One of the most common reasons for declining agricultural productivity is deteriorating soil quality due to over-use of chemical fertilisers which are easily available at subsidised rates. The Government of India introduced Soil Health Cards (SHC) for farmers in 2016 under the National Mission for Sustainable Agriculture to promote judicious use of fertilisers amongst the farming community.

Blog

Designing User-Friendly USSD Interface for Digital Financial Services

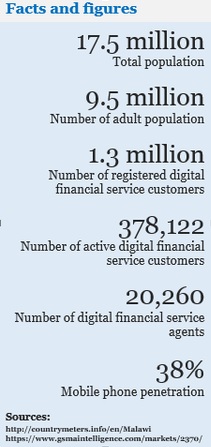

According to Finscope 2014, it is estimated that 33% of Malawians have access to formal financial services. For any non-urban individual in Malawi, travelling to the nearest bank takes an average of more than an hour and a quarter. By contrast, 50% of adult Malawians have access to a mobile phone, 20% are aware about mobile money, and 4% actually use mobile money account. The high rate of access to mobile phones provides an immense opportunity to Digital Financial Service (DFS) providers to offer a diverse range of formal financial services to unbanked Malawians.

For any customer segment, there can be multiple criteria for availing financial services. While some of the criteria, such as product features, channel accessibility, network connectivity, and usage charges have a certain role in the uptake of DFS, the User Interface (UI) plays a more important role than is envisaged by DFS providers. UI plays an integral part in enhancing customer experience and facilitating regular usage of mobile money wallets.

Globally, DFS providers offer their products and services on different access channels such as Unstructured Supplementary Service Data (USSD), SIM toolkit (STK), Interactive Voice Response (IVR), mobile applications and the internet. In the current scenario, USSD (in addition to mobile applications) is one of the most convenient and best available options for reaching the mass market in a cost-effective way. Preference for any channel, however, varies across geographies depending on key factors such as literacy level of users, service offerings, availability of and accessibility to alternative service providers, and ease of use, among others.

When mobile money was launched in Malawi, customers could access their account only through an STK menu. In 2013, however, a leading mobile money provider started offering its services over USSD as well. MicroSave’s market research, funded by UNCDF’s Mobile Money for the Poor (MM4P) programme, highlights that contrary to the popular perception, most users in Malawi have a higher preference for the USSD access channel when compared to STK.

This note focuses on key user insights explaining the preference for USSD, which should remain the core focus area for providers while designing the interface of their access channel.

Key Findings

During the course of our study and also working with other providers in Malawi, we noted that self-use of mobile money accounts was common across the country, especially among young people and the working class, more prominently among men. Although agent assisted transactions / over-the-counter (OTC) services in Malawi are commonplace, our research shows that it is not as prevalent as in countries such as Uganda (30%) and Zambia (67%). Most users have learnt how to use mobile money on their own. This, to a large extent, can possibly be attributed to USSD channel’s intuitive UI, familiarity with easy-to-interpret menu content and simple navigation through menus. Apart from the UI, there are two more compelling factors which drive the preference for USSD channel among customers:

During the course of our study and also working with other providers in Malawi, we noted that self-use of mobile money accounts was common across the country, especially among young people and the working class, more prominently among men. Although agent assisted transactions / over-the-counter (OTC) services in Malawi are commonplace, our research shows that it is not as prevalent as in countries such as Uganda (30%) and Zambia (67%). Most users have learnt how to use mobile money on their own. This, to a large extent, can possibly be attributed to USSD channel’s intuitive UI, familiarity with easy-to-interpret menu content and simple navigation through menus. Apart from the UI, there are two more compelling factors which drive the preference for USSD channel among customers:

- Past behaviour of users accessing a service on phone, such as self-airtime top-up using USSD channel, results in rapid uptake of mobile money usage;

- Robust technology provides positive experience to mobile money users.

It should be noted that unbundled menus are a design feature, and may not actually be an advantage specific to USSD. An unbundled menu may have negative implications as well. For instance, novice and occasional users may find it challenging to navigate to the required option as the probability of a session time-out increases with a more detailed menu.

