenya has observed that customers conduct more than double the number of transactions at agents when compared to transactions at the bank branch and ATMs, while self-initiated transactions conducted on customers’ mobile devices amount to four times those made at agents.

Meeting KYC Requirements is a Particular Challenge for Refugee Populations

By the end of 2015, war, conflicts, and natural disasters had forcefully displaced an unprecedented 65 million [3] people around the world. Refugees and displaced populations face great challenges in obtaining formal identity and proof of residence, and often fail to meet KYC requirements. A few countries, including Egypt, Zambia, and Uganda, have allowed refugees to open mobile wallets using government attestation cards or through UN refugee registration cards issued by UNHCR. However, regulators report that providing identification to refugees needs careful application due to Anti Money Laundering and Combating the Financing of Terrorism regulations and acts.

Fragmentation of Records Pose Challenges to Digitising Identity

For many governments, the evolution from paper-based identity to digital identity proves challenging. It requires a huge capital investment to create a national database and to remove duplicate records from multiple existing databases so that there is a single identification number per individual.

Digital Identification can Facilitate Rapid On-boarding and Competition among Providers

Access to national identification databases varies from country to country. Yet, the drive for financial inclusion requires regulated financial institutions to be able to avail digital access for free or for a low fee. Government and private institutions in Kenya have been progressing with an Integrated Population Registration System (IPRS), a central database to verify the identity of a citizen and residents. Commercial banks, telecommunications companies, and other institutions are digitally linked to the National Population Register of the IPRS and have been using this information for efficient customer on-boarding.

Given that on-boarding customers is easier with digital identification, competition can be facilitated by removing barriers, not only to on-boarding but also to the movement of customers. For instance, in India, the IndiaStack API has been designed to use unique digital infrastructure that links a biometric identity (known as Aadhaar) combined with a digital locker that contains customer documents and certificates, to enable banks to provide competing loan offers to potential customers without submitting any physical documents.

Is there a Balance between Customer Protection/Privacy and Data Sharing of Digital Identification?

In the cases where governments have allowed public and private institutions to access the digital ID database, it is important to decide the extent of information that should be shared with various institutions. Such information ranges from complete details about the individual, including full KYC, to top-level verification that safeguards the privacy of citizens. For instance, in India, the government has not limited Aadhaar to being a means of identification to deliver government subsidies and services alone. Private agencies like financial institutions or telecom companies can use Aadhaar for the purpose of electronic KYC, which replaces the physical proof of identity/proof of address documents. Private players may also use Aadhaar to authenticate transactions based on biometrics. In other words, in the federated structure, the demographic data including biometrics reside with the government agency. Other agencies, including private ones, are allowed to fetch the required demographic data for KYC and biometric match-based confirmation to authenticate transactions on a real-time basis.

Conclusion

Digital identity and KYC, including tiered KYC, are vital components to on-board large numbers of unbanked and under-banked people to mobile money accounts and bank accounts in a rapid, cost-effective manner. With large populations possessing a digital account, and with digital identity being accessed by the government and financial and payment sectors, there is a distinct possibility that G2P payments, merchant payments, and technology-enabled financial services will show rapid evolution worldwide.

[1] The World Bank Group’s Identification for Development (ID4D) initiative

[2] Based on a presentation to the Alliance for Financial Inclusion

[3] UNHCR 2016

A Strategic Approach for Next-Generation DFS Agent Networks

With special thanks and acknowledgement to Abhinav Sinha (EKO India), Tamara Cook (FSD Kenya), Kwame Oppong (CGAP), Paul Mbugua (Eclectics), Paul Musoke (FSD Africa), and Abigail Komu (Independent Consultant).

Some people may argue that agent networks will soon go extinct. Even if that is the case, it will not happen until long into the future. In our opinion, agents in the developing world, where about 75% of the unbanked populations live, will remain the core bridges between cash and digital value. Agent network management, however, remains the most operationally burdensome and, at between 40–80% of business revenue, costly element of the digital financial service (DFS) value chain.