1. Extension of Status Quo Behaviour

Unlike countries like India, where agents electronically top-up airtime for customers, airtime scratch cards seem to be the most preferred mode of self-top up among Malawi’s growing base of mobile subscribers.

Unlike countries like India, where agents electronically top-up airtime for customers, airtime scratch cards seem to be the most preferred mode of self-top up among Malawi’s growing base of mobile subscribers.

These prepaid users, both semi-literate and illiterate, are not only numerate; but are also familiar with the USSD channel which they frequently use for airtime top-up (i.e., they top-up airtime by entering the scratch card number using a USSD short code such as *XXX*1234 1234 1234#). Starting mobile money USSD sessions and entering numeric responses are not new for these users, but rather an extension of their conventional practice for airtime top-ups. Eventually, these users become confident of accessing their mobile money accounts over the USSD channel.

2. Quick Access to Sessions and Fast Response Time

USSD is simple and easy to use. The user dials a short code *XXX#, presses the call button on the mobile phone and starts interacting with the platform. USSD provides fast access to mobile money menus.

USSD is session based and the system’s response time between an action point and the user’s response is usually fast. In addition, depending on the provider, users have less time during USSD sessions, compared to STK or other UIs, to input their responses and prevent a session drop-out. This, of course, acts as a major deterrent for novice users. Experienced users, however, are familiar with the channel and complete their transactions quickly while using USSD menus. The users also do not need to wait for any text message confirming their transaction status as such communication is received immediately through flash messages.

3. Easy to Recognise Network Downtime

USSD establishes a real-time connection with servers at the back-end and allows true session-based communication. Compared to STK, where users become conscious of network failure at a much later stage after entering responses, USSD users become quickly aware of session drop-outs and hence, can re-initiate the USSD session much earlier than the STK platform.

4. User Friendly Design, Detailed Menu, and Easy Navigation

In multiple blogs, MicroSave has categorised USSD menus as bundled and unbundled. A bundled menu has limited options in the main menu and requires further navigation to explore sub-menu options. The unbundled menu however, is more detailed with a list of various options in the main menu itself. The research found that this detailed menu is commonly preferred by mobile money users in Malawi. The inclination towards USSD is primarily due to the availability of detailed menus and the preferred use-cases being placed at the beginning of the main menu such as money transfer and airtime purchase. This enables users to easily locate their preferred options and complete their transaction without navigating through multiple menus. Furthermore, users find the menu content to be simple, uniform and easy to interpret.

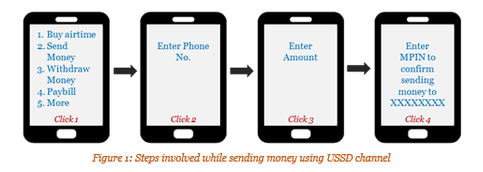

This helps users to complete most transactions with just four to five ‘clicks’ (See figure 1). Eventually, most users complete their transactions within a minute of initiating the USSD sessions.

It should be noted that unbundled menus are a design feature, and may not actually be an advantage specific to USSD. An unbundled menu may have negative implications as well. For instance, novice and occasional users may find it challenging to navigate to the required option as the probability of a session time-out increases with a more detailed menu.

5. Easy and Consistent Menus for Bill Payments

Access to electricity is limited to a few Malawians only but it is used extensively wherever available. Paying electricity bills at dedicated bill payment centres, however, is time-taking due to limited availability and inaccessibility. For these users, mostly based in urban/semi-urban locations, paying electricity bills using mobile money service offers much convenience. The fact that there is an option of paying utility bills without prohibitive service charges has also encouraged customers to use their mobile money accounts for such services.

Access to electricity is limited to a few Malawians only but it is used extensively wherever available. Paying electricity bills at dedicated bill payment centres, however, is time-taking due to limited availability and inaccessibility. For these users, mostly based in urban/semi-urban locations, paying electricity bills using mobile money service offers much convenience. The fact that there is an option of paying utility bills without prohibitive service charges has also encouraged customers to use their mobile money accounts for such services.

Additionally, users find it easier to navigate other bill payment menus as they find similar sub-menus while paying for television subscriptions and other payments. For instance, to make a bill payment, a user has to select the type of bill payment, select the payee, enter the amount, customer ID and the MPIN as depicted in figure 2.

Conclusion

Overall, the research finds that most customers are aware of the convenience associated with mobile money services. This primarily includes storing money to avoid cash holding risk, transferring money on their own, the convenience of airtime top-up and paying utility bills anytime and anywhere, among others. Simplified USSD interface and convenience to use mobile money services are the major factors leading to higher uptake and regular usage of mobile money, reduced dependence on agents for transactions and increased self-usage of mobile money accounts by customers.

Overall, the research finds that most customers are aware of the convenience associated with mobile money services. This primarily includes storing money to avoid cash holding risk, transferring money on their own, the convenience of airtime top-up and paying utility bills anytime and anywhere, among others. Simplified USSD interface and convenience to use mobile money services are the major factors leading to higher uptake and regular usage of mobile money, reduced dependence on agents for transactions and increased self-usage of mobile money accounts by customers.

So, when most mobile money operators in Malawi continue to invest in furthering their operations, particularly in rural geographies, they should bear in mind that nothing beats the convenience and simplicity of use offered by mobile money as well as realise the importance of user interface in enabling a positive user experience. Fortunately, USSD interface scores high on both these key elements. It may not be incorrect to mention that a positive user experience is likely to define the uptake and success of mobile money in Malawi

Digital Financial Services in Bangladesh

Bangladesh’s digital financial services have been much in discussion for rapid growth. Six years since inception – where the market is heading to? What providers ought be doing. This and much more in this video where MSC expert, Akhand Tiwari, talks candidly on the critical role regulation and behavioural sciences will play in shaping the future of mobile banking in Bangladesh.

Do Financial Service Providers Really Understand Savings Group Members?

The 2016 State of Linkage Report found that 40% of financial service providers (FSPs) currently providing savings and credit products to savings groups (SGs) worldwide are in Kenya, Tanzania and Uganda. With an estimated combined SG population of 3.5 million, FSPs in these three countries may recognise the potential of this market – but how much do they understand about the needs and perspectives of the people they are aiming to reach?

FSPs can gain useful insights from some new perspectives from SGs (both linked and unlinked to banks). These were gathered through rapid small-scale demand-side studies in Ghana, Tanzania and Zambia carried out by Savings at the Frontier (SatF); and from feedback given by women belonging to Village Savings and Loans Associations (VSLAs) in Kenya during the East Africa Savings Group Linkage Summit organised by CARE East and Central Africa in December 2016.

Why do people join saving groups?

The strongest incentive for linking with formal FSPs for all the SG members interviewed for the SatF studies is the increased security of their cash. In Ghana, we heard about an SG treasurer who found a note under her door saying that she was going to be robbed. She rushed out and buried the cash box in a nearby field, terrified but thankfully not robbed. Similarly, one of the Kenyan VSLA members referred to storing “up to US$ 4,000 under the bed.” The fear and terrifying experience of potential loss of hard earned cash is an important driver towards formal banking among SG members.

Another incentive for SG members interviewed by the SatF team was earning interest on surplus savings. However, we encountered a lack of knowledge – and thus confusion – resulting from the way groups calculate interest on a monthly basis, compared to banks who do it annually.

The SatF country studies found that simply being members of a group enhanced savings discipline. Similarly, the Kenyan VSLA members reported that linkage helped to improve savings discipline, which in turn supported members to better plan for their futures.

Why don’t savings group members currently use banks?

In the three SatF country studies, SG members reported that they did not use banks because they did not think they had enough money to save. Bank bureaucracy was also seen as a major hurdle when directly compared to SGs’ simpler procedures. Similarly, the Kenyan VSLA members referred to “too much paperwork” putting them off using banks.

In Ghana, we found that physical access to banks was more difficult than in Tanzania and Zambia. Access remains a major challenge in reaching SG members who tend to be far removed from banking networks. A further hurdle is a lack of knowledge about formal products and services.