On 23rd June 2017, MicroSave wrapped up its four-year expedition, namely the ‘Agent Network Accelerator Programme’ (ANA) with a day-long workshop held in Nairobi. Industry experts and representatives of various stakeholder institutions across the globe came to deliberate on the lessons learnt over the years and discuss the next generation of agent models.

From the surveys conducted by The Helix Institute, including the nationally representative ANA surveys, it is clear that most financial service providers now understand the key challenges to agent network management, as well as their ultimate obligation to move beyond the role of agents as bridges. Providers should be designing strategies that take market evolution into consideration. On the demand side, the needs, preferences, and perceptions of customers are changing. Meanwhile, on the supply side, it is increasingly becoming vital to manage costs while providing services to all market segments efficiently.

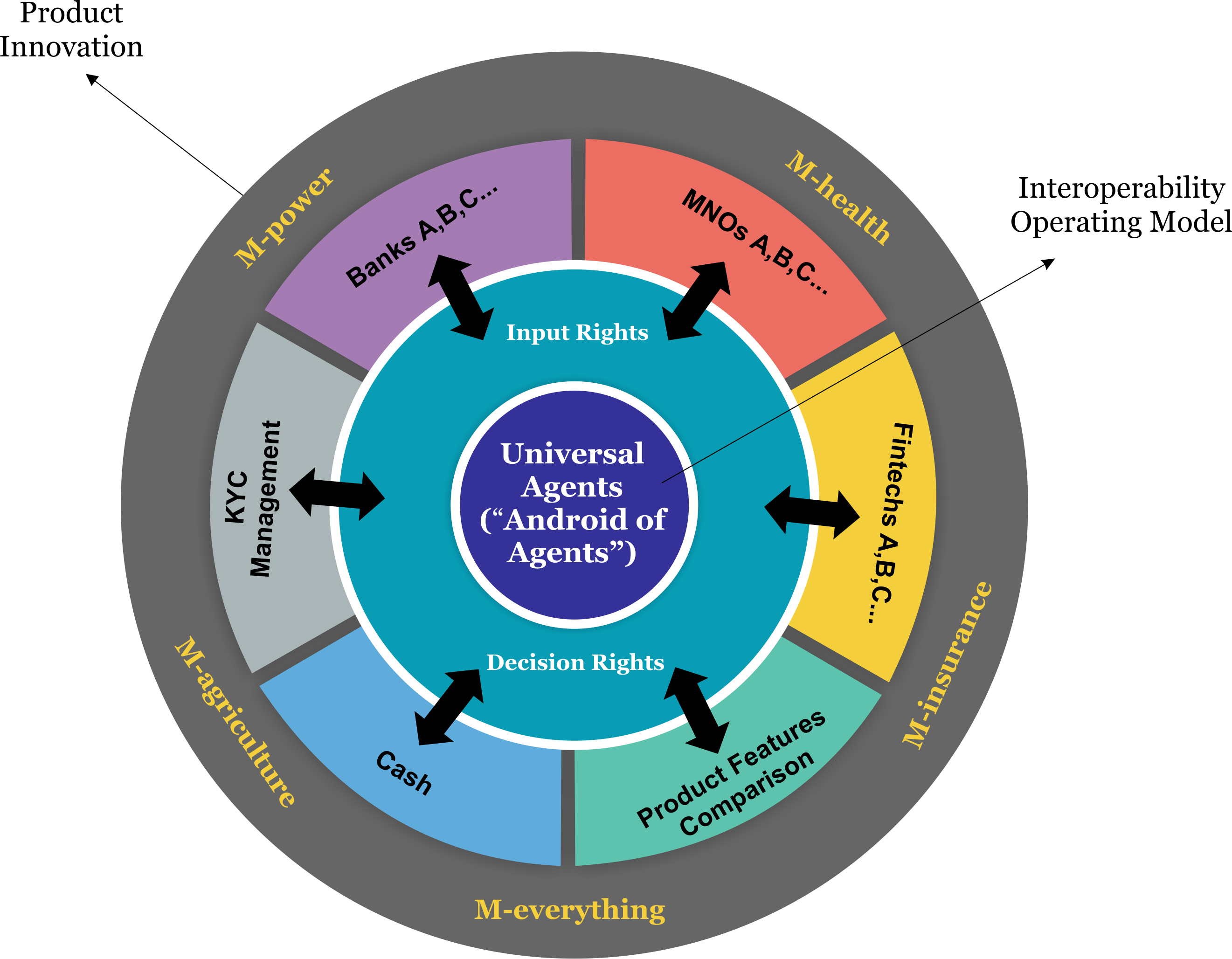

The workshop in Nairobi identified two critical elements that form the basis of future-proof agent network deployment strategies. These two elements – interoperability and innovation – ensure sustainable agent models that are able to respond to rapidly changing business environments.

Interoperability

As long ago as 2012, industry experts identified an open and fully interoperable market as the future. A lot of writings have focussed on interoperability and its benefits. Yet here, at the axis of interoperability lies the “android of agents”, or a universal agent. What this means is that industry players should serve customers through a shared agent network. Thus, banks, mobile network operators, and third-party fintech entities would all share a universal agent. This universal agent does not need to hold separate e-values for each client, unlike most non-exclusive agents today. At the core of the universal agent’s services is a comparison of the products and services from the different players, which creates a more transparent market and allows customers to easily access information.

On the supply side of the ecosystem, a unified platform would help customers access financial services from anyone who wishes to offer them. Shared agents and a unified e-currency will allow providers to focus on offering relevant products and not on building expensive agent networks or channels that eat into their bottom line.