The women we spoke to in Kenya identified the following other linkage-related challenges:

- Worries about fees and deductions when savings were held in a bank;

- Confidence in mobile banking was undermined by poor network coverage and connectivity;

- Groups that didn’t access bank accounts through mobile agents had to travel quite a distance to reach a branch;

- Limitations on youth (i.e. under 18s) being included in linkage banking as they lacked ID cards; banks need these to meet Know-Your- Customer (KYC) requirements;

- Technology, including mobile money, can be a challenge for older group members and illiterate members; and

- Some group members were still wary of dealing in anything other than cash.

Technology as an Enabler

Technology will continue to be an important enabler of linkage. Access to mobile phones is prevalent in all three SatF study countries. However, registration for mobile money varies widely: it is low in Zambia (4.5% according to FinScope 2015) compared to the SG members we interviewed in Ghana and Tanzania with 32% and 85% respectively. The Kenyan women’s experience with technology, including mobile money, was that it provided ease of access, low costs, improved record-keeping, transparency and (in one case) reliable calculation of share-outs resulting from electronic records.

Limited Product Range

In terms of products for SG members, the women in Kenya reported that most banks serving SGs provided savings accounts. Only one bank had offered a small wholesale loan to one group. The women reported that banks made some efforts to lower entry barriers, for example by not charging account ledger fees or imposing a minimum balance.

Lessons for Banks

Drawing on all this, we believe there are a number of lessons for banks that will contribute to the success of future linkages with SGs, in particular:

- Understand your potential customers, get to know them and build trust: research both demand- and supply-side options. For example, six out of ten SG borrowers in Tanzania used loans for both productive investments and consumption purposes: this has clear implications for the development of tailored products;

- Segment the SG market: for example, women and youth in particular offer promising uptake of digital financial services, especially in Tanzania;

- Keep KYC requirements to an absolute minimum: lobby for changes in regulation and local government requirements, if necessary;

- Be prepared to experiment: remember, these linkages are likely to be context specific;

- There is rich potential for digitising informal collective savings: this offers the chance to record every single individual level transaction and thereby open up potential for cross-selling opportunities;

- Linking SGs can be profitable: some SGs we met in Zambia reported relatively regular banking transactions and high bank account balances;

- Acquisition costs for banks of acquiring new SGs and individual member accounts may well be high: especially in rural areas; and

- FSPs will need to work with SGs and their members to understand what is needed to ensure continuing active engagement and use of accounts.

Ian Robinson is an independent consultant and George Muruka is a senior consultant at MicroSave in Nairobi. They make up the demand-side team on the Savings at the Frontier programme.

Savings at the Frontier is a $17.6 million partnership between Oxford Policy Managementand The MasterCard Foundation. Its aim is to expand the range of financial products and services available to people living in poverty in Ghana, Tanzania and Zambia by testing and implementing business models that sustainably deliver those products and services to savings groups and other informal savings mechanisms. For more information, please visit the link.

Bench marking customer to agent ratios

DFS providers struggle with a variant on the chicken and egg problem: whether to recruit more agents or more customers? How to provide adequate access for customers while ensuring agents face sufficient demand? All are interested in striking the right balance. New research from The Helix Institute finds that to date we have overestimated the number of customers per agent required to ensure network viability in maturing markets.

DFS providers struggle with a variant on the chicken and egg problem: whether to recruit more agents or more customers? How to provide adequate access for customers while ensuring agents face sufficient demand? All are interested in striking the right balance. New research from The Helix Institute finds that to date we have overestimated the number of customers per agent required to ensure network viability in maturing markets.

Existing Industry Benchmarks

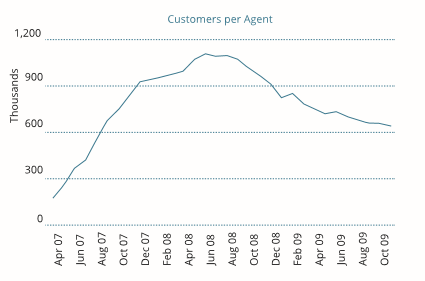

Until now, network management gurus (GSMA, McKinsey, The Helix Institute) referenced what has become a CGAP’s classic: the graph depicting the evolution of M-PESA customer to agent ratio in the early month after its launch in Kenya (Figure 1).

Figure 1. M-PESA Customer to Agent Ratio (2007-2009)

In 2013, GSMA further qualified the M-PESA benchmark. Using data from the Global Adoption Survey, it recommended a target ratio of 150 to 800 active customers per active agent. A new Helix study draws on 15 datasets to offer updated and more precise benchmarks for five leading DFS countries: Bangladesh, Kenya, Pakistan, Tanzania and Uganda. In this blog, we use a similar methodology[1] to examine provider-specific customer to agent ratios in these markets.

Registered Customers vs. Active Agents

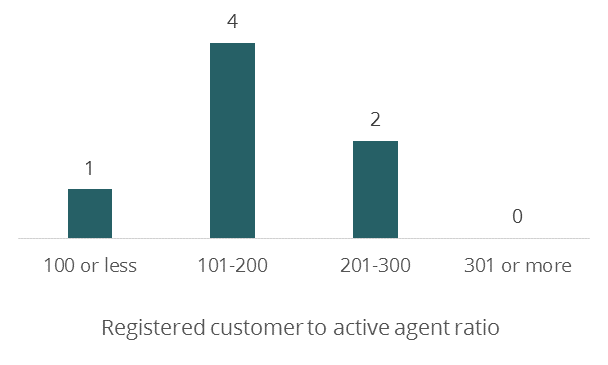

In East Africa, customers generally need a registered account to use mobile money and providers set targets for new registrations. These must be balanced with agent acquisition. Using the latest data available for Kenya, Tanzania, and Uganda[2] we determine provider-specific registered customer to active agent[3] ratios for seven leading MNO DFS providers range from just under 100 to under 300 (Figure 2).

Figure 2. Distribution of Leading East African DFS Providers, by Registered Customer to Agent Ratio

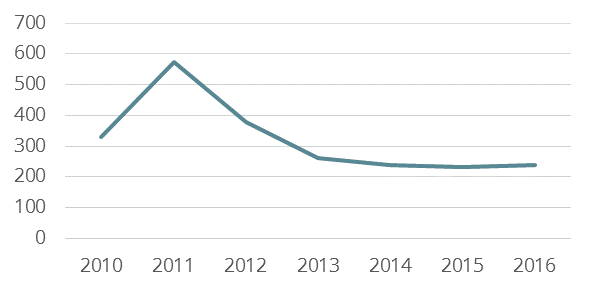

Figure 2 shows that the bulk of East African leading providers have registered between 100 and 300 customers for each agent who has transacted at least once over the past quarter. This ratio is much lower than the initial M-PESA benchmark. In fact, looking at more recent M-PESA ratios, calculated using subscriber and agent figures reported in Safaricom annual reports, we find that for the past four years it has flattened out between 200 and 300 (Figure 3).

Figure 3. M-PESA Subscriber to Agent Ratio (2010-2016)

Registered customer to agent ratio will and should fluctuate during periods of expansion, as providers shift focus between on-boarding new customers and new agents. Nevertheless, benchmarks can help gauge whether growth is becoming too imbalanced. Importantly, provider and agent viability will vary even at similar registered customer to agent ratios, depending on product offering, customer activity rates, and commission structures. Thus, customer to agent ratios should not be targeted in a vacuum.

Active Customers vs. Active Agents

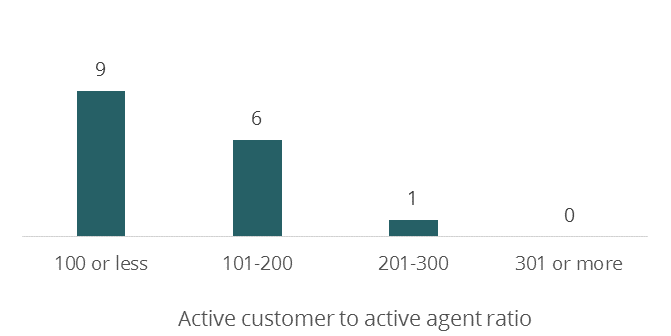

Because a large proportion of customer accounts are inactive, we also examine the ratio of active customers[4] to active agents for 16 providers in the five leading markets (Figure 4). Naturally, these ratios are much lower than the ones in Figure 2.