On the supply side of the ecosystem, a unified platform would help customers access financial services from anyone who wishes to offer them. Shared agents and a unified e-currency will allow providers to focus on offering relevant products and not on building expensive agent networks or channels that eat into their bottom line.

On the demand side, customers are increasingly changing and are beginning to look beyond the available products. They are keen to avail premium services that go with product delivery. There has been a revolution in financial services, as it has evolved to mobile, wearable devices, and the Internet of Things (IOT). Customer expectations from financial service providers have evolved as well. Now, more than half of consumer bank interactions take place through online or mobile channels.

A recent report by Accenture identified a number of factors that have brought about change in the digital finance landscape. The report notes that consumers are increasingly willing to share more of their personal data in anticipation of benefits from providers. Digital platforms attract younger consumers as an alternative for accessing financial services, while more customers are starting to accept automated support services. In the light of such trends, financial service providers have to engage in constant innovation and develop novel products and services to survive.

The players behind the universal agent described above collectively create the ‘finance store’. Providers, therefore, compete in terms of product and not channel. Customers then assess what is available at the universal agent points, where they choose their own products and use-cases.

Providers have been building expensive distribution networks, and often struggle to keep up as customers’ needs evolve to demand easier and quicker access. It is therefore wise to focus on the product offering and share agent channels to respond to changing demand quickly.

| The workshop experts see the potential of an amalgamation of industries, which enable institutions to work together and provide value-added services to basic financial provisions. For the low-income segments, let us consider the basic human needs of food, shelter, and clothing. How are customers spending to meet these requirements? How can financial service providers partner with entities in these sectors to create value-added products and services, and make their offerings relevant to the populace? On considering other higher income segments, what extras beyond the basic requirements do customers spend on? What other value-added services can be created? The answers to these questions will inform the strategies of financial services for the future business case of the agents.