Figure 4. Distribution of Main DFS Providers in Five Leading Markets

Plotting active customer to active agent ratios in the most dynamic digital finance markets helps update and narrow the target range from 150-800 down to 100-300. Some factors that affect these ratios include DFS take-up and usage rates. Higher levels of dedication would translate into the ability and need to accommodate greater numbers of customers because dedicated outlets focus exclusively on serving mobile money clients. High agent churn could lower the ratio as less experienced agents tend to serve fewer customers, or increase it if outlets going out of business are not immediately replaced. While proposing benchmarks amidst this complexity is a tricky affair, we find the 100-300 range more useful than the guidance available up to now.

Ratios vs. Agent Performance

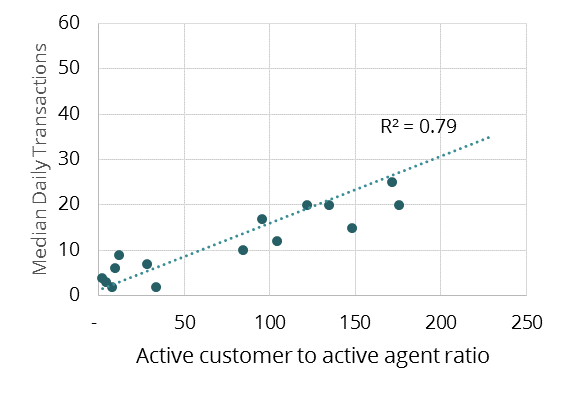

To further hone in on the viable range of active customer to active agent ratios, we have plotted them against agents’ daily business volumes (Figure 5).

Figure 5. Agent Business Volume vs. Active Customer to Active Agent Ratios

NOTE: One provider’s data is included in the analysis but not shown as its unique values would have revealed its identity.

Some sixteen data points only indicate a trend, but Figure 5 presents a fairly clean and strong one. Interestingly, providers with a ratio of 84 or higher perform a median of ten transactions or higher. Therefore, we can make a tentative conclusion that to keep median daily transactions above ten, the ratio of active customers to active agents should fall roughly within the 100-250 range, depending on commission rates, agent density and other variables like transactions per active customer.

Conclusion

In nascent markets, customers transact less often than those in more mature markets, where customers have developed trust in the DFS systems and enjoy a wide range of opportunities to transact. The above analysis suggests that in “lift-off stage” of deployment providers may aggressively recruit customers to drive demand for their service. This, in turn, allows them to further expand the agent network. As DFS take-up and usage rates intensify and the deployment reaches its “orbit stage”, the ratio of customers to agents will eventually flatten out, at a much lower range of 100-300 than the 400-600 benchmarks the industry has been using until now.

[1] We combine data from IMF and World Development Indicators with nationally representative Agent Network Accelerator (ANA) and Financial Inclusion Insights (FII) surveys to calculate provider-specific number of active agents as well as registered and active customers. See Appendices III, V, VII and IX in Agents Count. for a more detailed explanation.

[2] Analysis is based on the latest data available, which is 2014 for Kenya and 2015 for Tanzania and Uganda.

[3] Active refers to agents who have conducted at least one transaction in that past 90 days. Bank of Tanzania statistics on activity rates are used as best available proxy for Kenya and Uganda.

[4] Active customers are defined as having performed a financial transaction using mobile money in the past 30 days.

Where credit is due – Customer experience of digital credit in Kenya

Digital credit offers enormous promise to enhance provide a valued service to the mass market thus increasing financial inclusion, while also driving uptake and use of digitial financial services (DFS). However, with 2.7 million people already blacklisted on the credit reference bureau in Kenya, concerns are growing about current standards of regulation, customer protection and product design. In response, MicroSave conducted a brief study in Nairobi and Meru to examine the root causes of the alarming default rates on digital credit and propose recommendations for regulators/competition authorities, providers and other stakeholders. The research examined the process of applying for loans from different providers as well as conducting individual interviews with borrowers to understand their needs, aspirations, perceptions and behaviours.