A good example of this amalgamation is how digital financial services have been transforming agriculture (m-agric). Laying down the necessary digital payment structures in agriculture is important to improve the sector. When this is achieved, subsequent growth of other components of financial services will be realised. One such component is access to credit, which is fundamental to agriculture value chains. Example: Umati Capital (UCAP) in Kenya Umati Capital is a non-bank financial intermediary that focusses on the provision of supply chain finance across various value chains. They leverage technology to provide financing to SMEs who supply to their corporate trading partners. Umati Capital seeks to address two key problems for its identified customer segments: • Access to working capital for small business suppliers of medium and large-sized corporates; • Provision of a supplier financing programme that is tailored to the supplier’s payment cycles. Currently engaged in the dairy sector in Kenya, UCAP uses technology to make faster lending decisions. With funds from angel investors, UCAP has set up mobile applications throughout each stage of the value chain to capture data and inform their disbursal of smallholder farmer loans via mobile wallets. UCAP has currently been running a pilot with 320 dairy farmers. The results are promising and Umati Capital has plans to scale up two major processors to reach 200,000 dairy farmers. |

Innovation

Providers need rapid innovation to respond to the changing demands of consumers. In the future, providers will need to continue prioritising innovation. They must deliver financial services that respond to the market’s needs and mental models for money management, and thus have a real social impact.

Innovation that is driven by the amalgamation of industries has already begun with m-agric, m-health, m‑water, m-power, etc. But it is yet to scale due to the lack of data-sharing and analytics that could potentially make the services relevant to their customers’ everyday lives. This is crucial and should be considered to create more digital use-cases for customers. The ‘universal agent model’ will create a richer data pool, where identifying the 5Vs of data (value, volume, velocity, veracity, and variety) will enhance the continued innovation of products. Product innovation that focusses on meeting customer demands will be essential to sustain the agent network and safeguard agent viability.

How do we ensure provider buy-in?

It is evident that a lot is to be gained through these types of strategies for the future. These gains include, among others, new products, higher quality, less-costly agent networks, improved liquidity management, money that remains digital in the ecosystem, new customers, and new use-cases.

However, there are some impediments to adoption by financial service providers, as outlined in the following section.

1: Sunk Costs: Many providers have made large investments in the form of expenses, time, and effort in legacy systems or distribution models. How can they now put that aside and become open to sharing? Understandably, the providers would be keen to reap the rewards from existing systems and agent networks before entering the coopetition (collaborating while competing) arena. In fact, many providers see their agent networks as a key source of competitive advantage. This will be a question of timing and nature of the market. Yet, as the market ultimately evolves, attempts to hold on to the past will only ensure their obsolescence. As the future unfolds, the platforms and distribution networks of providers are expected to become increasingly irrelevant.

2: Time Horizon: As GSMA has pointed out, both significant investments and serious intent are required to ensure that mobile money systems flourish and yield profits. Indeed, this is the key differentiator between mobile money deployments that ‘sprint’ and those that ‘limp’. But many providers already under-invest in a business that calls for large-scale upfront as well as ongoing investments to achieve scale and succeed. So it is fair to assume that many providers will hesitate to embrace further investment in the future because they anticipate long break-even periods. In this case, it is ideal to see things from a collective perspective – considering multiple entities/providers – where there would be a merger of volumes from the combined customer base, combined transactions numbers, etc. The break-even ball game would change from being linear, where a provider hopes to make profits after a period of time from expected transactions for a single source, to a stage where the provider makes profits from parallel sources due to partnerships. An instance of this is the monies raised from opening APIs, where there is a technological cost to every API call.

3: Risks: Providers are likely to express concerns about unforeseen or expected new risks that would arise through the coopetition model. However, there is a need to embrace risk to design robust mitigation strategies to provide financial services. It calls for collectively identifying and documenting risks as and when they occur, as a measure of planning against future occurrences. Indeed, the coopetition model is likely to facilitate sharing information and integrating systems to better mitigate risk. Fearing risk will simply inhibit innovation as the market evolves.

Conclusion

Is it possible to begin developing tomorrow’s distribution network today? How do we develop deployments that enable and facilitate the demand and supply equilibrium? The solution lies in finding that equilibrium. This can be explored by enabling a single e-currency to serve multiple financial services, developing a real-time self-initiated request platform for customers, encouraging innovation and coopetition, and aiming at social impact for daily relevance. The future starts tomorrow!01